TMTB EOD Wrap

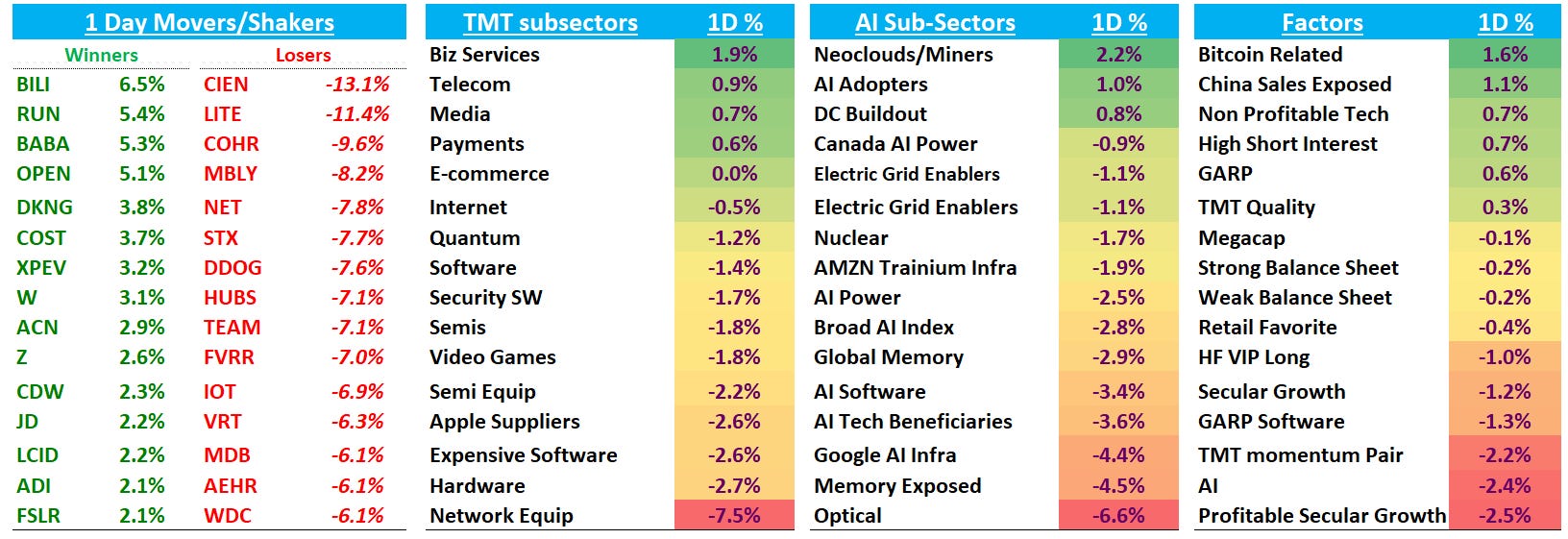

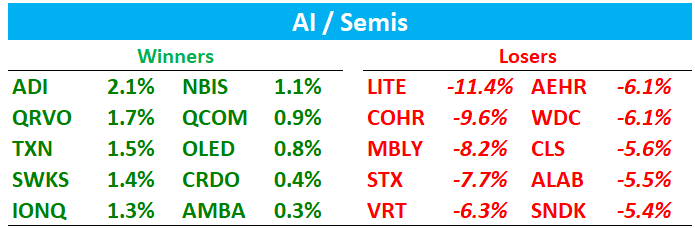

QQQs -57bps today in a pretty fragmented factor day coupled with AI infra unwind / rotation: the worst pocket was Network Equip (-7.5%) and anything tied to optical + storage + DC plumbing, with CIEN (-13.1%) COHR (-9.6%) and LITE (-11%) dragging the optical stack, and HDDs/memory getting hit: STX (-7.7%) / WDC (-6.1%) / SNDK -(5%) alongside Google AI infra (-4.4%) while weirdly enough Neoclouds outperformed. Unclear what exactly catalyzed the rotation — some speculated Anthropic raise at only $350B, mixed OAI Dec. data (see morning wrap) Musk vs. OAI lawsuit that could go to trial - but I didn’t really hear any great explanations that made a ton of sense.

Software was also heavy (Software -1.4%, Expensive Software -2.6%) with not much spared as app sw / secular growth winners / consumptions names all getting clipped (DDOG -7.6%, MDB -6.1%, ADSK -5.9%, NET -7.9%, SNOW -4%), while “safer”/less-duration TMT held up better (Biz Services +1.9%, Telecom +0.9%, Payments +0.6%) and select IT/services names worked (ACN +2.9%, CTSH +2%). Other leadership came from Bitcoin-related (+1.6%), China sales exposed (+1.1%), and high short interest / non-profitable tech (+0.7% each) with higher-beta/shorted stuff like OPEN +5.1%, RUN +5.4% IONQ +1% working. IWM > QQQs by 150bps+.

On the positive side, AMZN +2% continues to work in one of those early 2020s streaks which have been absent for a couple years. Given its a Top 3 crowded long in Tech, many happy about that.

Trump helping pump the housing market after the close - $200B in MBS:

Let’s get to it…

AI / SEMIS

Claude code is the real deal…

Neoclouds IREN +5%, CRWV flat, NBIS +1% outperformed the rest of AI infra. Only thing I saw was APLD positive comments (h/t James Keller in TMTB chat):

And what we’re seeing is a big opportunity in the compute side of the market, obviously the data center side as well, but the compute side of the market, you’re seeing a lot of deals happen over the past three or four months in that part of the market, We’re involved in with a lot of those counterparties and discussions and have been, and we think there’s a really large opportunity for our cloud business as we spin it out into ChronoScale to get some of those types of contracts. And working with us, we think there’s a really unique relationship there where we can get data center capacity to be able to deploy significant scale for those style of contracts with those customers.

BE +13% the standout winner today as merican Electric Power (AEP) has executed a massive $2.65 billion unconditional purchase agreement with Bloom Energy. This deal is for a almost all or all of the 900 MW option AEP held (originally signed in Nov 2024). Positive takes is that this was a significant positive suprise that supports the bullish view that there is demand to support an expansion beyond 2gw. The purchase agreement is “unconditional,” meaning AEP is committed. Even if the specific offtake conditions aren’t met by Q2 2026, AEP expects to be financially compensated for all capital costs, effectively de-risking the deal for Bloom. The pushback: There is confusion regarding whether this project is incremental (new) or just the formalization of the previously known “Tallgrass / Crusoe” project in Cheyenne.

Saw Mizuho come out and say ASP of roughly ~$2,950/kW (based on $2.65B for ~900MW) is below their prior estimates of ~$3,000/kW+, implying Bloom gave a “volume discount” to secure the order, which could compress Gross Margins. There is also

INTC -3.5%. Trump out after the close: