TMTB EOD Wrap; MDB First Takes

Good afternoon. QQQs +13bps today with some nice buy the war news action after being down closer to 1.5% in early morning trading. Yields jumped 9-12bps across the curve due to the spike in energy price. Brent finished +875bps. Here’s VK:

Trump warned the campaign could persist for 4-5 weeks, and Iranian retaliatory strikes were inflicting some (minor) damage throughout the region while (tragically) claiming several lives (including at least six American servicemen), but the consensus view is that this conflict won’t metastasize into an uncontrolled quagmire (that is based on the absolute military dominance of US and Israeli forces, Iran’s utter isolation, and a willingness by major OPEC+ producing countries to increase oil production, as they did on Sunday)

But above all else, we know Trump wants inflation low and the narrative clean as we head into midterms and we think he’ll take whatever off-ramp is necessary to make sure that happens. VIX was up 20% at one point and finished in +MSD to end the day. Bitcoin finally got a bid finishing the day +6%, carrying bitcoin related names with it. Overall, QQQs and SPY remain range bound.

Most Tech investors spent the day at the Palace Hotel taking in 1x1s and presentations — our chats were quieter than normal today.

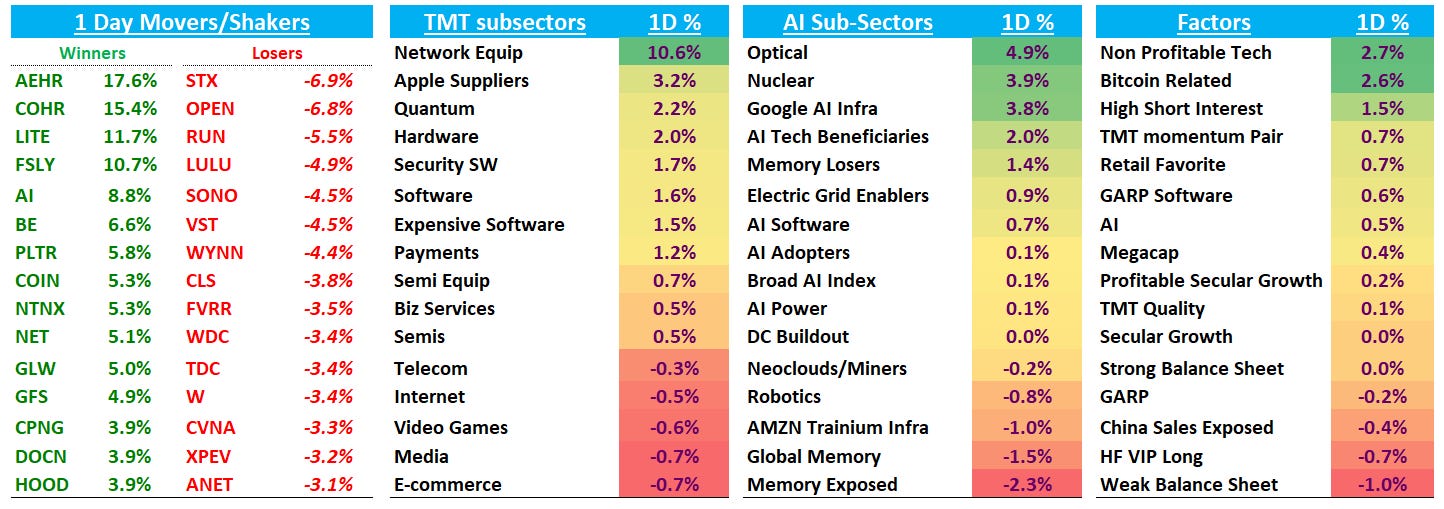

In price action, Optical was the standout today as NVDA +3% announced they were investing $2B in COHR +15% and LITE +12%. More good news for the optical bulls — as if they needed any more — as we head into GTC where bulls hope NVDA makes some more positive optical announcements (we went over GTC expectations in our weekly yesterday in case you missed it).

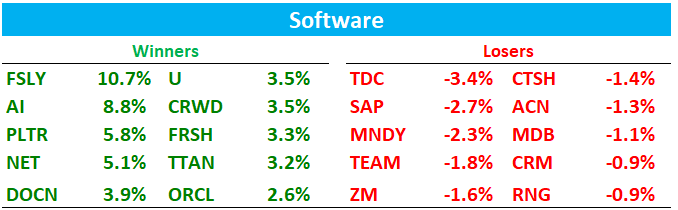

Nuclear and software was also strong (IGV +1.5% vs semis +0.5%, 4 out of the last 5 days where sw outperforms). On the flip side, memory-exposed and AMZN Trainium infrastructure names lagged. On the factor front, non-profitable tech and bitcoin led the way higher.

