TMTB EOD Wrap: META in the spotlight

Good afternoon. QQQs +1.6% as Oil -2% and yields fell 2-5bps across the curve.

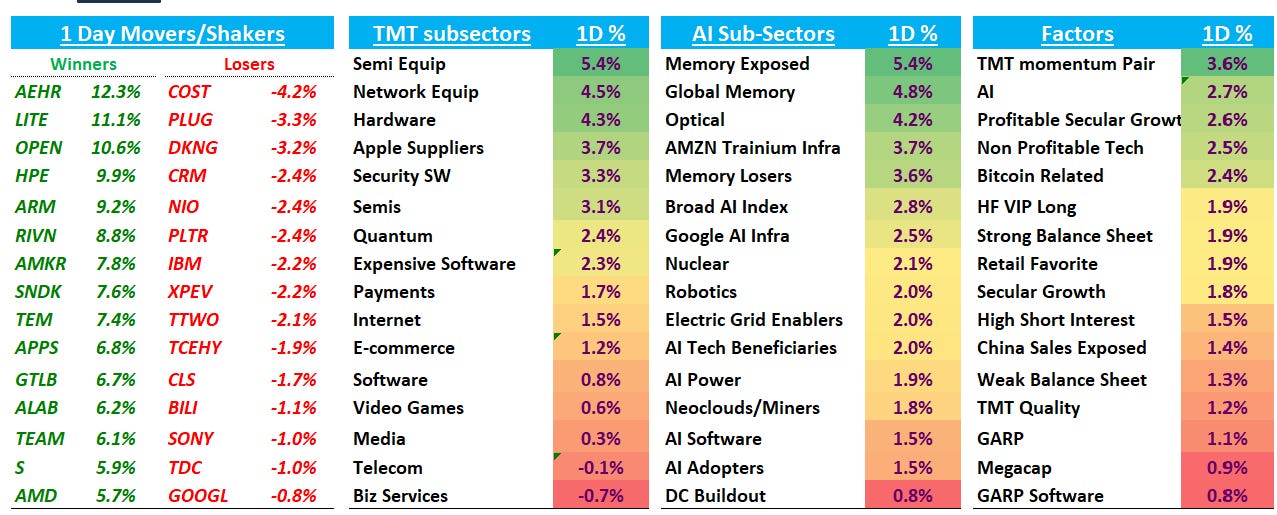

In Tech, Internet/Software +1% hung in there but market was led by Semis +3% which were aided by an early Reuters report that META was going to double compute capacity next year to 14GW, which helped negate some of the chatter around “excess capacity” and META cutting capex following the Bloomberg article about them selling compute last week. To put some numbers and context around the discussion, META likely ends the year somewhere around 7-8GW this year. If you assume ~$35B per GW (lot of assumptions on this # so could be wide range), that implies close to $250B in capex next year. Street is at $135B/$160B for ‘26/’27 and buyside was closer to $155B/$215B+ coming into today, so that latter number definitely gets bumped up. One would imagine the initial ‘27 capex guide is somewhere around $215/$220B then gets moved up throughout the year. The obvious read from the market was more capex = good for AI semis.

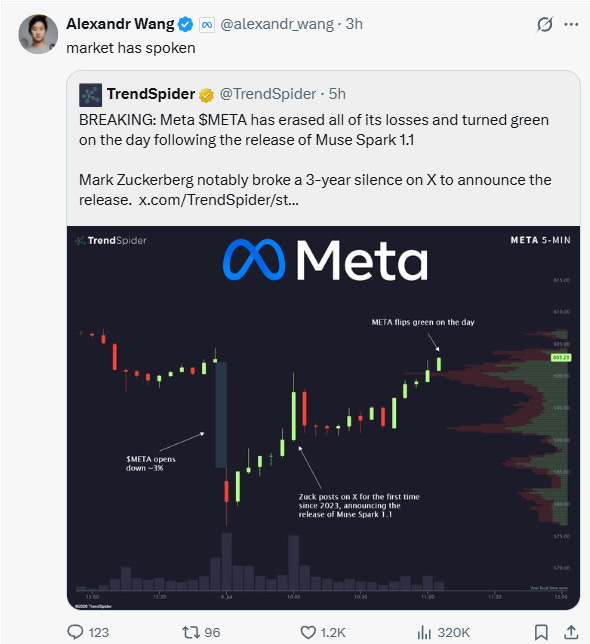

META stayed in the spotlight throughout the day with the release of Muse Spark 1.1. We’ve had 3 big model releases from 3 of the labs this week: MSL (Muse Spark 1.1), xAI (Grok 4.5), and OpenAI (ChatGPT 5.6). While most of the talk yesterday was about Grok 4.5’s better than expected cost & capabilities, today’s focus was on Muse Spark 1.1, where early agentic benchmarks show it at the level of Opus 4.8/GLM 5.2 although still trailing a bit in coding benchmarks. Pricing is very aggressive at $1.25/$4.25 Input/Output, which is even cheaper than GLM 5.2:

META finished +5% and even Alexandr Wang got in on some pumping near the end of the day:

Semianalysis had an article near the close talking up MSL’s ambitions, saying: “In our view, the race for 3rd is currently between Meta and SpaceX, not Google.”

