TMTB Morning Wrap

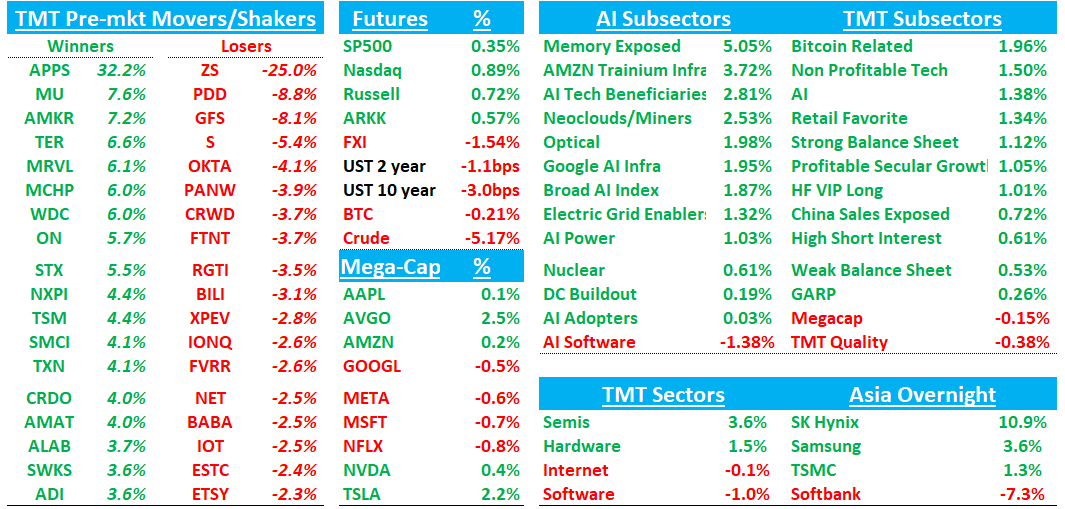

Good morning. Futures +90bps earlier led by — you guessed it — Memory and AI semis. MU +8% getting close to $1k. Lots of your favorite AI semi names up 4-6%. Internet and Software down early, the latter led lower by ZS’s -25% horrid print, which is bringing down other cyber names as well (PANW/CRWD -4%). Interestingly, hyperscalers largely weaker early with GOOGL/META/MSFT -50bps although AMZN in the green on UBS deep dive into their backlog as they take up AWS #s (more on that below).

Yield slightly down while Crude drops another 5% today.

Asia mixed but Korea in the green: TPX -0.52%, NKY +0.01%, Hang Seng -1.06%, HSCEI -1.33%, SHCOMP -1.25%, Shenzhen -1.3%, Taiwan TAIEX +1.68%, Korea KOSPI +2.25%. SK Hynix +10%; Samsung 3.5%; Lenovo +4.5%. Softbank -7%.

We’ll hit up SMTC +10% and ZS -25% first then get to the usual, where a lot of good stuff awaits today…

Let’s get to it…

SMTC +13%: Solid beat and raise with numbers and guide above bogeys and implying significant acceleration.

Not much to pick at here despite expectations being very high going in after TSEM and MTSI. Bulls very much in control as call confirmed the multi-legged product story and will like the DC 2H FY27 acceleration commentary.

The #s:

Q1: Revenue was $291.0M, +15.9% y/y (last q +9.3% y/y) vs Street $283.5M and bogeys closer to $290…EBITDA: $66.4m vs $58mn…GM: 53% vs 52.6%

Q2: Revenue $328M, +27.3% y/y vs Street $300.7M, +~16.7% y/y and bogeys closer to $310M..EBITDA $79M vs street at $63M.

Key Takeaways:

Mgmt called out upside tied to data center, optical and ACC momentum as driving the upside.

Data center revenue hit $71.6M, +39% y/y, and mgmt guided FQ2 data center to roughly $97M, +85% y/y / +35% q/q. Mgmt also walked away from the prior “50% y/y floor” framing and instead said growth should accelerate in 2H FY27, supported by backlog, bookings, 1.6T FiberEdge, CopperEdge and HieFo optical components.

Mgmt said 800G FiberEdge/TIA demand remains “exceptionally strong,” with wins across established and emerging module suppliers, including some sole-source sockets. Impt bc the FQ2 guide appears driven meaningfully by continued 800G strength, before the larger 1.6T contribution really builds in the back half.

Mgmt highlighted significant 1.6T optical design wins with major module makers using latest-generation DSPs, with shipments launching in FQ2 and module ramps supported by backlog in 2H. Early 1.6T volume is still FRO, while 1.6T LRO/LPO is under evaluation, creating additional upside if linearized optics adoption broadens.

Mgmt emphasized it began preparing capacity ~18 months ago, can support drop-in demand, and is working with foundry/OSAT/test partners to double or triple current capacity. HieFo gain-chip demand is running about 3x supply, with capacity targeted to rise 3-4x by year-end and another 3-4x by the end of next year.

SMTC started shipping 1.6T CopperEdge ICs to cable partners for a U.S. hyperscaler, and mgmt said ACC and on-board linear equalizer engagements should convert into design wins. Pushback here is customer cocentration, but mgmt said samples are being evaluated by multiple hyperscalers and enterprise customers

FQ1 gross margin was 53.0% vs Street 52.5%, and FQ2 guide is 54.0% vs Street 52.6%. Signal Integrity GM stepped down as HieFo entered ramp mode, but mgmt expects the 1.6T data center portfolio to be accretive to semiconductor products and Signal Integrity GM as it scales.

FQ2 OpEx guide of $105.2M is above Street, but mgmt tied the increase to R&D for data center and LoRa, while SG&A declines as a percentage of sales.