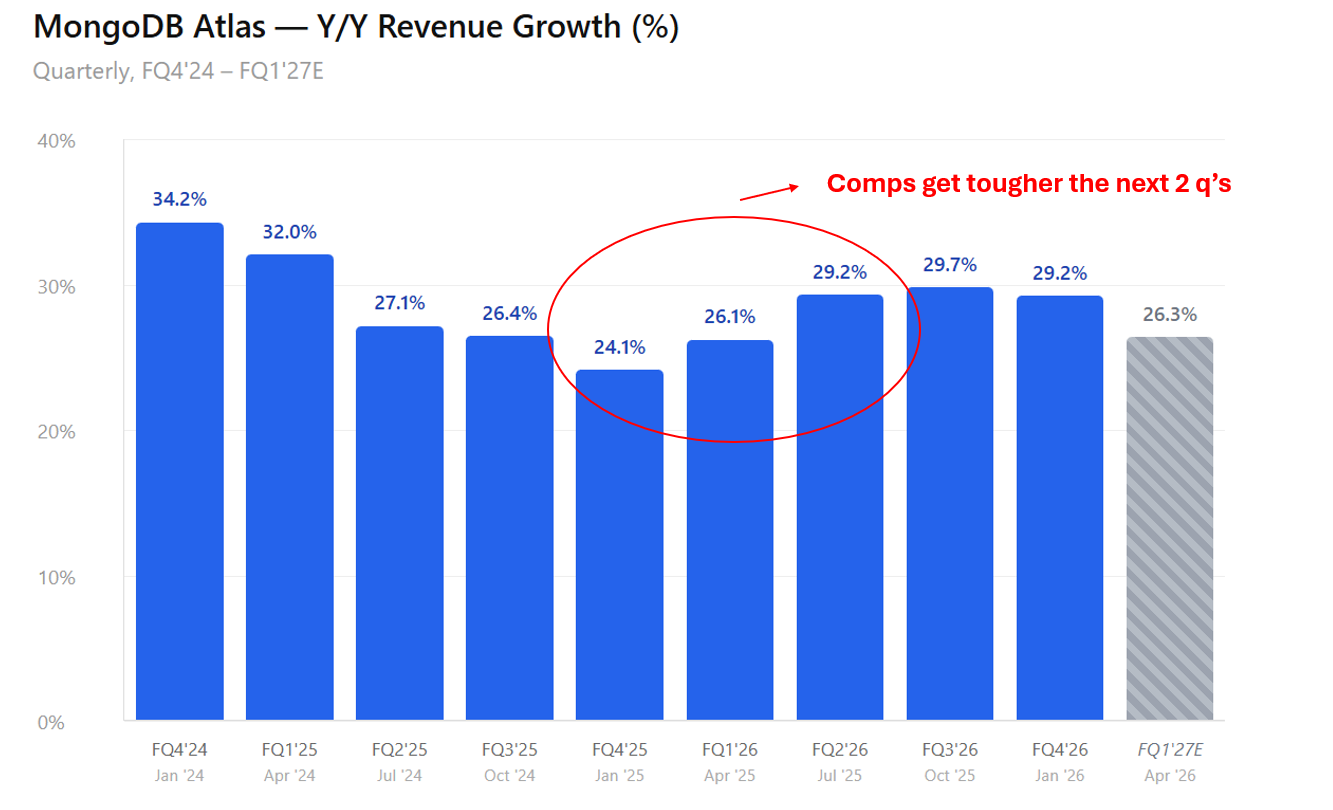

Post-close, MDB -25% catching bulls off-guard with Atlas only 29% y/y this q vs buyside closer to 30%. Guiding FY27E revs $2.86B-$2.90B, +16.3% to 17.9% Y/Y vs bulls who wanted closer to 19%. 2 heads of sales leaving. We get Atlas revs for Q1 and F27 on the call, but likely don’t look great given comps get tougher in Q1 and Q2 after several quarters of it getting easier. Not a great look when CEO was making the podcast rounds sounding good. If sw investors didn’t reward SNOW on their better print, then this worse print doesn’t bode well for a stock still trading at 8x+ ev/sales

Let’s get to it…

AI / SEMIS

NVDA +3% finally catching a bid trying to make back it’s post earnings slide as MS made it its top semi pick arguing the shares have been flat for two quarters despite strengthening fundamentals due to concerns over growth durability that should pivot to “2027 enthusiasm” in coming months. Joe Moore has been pretty good with top picks — as he was keen to point out in his note — as he previously took NVDA off top pick status in September in favor of memory, and is now hopping back on board. Some investor enthusiasm around new products (Groq & optical) likely being announced at GTC and Jensen is giving his keynote at MS TMT on Wednesday.

AEHR +17% as William Blair upgraded to Buy saying they believe the company has secured multiple design wins in both package-level and wafer-level burn-in across at least two major customers. Blair’s proprietary 2030 model for AI processor burn-in tools projects a $1.5B–$2.3B TAM, with a 30% share supporting the firm’s $50–$70 valuation range. Also heard some seeing a positive read-through from the bullish Irrational Analysis’ piece on Groq this weekend. Here’s Claude:

The Irrational Analysis piece specifically highlights hybrid bonding to stack SRAM on Groq-style chips as a key Nvidia IP synergy. Hybrid bonding requires known-good-die (KGD) testing — you absolutely must verify each die works before permanently bonding them together, because once bonded they can’t be separated. That’s AEHR’s core competency with their FOX wafer-level burn-in systems. More exotic multi-die packaging = more testing required per unit, not less.

The broader trend is even more important: The article describes a proliferation of complex, specialized AI chip architectures — Groq, Cerebras, TPUs, custom ASICs — all of which are moving toward advanced packaging (chiplets, 3D stacking, hybrid bonding). Every one of these architectures increases test and burn-in requirements because the cost of a packaging failure scales with die complexity and package value. A bad die in a $30K AI accelerator module is catastrophically expensive. AEHR is the only company offering both wafer-level and packaged-part burn-in for AI chips, which is exactly what you need as architectures get more complex.

TER +2% potentially in sympathy

BE +6% didn’t’ see much here.

Memory mixed: MU flat. STX/WDC -4-6%; SNDK -2.5%…Didn’t see much but imagine some rotation here given sw and NVDA o/p

AMD -80bps after being down closer to 4-5% in early morning - didn’t see much here.

AVGO -25bps ahead of earnings this week