Bulls hoping this is enough to sustainably turn around the META narrative — we think it’s definitely helpful, but more inroads need to be made + you still have the whiplash on hyperscaler ROI narrative to contend with & need an accel in ad #s to get investors pencil’ing a higher EPS while helping the ROI argument. Still, we think this week’s model releases from MSL and last week’s article about monetizing some compute likely limit the downside here and makes the r/r more attractive, which jives with the move today which was likely helped by some short covering.

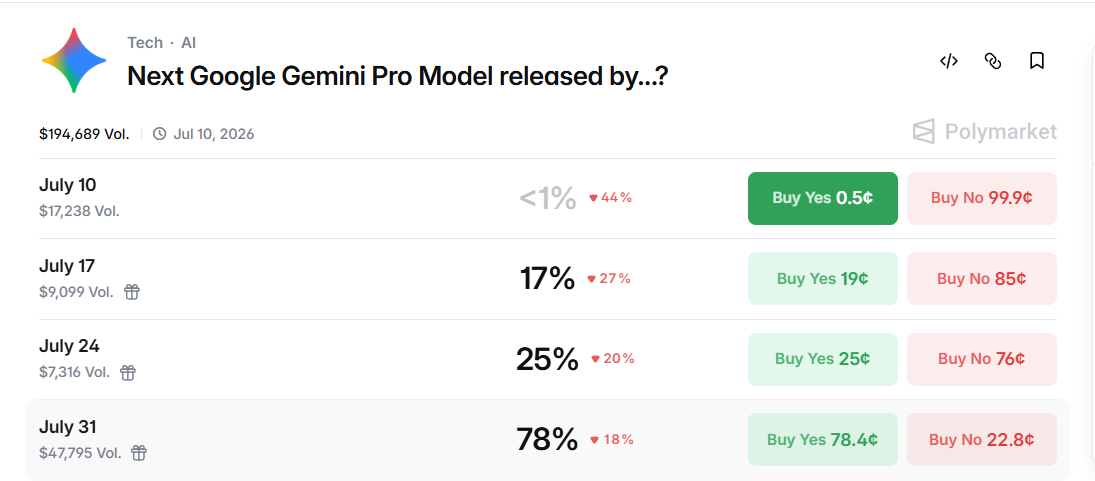

The perception of GOOGL -1% falling behind in the SOTA race has been around for a couple months now (falling behind in coding/talent leaving to Anthropic & OpenAI, etc.) which is part of the reason it’s been in the funding short camp. It likely remains there near-term, but we just saw how fast xAi/META’s perception can change (at least temporarily) following a model release, and we likely get Gemini Pro by the end of July, so something to keep an eye on:

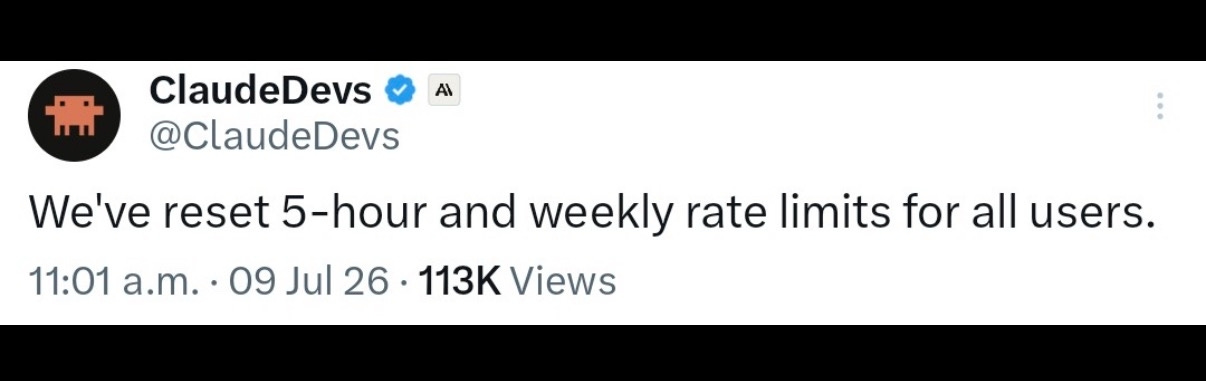

Anthropic feeling a bit of the heat as the race heats up:

Ok, let’s get to the roundup:

AI/SEMIS

Semis strong all day although most names faded as the day went on. Fwiw (mainly for some of you fast money guys), the pattern this week has been whatever out or underperforms intraday, that tends to follow through the next day.

LITE+11% outperformed for the first time in a while while the rest of the optical space also caught a bid GLW/CIEN +5%; COHR +3%; NOK +8%. Rosenblatt was out defending the group saying the 1–2 month optical selloff to short sellers pushing a China InP over-capacity thesis they don't strongly believe — multiple shorts told the firm they'll cover into 2QCY26 prints (late July/August) and buy optical in 2027 for the 2028–30 scale-up CPO opportunity. Rosenblatt's work shows Chinese players (Dongshan, Sanan IC) could add just 20–40% to its ~$26B 2030 InP forecast that already runs 40% behind demand; Chinese makers lack working 200G EMLs, are far from CPO lasers, and supply is decoupling anyway. Klein (tech spec) at Mizuho was also out saying biggest contrarian long bet in semis would be buying optical into july earnings. Our sense is the group will continue to be ripe for short-term trading shifts in narratives, while investors wait until ‘27 to sustainably size up, which means investors will trade around catalysts more than other groups. Some interesting conferences/catalyst to mark on your calendar for the group in 2H: