TMTB Morning Wrap

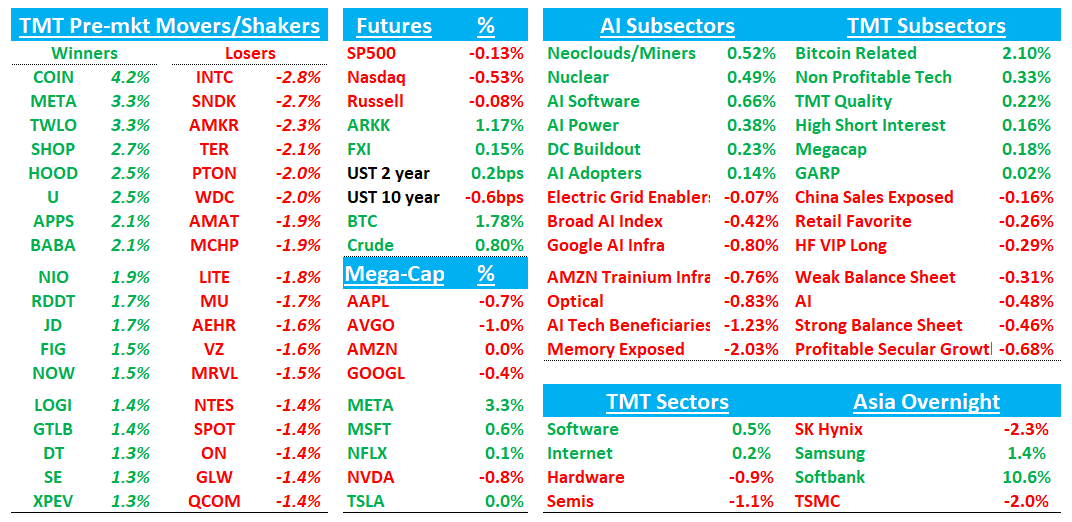

Happy Friday. Big focus overnight continues to be META +3% while other hyperscalers flat (more below on META). Semis -1% while Software +0.5% and Internet +0.2% in the green.

Relatively quiet morning. Asia mainly green overnight: TPX +0.39%, NKY +1.2%, Hang Seng +0.6%, HSCEI +0.52%, SHCOMP -1%, Shenzhen -1.24%, Korea KOSPI +2.52%. Memory names mixed but Softbank +10%.

Lots to get to so let’s get to it…

META

We wrote about META in our EOD wrap yesterday here. Lots of sell side notes out overnight…a few snippets of some of the more interesting ones below…

META: Why Meta is selling AI models now

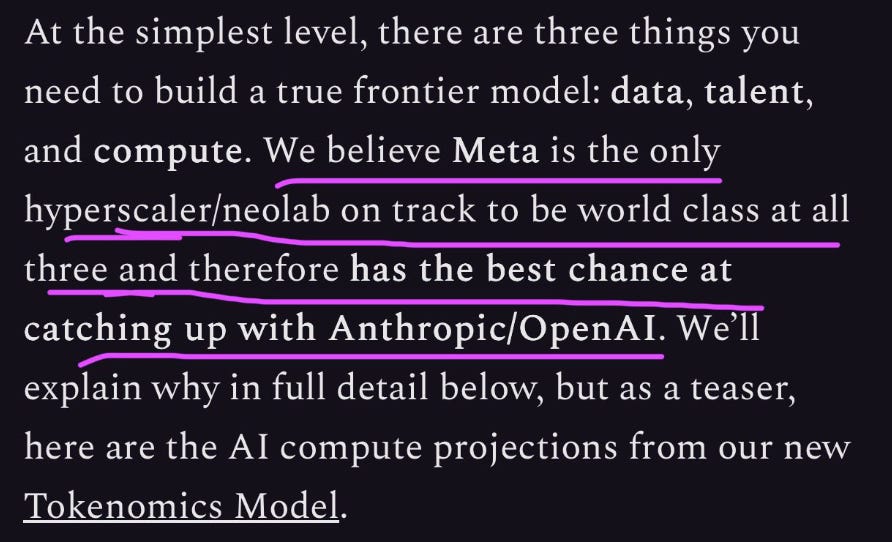

When I got Alexandr Wang on the phone ahead of Meta’s Muse Spark 1.1 release, I wanted to know how serious Meta was about its new API business for selling access to the model, which now puts it in more compeitition with OpenAI, Anthropic, and Google. Wang said that Meta sees the API as a real business, not just a learning exercise. Tokens are “gigantic and growing very, very quickly,” he told me, and capturing even a slice of that “can be a very meaningful business even for Meta at our scale….I floated the theory that Meta built more compute than it has inference demand, and the API soaks up the slack. Wang said no; the model is worth sharing on its own, and watching how developers use it will shape what Meta builds next."…“We feel really optimistic about our ability to be at the frontier by the end of the year,” Wang told me.”

META: Semianalysis: “In our view, the race for 3rd is currently between Meta and SpaceX, not Google.”

META: BofA Reads Reuters Chip Memo as Positive — 14GW 2026/27 Capacity Target Implies Costs Well Below Street; Buy, $835 PO

BofA flags the Reuters-reviewed internal memo showing Meta targeting 14GW of compute capacity additions across 2026–27 (6.5GW in 2026 vs. BofAe 2.6GW), which if accurate implies ~$22B cost per GW (assuming $145B of capex this year)— less than half BofA’s $45B/GW estimate — suggesting engineered cost savings with significant positive economics vs. Amazon/Google Cloud annual revenues of $10–16B per GW. BofA views the Iris custom chip as a sentiment positive supporting capacity ROI, though unlikely to drive 2026 savings.

META: KeyBanc Raises PT to $790 on Product Cycle Velocity — Preferred Megacap Into 2H; Maintains OW

KeyBanc lifts 2026/27E revenue 1% each to $254.6B/$308.1B and introduces 2028E at $366.9B (4% above Street), arguing Meta’s AI product cycle — Muse Image’s strong benchmark reception, Spark 1.1’s business-task performance (e.g., Harvey), and API pricing competition — can drive positive revisions plus P/E expansion. For 2Q, KeyBanc models in-line revenue of $60.2B with EPS 3% above consensus, and sees 3Q guidance of $61–64B with upside to typical q/q seasonality from AI products and wearables. KeyBanc’s checks show Family of Apps still generating healthy ROI despite macro/geopolitical ad-budget risk. New $790 PT rolls to 20x 2028E EPS; bull case $1,065 at 25x if new AI revenue streams gain traction.

META: Benchmark Maintains Hold on Leaked 14GW Memo — Capacity Ambition Escalates but ROIC Bridge Still Missing

Benchmark reads the leaked memo (14GW by 2027, capex up to $145B) as escalating ambition without addressing the ROIC visibility anchoring its Hold: the incremental 7GW implies ~$350–400B of spend at $50–60B/GW, pointing to a step-function guide raise or off-balance-sheet buildup, while Meta declines to quantify its cloud-capacity commitments. Setup skews asymmetrically to downside through 2H26–’27 absent explicit unit economics or performance-per-watt disclosure