TMTB Morning Wrap

QQQs -1% following through from yesterday’s weakness which broke Tech’s 10D win streak. Outside of Tech, F and MAT pulled their guide yesterday bc of macro/tariff uncertainty and a few others (Royal Philips, CLX) talked up uncertainty due to trade tariffs. China Caixain PMI came in soft (China +1%). All eyes on Fed decision/commentary tomorrow. Trump said a drug tariff announcement would arrive before the end of the month.

In Tech, we got some decent earnings from DDOG and PLTR but they are both trading down. We mentioned in our weekly that TEAM, CFLT, and TWLO’s price action late last week post-earnings was a bit of a change in character in software’s price action, and PLTR/DDOG are continuing that trend so far this morning. We read these as possible broader neg tea leaves for the market as the late April rip in the QQQs was partly catalyzed by NOW’s better earnings action post their print.

We’ll hit up Earnings first (DDOG, PLTR, DOCN, DASH), then move onto to Research/News/3p, where its a fairly slow morning.

A deluge of earnings on deck the next 3 days…Some on deck tonight that could influence AI trade (AMD, ANET, ALAB, SMCI)

Public comment window for the U.S. Section 232 semiconductor probe closes tomorrow…

Let’s get to it…

DDOG -3%: Solid Q1 and raises Q2/FY guide

The company raised its 2025 revenue guidance from ~19% to ~21% at the high end after Q1 inline with bogeys. Q2 guide also much better at 22-23% vs bogeys of 20%. That said, billings were a bit light and management lowered the 2025 operating income outlook — the revenue beat was the lowest vs guide in 7 quarters. Stock still down 25% YTD so the better rev guides should be good enough as keeps bulls hopes of mid 20s growth alive (comps get easier in 2H of the year)

Q1 results:

Revenue grew +25% (flat vs Q4’s +25%), beating guidance of +21% and landing in line with buyside expectations of +24-25%.

Added ~160 new customers with ARR >$100k quarter-over-quarter (Q4 added ~120).

Operating income came in at $167M, above guidance of $162-166M.

Billings rose +21% year-over-year (Q4 +26%) to $748M, slightly below Street at $752M.

Guidance updates:

Q2 revenue forecast is $787-791M (+23% at the high end), ahead of buyside expectations (~19-20%).

2025 revenue guidance was raised to $3.215-3.235B (~21% at the high end vs previous +19%).

2025 operating income guidance was lowered to $625-645M, down from the prior $655-675M, reflecting a ~20% operating margin vs the prior ~21%.

