TMTB Morning Wrap

TMTB will be out on holiday beginning Friday through next week

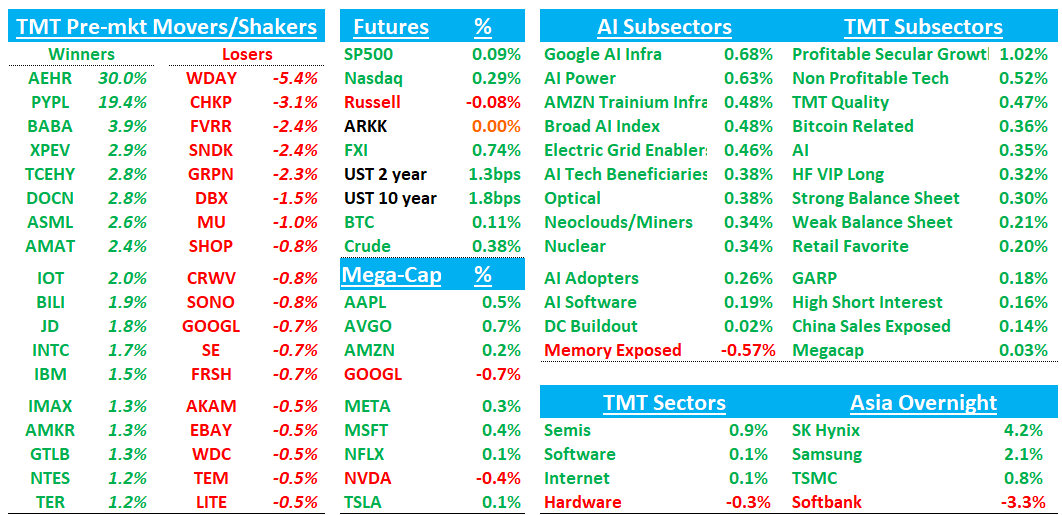

Good morning. QQQs +30bps as some turbulence on the Iran front as US carried out another round of strikes near Strait of Hormuz overnight and Trump said US may hit power plants and bridges next week unless Iran makes a deal. Oil is holding fairly steady. In Tech, semis +1% while software/internet are flat. Memory names lower with SNDK -2.5% and MU -1%.

Overnight, Asia mixed as Korea and memory names were strong following Hynix’s big move up in U.S (although underperformed KOSPI).: TPX +.22%, NKY +1.49%, Hang Seng +1.4%, HSCEI +1%, SHCOMP -0.29%, Shenzhen -0.68%, Taiwan TAIEX +2%, Korea KOSPI +6.24%. Samsung +2%. SK Hynix +4%.

Lots to get to, so let’s get to it…

ASML +3%: Very solid beat and raise above street and buyside. Q3/’26 guide and ‘28 commentary better while co points to large capacity increases. Only nit is ‘27 EUV slightly below bogeys

Revenue came in at €9.3B vs. Street expectations of €8.8B, gross margins were 54% vs. 52% expected, helped by higher sales volumes and business mix. Q3 GMs guided to 55-57%, well ahead of street in low 50s. ASML raised full-year guidance to €43-45B of revenue from €36-40B previously. Gross margin guidance also moved materially higher to 54-56% from 51-53%

The co. has indicated that they will raise both EUV and immersion DUV capacity in both 2027 and 2028 by 30% which would result in approx. 85/110 EUV and 169/210 Immersion DUV tools in 2027/2028, which is higher than the high on the street for ‘28 and would imply more than €65 in EPS for 2028, potentially even more given strong Installed Base Management revenue that ASML is already seeing. Only nit I’m hearing negative this morning is that the co. does not achieve 90 EUV tool capacity in 2027 (co guided 30% on 65 = 85), which is slightly below 90 bulls were hoping for.

Mgmt said demand remains exceptionally strong across logic and memory. AI-related investment continues to accelerate as customers pull forward capacity additions to meet robust demand for advanced logic and memory chips. In memory, ASML said current DDR and HBM pricing clearly signals the need for more supply, prompting customers to accelerate expansion plans. Company talked up very strong intake continuing across 1H and customers looking to accelerate capacity expansion. The company is seeing greater High NA readiness and points to Intel use at 18A earlier than expected. Also announces CMD for June 10th 2026.

AEHR +30%: Record Bookings and Backlog Drive FY27 Outlook Well Above Street

AEHR reported F4Q revenue of $18.8M, +34% y/y and roughly in line with Street with key record bookings of $60.7M lifted effective backlog to $100.6M, supported by expanding AI accelerator, silicon photonics and SiC programs. FY27 revenue guidance of $130M–$150M implies roughly 160%–200% growth and was about 50% above Street at the midpoint, with non-GAAP EPS guided to $1.80–$2.20 versus Street near breakeven.

PYPL +20%: Stripe, Advent offer to buy PayPal for more than $53 billion at $60.50 a share sources say - Reuters

The proposal follows an initial approach made in early April, the sources said. Stripe and Advent have not received a response from PayPal and are seeking to advance discussions in the coming weeks, the sources added.

Under the proposal, Stripe and Advent would jointly own PayPal, with each holding an equal stake, rather than breaking up the company, the people said. There is no certainty the approach will result in a transaction, they added.

PYPL: Bernstein Says Stripe Bid Could Reshape Global Payments but Faces Financing and Regulatory Hurdles

Bernstein sees strategic logic in Stripe/Advent’s reported $60.50-per-share bid for PayPal, given PYPL’s valuable Braintree, Venmo and branded-checkout assets, but believes a higher offer is unlikely because the proposal already values the company near 15x FCF versus a pre-deal multiple below 5x. Financing would be substantial—roughly $50B of committed debt plus rollover equity—and could push leverage toward 5x–6x, while integration complexity and regulatory scrutiny would also be significant. Bernstein sees a greater chance of selective asset sales or a broader bidding process than a clean full-company transaction at a materially higher price.

AMD: Rosenblatt names top long idea going into earnings and raises target from $490 to $665

We are expecting AMD server CPU, EPYC, to deliver over 70% y/y revenue growth at above corporate average gross margin,” and “we see AMD’s Venice server CPU as dominating high-end market as Intel’s Diamond Rapids server CPU has been delayed,” writes analyst Kevin Cassidy