TMTB Morning Wrap

This is the last post of the shortened week. We will be back to regularly scheduled programming Morning and EOD Wraps on Monday.

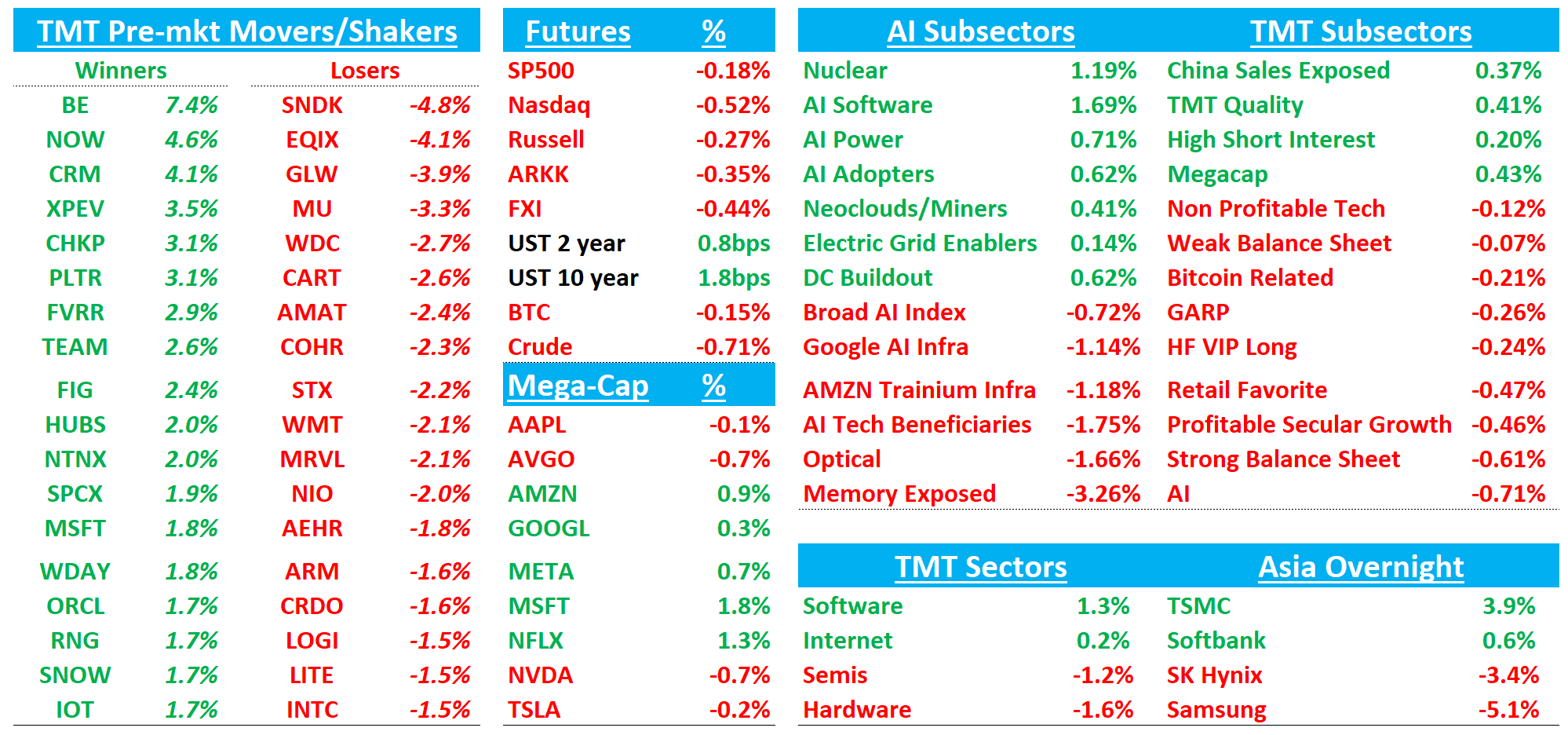

Good morning. Futures down 50bps on a relatively slow day as we head into July 4th weekend. Yields up slightly 1-2bps across the curve ahead of the jobs print tomorrow morning as the market continues to price in 35bps worth of hikes this year.

Asia saw mixed price action: TPX +0.42%, NKY +0.59%, SHCOMP +0.44%, Shenzhen +0.39%, Taiwan TAIEX +1.94%, Korea KOSPI -2.04%. Korea weighted down by memory: SK Hynix -3.5%; Samsung -5%. Taiwan helped by TSM’s +4%.

In the U.S., Software +1% outperforming Semis -1% early with the former helped by a few upgrades from Difucci at Guggenheim (CRM, NOW, CHKP). Memory following Korea memory names lower (SNDK -5%, MU -3%). HDDs and Semicap also weak to start the new month.

