TMTB Morning Wrap

Good morning. Futures +1% as Trump following hopeful media reports and commentary over the weekend about an end to the war with Trump saying negotiations are “proceeding nicely.” Rubio said a deal would take a few more days to get done. However, things took a small step back overnight as US fired on certain Iranian targes in a “defensive” move.

Yields down 4-6bps across the curve while Oil. Brent fell 7-8% yesterday but bouncing 3% today.

Asia mixed: TPX -0.1%, NKY -0.25%, Hang Seng -0.03%, HSCEI +0.3%, SHCOMP -0.17%, Shenzhen -0.6%, Taiwan TAIEX -0.27%, Korea KOSPI +2.55%. Lots of AI semi names up significantly in Japan and Korea over the past two days; Samsung +3%; SK Hynix +7%. Lenovo up another 15% after being up 20% on Friday. Softbank +11%

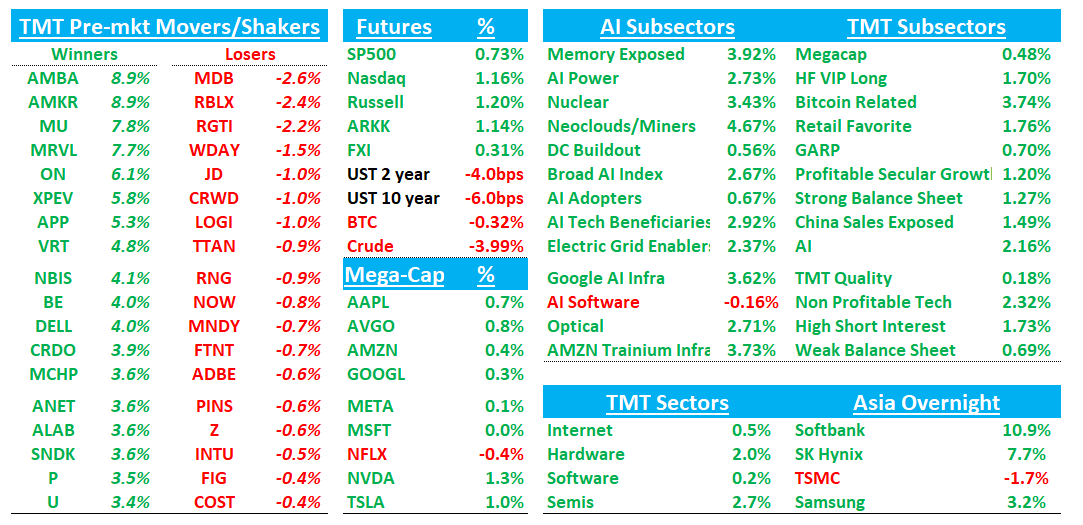

In the U.S. AI Semis names leading us higher as well with Semis +3% while Software/Internet lag. What’s new?

TD Cowen’s TMT conference begins tomorrow. This week, we get earnings from SMTC, ZS, CRM, MRVL, P, SNOW, DELL, S, ESTC, and MDB. You thought earnings were over?

Lots of good stuff to get to today, so let’s dive straight in:

MU: UBS Raises PT to $1,625 as LTAs Reshape Memory Cycle and Support >$100 EPS Power

UBS sharply raises MU PT to $1,625 from $535, arguing new long-term agreements (LTAs) are fundamentally changing the memory industry by improving visibility, smoothing cyclicality, and supporting structurally higher earnings power. The firm believes enhanced LTAs now cover 20-30% of industry DDR bit shipments and ~60-70% of server DDR5 volumes, helping stabilize pricing and lock in supply assurance for hyperscalers. UBS now expects MU EPS to remain comfortably above $100 through at least C2029 and forecasts ~$400B of cumulative FCF from 2027-2029, while also highlighting continued upside from HBM pricing/tightness and AI-driven DRAM demand growth.