TMTB Morning Wrap: Gitlab, CRWD and WIX recaps / News & Research Recap

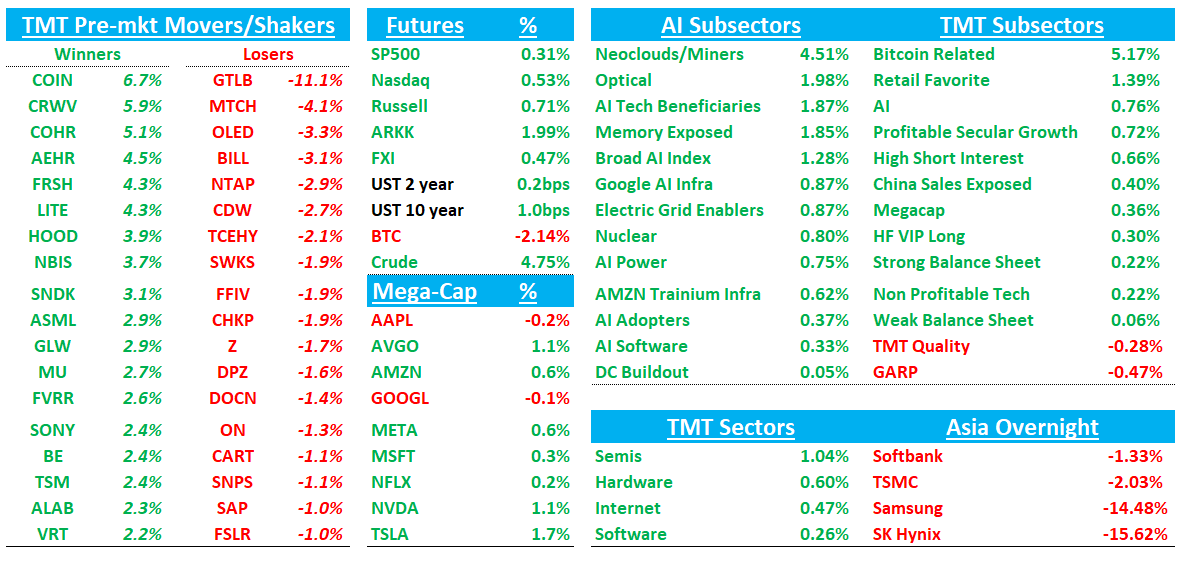

Good morning. Futures +50bps as stocks bounce back from yesterday’s red day. On the macro front, the Iran strikes continue, but NYTimes was out this morning saying officials from Iran’s Ministry of Intelligence reached out to the CIA to discuss ending the war. Stocks in Asia mainly red across the board with Korea the big loser: TPX -3.67%, NKY -3.61%, Hang Seng -2.01%, HSCEI -1.45%, SHCOMP -0.98%, Shenzhen -0.53%, Taiwan TAIEX -4.35%, Korea KOSPI -12.06%. Korea now down 20% in 2 days back to levels not seen since…(checks chart)…early February. Memory stocks down big but so far U.S. names not following with SNDK/MU +2-3%. Semi favorites bouncing as well with Optical and semi-cap leading the way higher this morning early.

Big news last night as well was Dario’s bullish MS TMT talk (we sent out notes last night here). The $19B ARR # was confirmed by Bloomberg. That’s up from $9B at the end of 2025 and $14B a few weeks ago so seems like even a bit of accel in the latest month. So $10B added in 2 months. At this pace, get to $60B by the end of the year. Not bad.

BTC +5% while yields are slightly up.

We’ll cover GTLB/CRWD/WIX earnings first then onto the usual.

GTLB -8%: Ok Q4 above street (although $3M one time benefit), but weaker Q1 guide and the initial FY27 outlook (especially margin) was below Street/bogeys. Bulls will say setting new CFO up for beats and raises; bears have questions. TheInformation OpenAI/Github article out a couple minutes after call ended (not a coincidence) weighing on stock as well as more fuel for bears.

OpenAI/GTLB: OpenAI Is Developing an Internal Alternative to Microsoft’s GitHub - TheInformation

According to The Information, OpenAI is developing its own internal code repository to reduce its reliance on Microsoft’s GitHub, which has recently suffered from several disruptive outages. While the project is currently nascent and aimed at internal stability, OpenAI has discussed potentially commercializing the tool, which would place the startup in direct competition with its primary investor and cloud partner.

The #s / Key Takeaways:

Revenue $260.4M, +23% y/y (last q +24.6% y/y) vs Street $252.2M, +~19% y/y. Mgmt flagged ~$3M of one-time benefit (FX + JiHu-related) inside the quarter, so beat would only have been 2% which is at the low end of historical beats.

EPS $0.30 vs Street $0.23; non-GAAP OM 20.5% vs 15.3%; FCF $41.8M (16% margin) vs Street $26.6M

DBNRR was 118% (down 1 pt q/q). Separately, RPO-based bookings growth was cited at ~5% y/y (down from ~11% last quarter), reinforcing the bear argument that GTM under-execution is still the core issue.

Q1 Guide: Revenue $253–$255M, +18–19% y/y vs Street $257M, +~20% y/y; Non-GAAP operating margin ~13% at midpoint vs Street 13.6%

FY27 revenue guide $1.099B–$1.118B, +15–17% y/y vs Street ~$1.13B, +~18–19% y/y; FY27 non-GAAP OM guide ~12% vs Street ~16.5% (biggest disconnect).

Mgmt repeatedly positioned FY27 as a year to 1) reaccelerate first orders, 2) add sales capacity, 3) expand packaging, 4) address the price-sensitive cohort, and 5) advance the AI strategy (DAP). They pointed to bookings growth not keeping pace for multiple years and cited ~300 bps of non-recurring FY26 tailwinds (price increase / FX / contract clauses) not embedded in FY27.

Mgmt framed the FY27 non-GAAP OM ~12% (vs Street ~16.5%) as a deliberate investment stance plus a structurally lower gross margin guide (85–87%) driven by mix (SaaS, Dedicated, DAP)

On AI, DAP is GA (January), mgmt emphasized early feedback and that they’re pushing from trials to production, but they also signaled monetization is more of a FY28 story (limited meaningful FY27 contribution embedded)

Co authorized $400M repurchase

Bull vs. Bear Debate:

Bulls argue the most important takeaway is that GTLB is intentionally “spending into” a multi-quarter turnaround while preserving strong cash generation and balance sheet flexibility. The quarter reinforces that GTLB can still execute on profitability in the near term (20%+ non-GAAP OM in FQ4) and generate meaningful FCF, even while absorbing macro lumpiness and a pressured SMB/mid-market cohort. Bulls also like mgmt’s explicit articulation of a concrete operating plan: first-order reacceleration, more sales capacity, packaging expansion, and a clearer AI roadmap, which provides a framework for investors to underwrite a reacceleration that is “within mgmt control” rather than dependent on a macro snapback

On AI, bulls believe the market is underappreciating GTLB’s potential to monetize beyond seats through an “agent platform” that naturally fits into the DevSecOps lifecycle, especially as AI-assisted coding expands code output and therefore increases downstream needs for testing, security scanning, policy, and deployment. They view FY27 guidance conservatism on DAP as a setup for upside, not a sign of failure, because mgmt is not embedding meaningful FY27 DAP revenue contribution and is emphasizing conversion from trials to production. Bulls also point to portfolio mix improving (Ultimate penetration) and see the repurchase authorization as a confidence signal that can help compress downside if execution is merely “okay.” With stock trading sub 3x revs, don’t need much to go right for stock to work.