TMTB Morning Wrap: Netflix (NFLX) Takeaways + The Usual

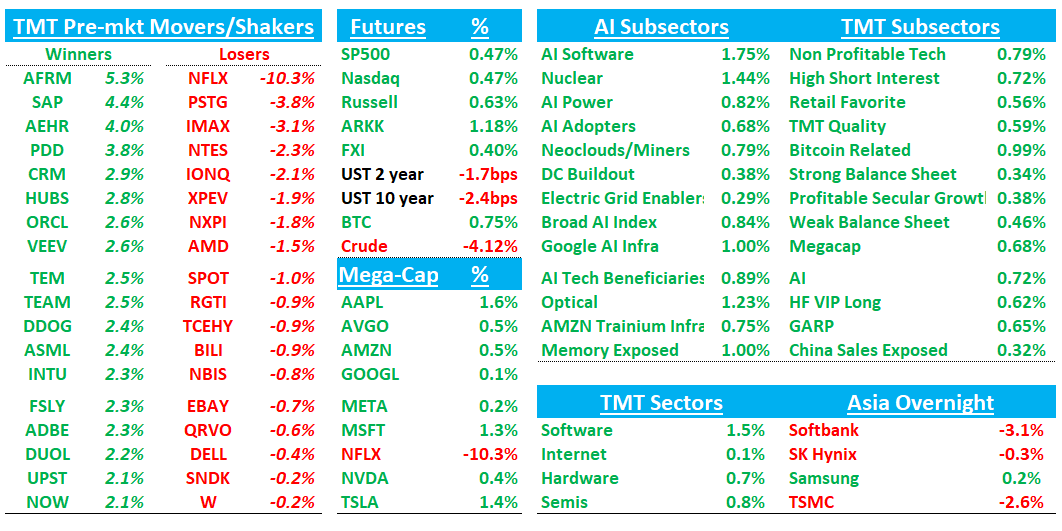

Happy beautiful Friday morning. Futures +50bps looking to continue its win-streak. Crude is lower by 4% as geopolitical news was quiet. Asia mainly red: TPX -1.41%, NKY -1.75%, Hang Seng -0.89%, HSCEI -0.67%, SHCOMP -0.1%, Shenzhen +0.37%, Taiwan TAIEX -0.88%, Korea KOSPI -0.55%

Lots to get to it, so let’s get to it…we’ll hit up NFLX first then onto the usual…

NFLX: Decent quarter but lack of FY raise, lower Q2 margin guide, and Reed Hastings leaving weighing on the stock. With engagement debt not settled, likely moves into funding short camp

Quarter was fine, but the stock was set up for more near $110, specifically some combination of a 2Q margin beat, a FY26 raise, and clearer upside from the March U.S. price hike after the WBD walk-away. That did not happen. Buyside settling in around $4 for CY27. Bears will say 20x ($80), bulls will say closer to 25-30x which gets you to $100-$120. We think range around $90-$110 for now. Around $100 this likely moves into funding short camp as without engagement ticking up, unlikely to get close to 30x and not many exciting catalysts on the horizon (world cup could be viewed as pot’l negative for engagement in Q3)

The #s:

FQ1’26

Revenue $12.250B, +16.2% y/y (last q +17.6% y/y) vs Street ~$12.18B, +~15.5%

Revenue ex-FX +14.1% y/y (last q +15.8% y/y)

Operating Income $3.957B, +18.2% y/y vs Street ~$3.94B

Operating Margin 32.3%, +60 bps y/y vs Street ~32.3%

GAAP EPS $1.23 vs Street roughly $0.76-$0.80

FCF $5.094B vs Street roughly $3.0B

Q2 Guide:

Revenue $12.574B, +13.5% y/y (~12.0% ex-FX) vs Street ~$12.63-$12.64B, +~14.0%

Operating Income $4.105B vs Street ~$4.33B

Operating Margin 32.6% vs Street 34.3%

GAAP EPS $0.78 vs Street ~$0.84

FY26 Guidance

Revenue $50.7B-$51.7B; midpoint $51.2B, +13.3% y/y (11%-13% ex-FX) vs Street roughly ~$51.3B, +~13.5%

Operating Margin 31.5% vs Street roughly ~31.6%-32.0%

Advertising Revenue ~ $3.0B, roughly +100% y/y, broadly in line with Street

FCF ~ $12.5B vs prior $11.0B

Key Takeaways:

Mgmt attributed the margin miss that to heavier 1H content amortization and some M&A cost timing.

Price hike commentary was constructive, but not enough to offset the lack of a raise. Mgmt said the U.S. price change was part of the plan, that early signals were in line with expectations, and that retention improved y/y in every region. The issue for investors is timing, since the full P&L benefit looks more 3Q-weighted than 2Q-weighted.

NFLX reiterated ~$3B of ad revenue for FY26, or roughly doubling y/y, with 60% of sign-ups in ads markets on the ad tier, 4,000+ advertisers, and programmatic approaching 50% of non-live ad revenue. Ad loads were unchanged, while fill rates continue to improve.

On engagement, one of the main overhangs on the stock, Mgmt said total viewing grew at a similar pace to 2H25, despite the Winter Olympics, and its internal quality engagement metric hit another all-time high. But NFLX continues to avoid giving investors a clean external metric to track, which likely keeps the debate alive.

APAC and live events were a real bright spot. The World Baseball Classic was a standout, with 31.4M viewers, the largest sign-up day ever in Japan, and Japan leading Q1 member growth globally. Mgmt also stressed APAC strength was broader than one event, citing India, Korea, and Southeast Asia.

AI, product expansion, and newer surfaces were incremental positives. Mgmt talked up InterPositive, better recommendation models, podcasts, vertical video, and the kids gaming app as ways to widen engagement and eventually improve monetization.

TECH RESEARCH/NEWS

Optical/Networking: GS Sees Next AI Mega Trend; 9x TAM Expansion Driving Supply Chain Upside

Goldman Sachs says optical networking is emerging as a key bottleneck and value driver in AI infrastructure, with scale-up architectures driving a step-function increase in dollar content (16–45x per unit) and expanding TAM ~9x to ~$154B by 2028; the firm highlights strong growth across optical modules, CPO/NPO, copper interconnects, and PCB midplanes as AI clusters scale (GB300 → Rubin Ultra), with scale-up (in-rack) and scale-out (cluster) both benefiting, though scale-up capturing ~70% of value; GS sees significant EPS upside across the optical supply chain as CSP deployments ramp, with adoption first led by hyperscalers, supporting multi-year growth through higher speeds (400G/800G), increased rack density, and rising connectivity requirements.

Anthropic/AI: Opus 4.7 Vibes not good so far

Should continue to help sw sentiment this morning

Anthropic: Financial Times talks with Anthropic chief Dario Amodei

Some quotes from the article:

“I suspect open-source models and Chinese developers will be able to replicate [Claude] Mythos’s capabilities within six to 12 months.”

“There’s no end to the rainbow. There’s just the rainbow. We don’t see anything slowing down. I’m the first to say that it’s going to completely transform the world and we’re underestimating its significance.”

“We should not deny that the disruption is going to happen. We just have to make the positive effect so large that we have a tool to address the disruption. [AI could help] raise the annual GDP growth rate in the US to 10 per cent a year, or more, [but it could also] eliminate about 50 per cent of all entry-level white-collar jobs within five years. [Ultimately, AI can only] diffuse at the speed of trust.”