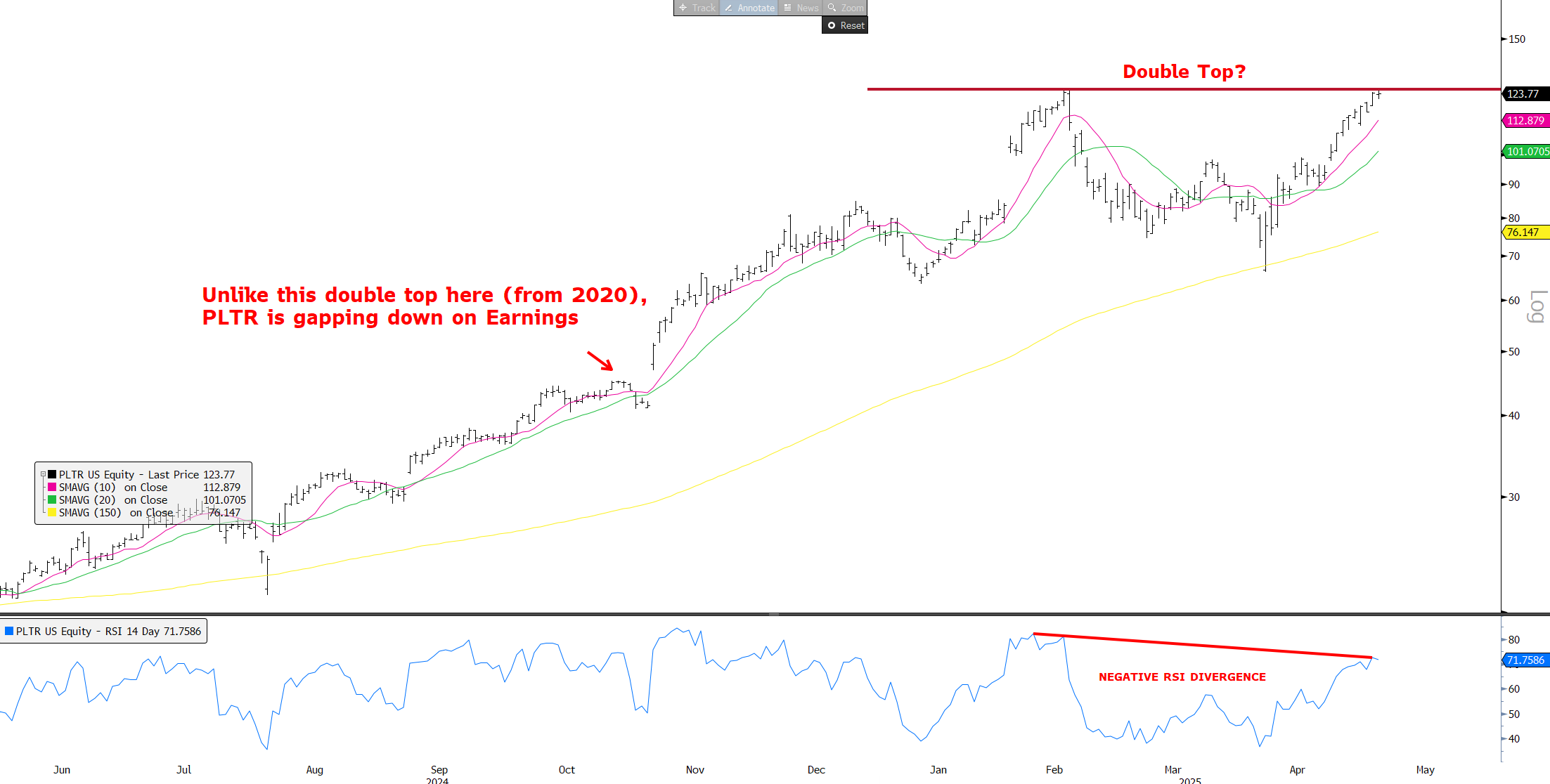

PLTR -9%: Another print, another acceleration in revs…

Total revs accelerated for the 7th q in a row to 39% as US comm +71% y/y and US Gov 45% y/y. FY25 rev growth raised to 36% from 31%. Importantly, Q2 guide was raised to 38% vs street at 33%, which is the toughest comp of the year and implies another accel to a likely 40%+. Billings accelerated to 45%. Other metrics were similarly good and mgmt sounded bullish on the call.

Two nits I’m hearing: Q1 rev beat was smallest in 5 quarters vs. guide and international commercial continues to show weakness, declining 5% y/y after growing 3% in q4, although granted it was on a tougher comp.

Our view: We thought quarter was good; importantly, the q2 guide alleviated our fears that growth might decel next q and implies we likely exit the year at mid 40s growth rate! PLTR is firing on all cylinders. Weakness in commercial worries us a bit, but its only 20% of revs and decel was on a tougher comps and comps get much easier going forward. Valuation is obviously in the stratosphere (200x P/E), but that’s been the case for a while now.

Still, PLTR is a unique stock that requires a unique approach to trading for us given its high valuation / retail-heavy base - weirdly, if the stock was up 3-5% today on a risk-on day, we’d be tempted to buy. We like trading PLTR intra q but need a good entry on the chart (with the right r/r) — and right market set up — to get involved on the long side. For now, we stay away and wait for digestion/better entry point on the chart although we remain positively inclined.

DASH -5%: Agrees to acquire Deliveroo + SevenRooms; Results looked ok….Q1 GOV 20.5% yy in line with bogeys. Q2 GOV 1% above street at the mid point, slightly better than bogeys. Q1 EBITDA slightly better although revs came 2% in below…

The big news is the expected acquisition of Deliveroo and SevenRooms ($1.2B in cash). A bit of pushback from investors this morning bc of the 2-for-1 deals going on, but DASH has a decent track record with WOLT might help it get a pass.