TMTB Morning Wrap: MongoDB (MDB) & Credo (CRDO) Recaps & Tech Research/News

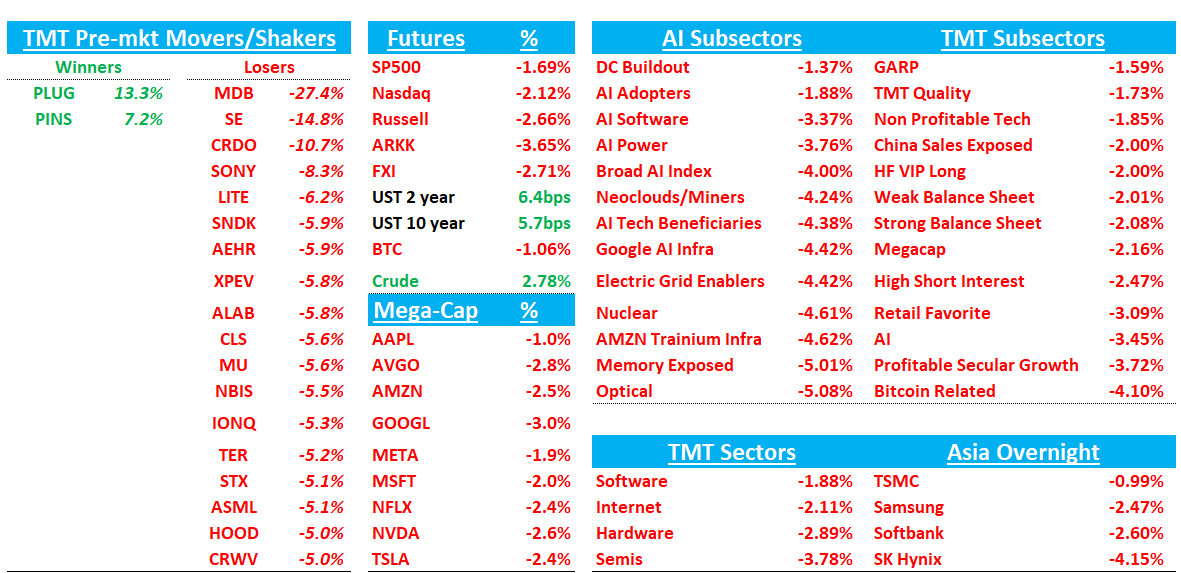

Good morning. Futures -2% this morning as concerns that the Iran response will be longer than expected, which is aimed at disrupting the entire region by targeting key economic and energy infrastructure. Oil is up another 7% as concerns Hormuz Strait will stay closed longer than expected.

Asia red overnight with Korea the biggest loser plunging 7%+ with memory names leading the way lower: Hynix and Samung both down mid teens. Memory names in the U.S. following a bit with SNDK/MU/HDDs all down 4-5%. BTC -3.5%. Yields are up another 5-8bps amid inflationary concerns. Dollars is up close to 2% over a couple days. Fed expects actually shifting in a more hawkish direction with the odds of a next cut not happening until Sept ticking higher.