Fable looks to be coming back soon…

Let’s get straight to it…

BE: Brookfield and Bloom Energy Expand AI Infrastructure Partnership to $25 Billion; Fivefold Increase to Build and Finance Rapid Power for AI Infrastructure

PR:

Bloom Energy (NYSE: BE), a global leader in power solutions, and Brookfield today announced the expansion of their strategic partnership as Brookfield increases its framework to finance power projects for AI infrastructure – from previously announced $5 billion to $25 billion – a fivefold expansion since October 2025. The increased funding will help grow the fuel cell partnership globally.

The expanded partnership is part of Brookfield’s dedicated AI Infrastructure Fund, which launched in November 2025 with a target to deploy $100 billion. Brookfield’s strategy is focused on investing in large AI factories, power solutions, compute infrastructure, and strategic capital partnerships. Brookfield is one of the world’s leading AI infrastructure investors, with over $100 billion already invested in digital infrastructure and clean power assets.

BE: Evercore Says Brookfield’s Expanded AI Power Partnership Reinforces Bloom’s Speed-to-Power Advantage

Evercore raised its PT to $350, arguing Brookfield’s decision to expand its AI power financing framework from $5B to $25B reinforces strong demand for Bloom’s distributed power solutions. While the announcement included few project-specific details, the firm believes the fivefold increase validates its “speed-to-power” thesis, with hyperscalers increasingly prioritizing fast, reliable behind-the-meter power as grid constraints persist. Evercore views the announcement as another positive demand signal supporting Bloom’s long-term AI infrastructure opportunity.

BE: Morgan Stanley Says Brookfield’s $25B AI Power Expansion Reinforces Bloom’s Long-Term Growth Outlook

The firm estimates the expanded framework implies roughly 5GW of fuel cell deployment potential and supports its existing forecast for 14.6GW of Bloom deployments through 2030, while creating upside if additional large projects are secured. Morgan Stanley believes the announcement, combined with recent project wins and supply chain checks, strengthens confidence in further estimate revisions over time.

NOW: Guggenheim Upgrades on Valuation, Not AI, as Federal Spending Recovery Supports the Outlook

Guggenheim pgraded ServiceNow to Buy, arguing the recent selloff has created an attractive valuation opportunity, with the stock now trading at ~5.9x EV/NTM recurring revenue, despite expectations for continued double-digit organic growth. It believes improving U.S. federal government spending should help remove a key overhang after a sluggish year, while stressing the upgrade is not driven by AI monetization, which it still views as uncertain and a potential long-term risk. Even so, the firm believes ServiceNow’s durable recurring revenue model and improving government demand create an attractive risk/reward at current levels.

CRM: Guggenheim Upgrades on Valuation, Not AI, Arguing the Market Has Become Too Pessimistic

Guggenheim upgraded Salesforce to Buy, arguing the stock’s 3.7x recurring revenue multiple already prices in a perpetual decline despite expectations the business can continue generating durable cash flow. While the firm remains skeptical that AI will become a meaningful revenue driver in the near term—and believes agentic AI poses a real competitive risk—it argues the market has become overly bearish, with shares down ~41% YTD. Guggenheim sees a more likely outcome of slower but still positive growth rather than structural decline, creating an attractive risk/reward at current levels.

CHKP: Guggenheim Upgrades on Valuation, Arguing the Bad News Is Already Priced In

Guggenheim upgraded Check Point to Buy, arguing the stock’s valuation has become disconnected from the durability of its recurring revenue and free cash flow generation following concerns around its go-to-market transition. While the firm expects near-term disruption to product revenue and acknowledges growth will likely remain in the single digits, it believes the current valuation already discounts an overly pessimistic outcome, with shares trading at just 4.3x EV/NTM recurring revenue and 8.0x EV/NTM FCF. Guggenheim also expects continued share repurchases and believes improving channel sentiment and GTM execution provide upside without requiring a dramatic acceleration in growth.

META / CXL / MRVL / ALAB: Wells Fargo Says Meta’s Vistara Deployment Validates the Long-Term CXL Opportunity

Wells Fargo believes Meta’s large-scale deployment of its custom Vistara CXL ASIC (paper here) validates CXL as a production-ready technology and should increase investor confidence in the long-term CXL ecosystem. The firm highlighted Meta’s reported 20-25% compute capacity savings and 4-12% throughput gains, while noting CXL’s ability to reuse legacy DDR4 memory could lower server costs and support future 100TB+ AI models. While the near-term memory impact is limited given today’s tight supply environment, Wells Fargo believes Meta’s deployment reinforces the long-term investment case for CXL across datacenter memory and server infrastructure.