Let’s get to it…MDB, CRDO, SE and CORZ First, then the usual…

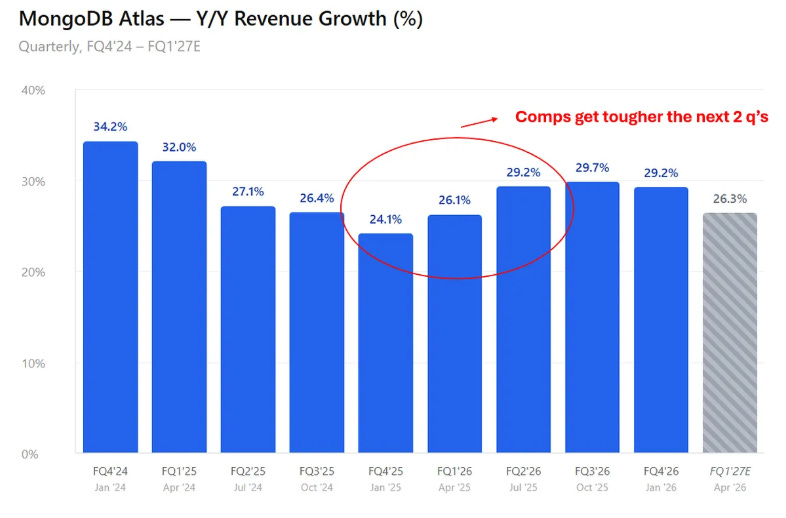

MDB weaker and decelerating Atlas growth + FY27 top-line growth guidance was below Street as we head into tougher Atlas comps

Print catching some consumption bulls off guard (positioning leaned long heading into the print) as Atlas only 29% y/y this q vs buyside closer to 30% (mgmt said bundled EA + Atlas activity shifted rev attribution toward EA implying Atlas would have been closer to 30%). Guiding FY27E revs $2.86B-$2.90B, +16.3% to 17.9% Y/Y vs bulls who wanted closer to 19%. Multiple executive transitions including a new Chief Customer Officer, departure of Chief Revenue officer and president of field operations. This is key chart for me below - Atlas decel’d in Q4 on a 2 ppts+ easier comp and now the comps get 2 ppts harder in Q1 and 3 ppts harder in Q2 so Atlas acceleration seems in the rear view mirror, especially with mgmt guiding FY27 Atlas in low 20s. For a stock with some structural/competitive hair (and now execution overhang given exec departures) and sw in a state of high valuation purgatory (stock still 7x+ ev/sales) not a great look and stock likely falls into funding short camp.

The #s/Key Takeaways:

Revenue $695.1M, +26.7% y/y (last q +18.7% y/y) vs Street $668.0M, +~21.8% y/y; Atlas revenue $502.6M, +29.2% y/y vs Street $494.4M, +~27.1% y/y and buyside 30%

Non‑GAAP EPS $1.65 vs Street $1.48; non‑GAAP OM 22.8% vs 21.3%

FY27 revenue guide $2.86–$2.90B (mid $2.88B, +~16.9% y/y) vs Street $2.898B, +~17.6% y/y and buyside closer to 19%; F1Q27 rev guide mid $661.5M (+~20.5% y/y) vs Street $662.7M (+~20.7% y/y).

EA + other subscription revenue $170.5M, +20.1% y/y vs Street $154.0M, +~8.5% y/y. Mgmt repeatedly emphasized that large multi‑year EA deals are the biggest swing factor and they will only include deals with a high probability of closing to avoid negative surprises

On AI, mgmt reiterated AI revenue is not material yet, while highlighting that customers using vector search and Voyage embeddings more than doubled y/y, and positioned MDB as a core “memory/state/retrieval” layer for agentic workloads.

On the call back, the key incremental clarification was that Atlas consumption “could have been stronger” in Q4 vs the last couple quarters, even though consumption trended within the quarter as expected, and guidance incorporates the February consumption trend that mgmt saw.

Mgmt reiterated the bundling/revenue allocation issue: bundling itself is common, but Q4 had a customer making a bigger EA commitment, making the revenue allocation more EA-weighted than expected.

Mgmt is not breaking out AI revenue yet (needs to be meaningful versus Atlas’ ~$2B+ scale), but emphasized working with 2 of the 3 biggest frontier model companies and the goal to be the best database for agents; also noted they are not seeing cloud repatriation to EA, though some customers want on‑prem as a resiliency backstop.

On competition/post-gres, mgmt said MDB is directly positioning against Postgres on scale + performance + security + platform integration. On the call, CJ cited a specific competitive win where Emergent Labs “selected Atlas over PostgreSQL” for AI agents, and then broadened the argument that many AI-native teams make early DB decisions and later run into scale/security issues, while MDB wins because it’s enterprise-class and offers native JSON + vector search + embeddings “in one” integrated platform (vs stitching multiple moving pieces together).