TMTB Weekly

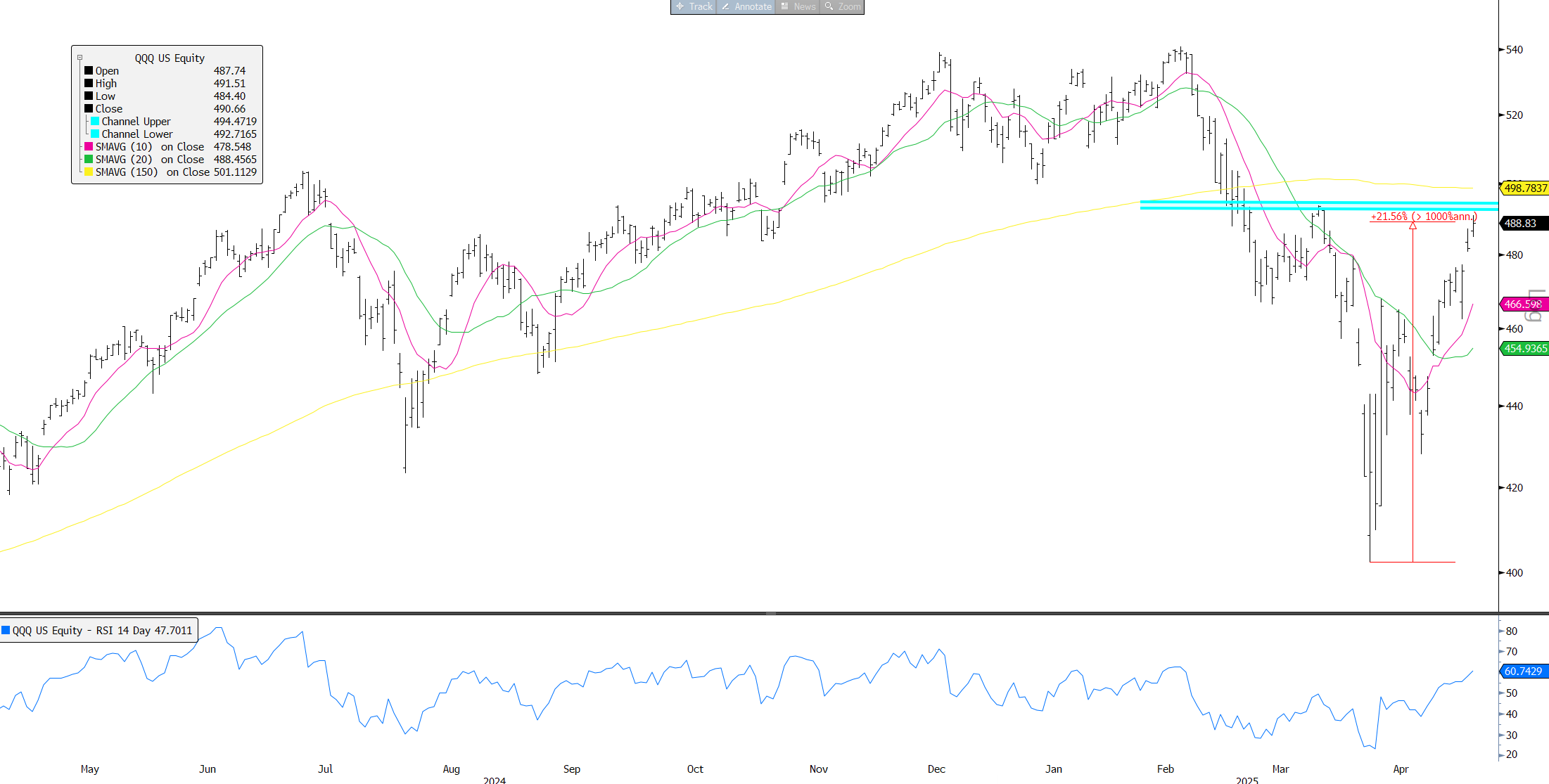

Happy Sunday. Another wonderful weekend where there is no tariff or tweet storm fire drill to cover, so I’ll take advantage of that and not spend too much time on the macro again. We’ll hit that briefly, then get into Tech after finishing the busiest week of earnings where we saw QQQs rip 4.5%, now up 21% from the bottom in one month.

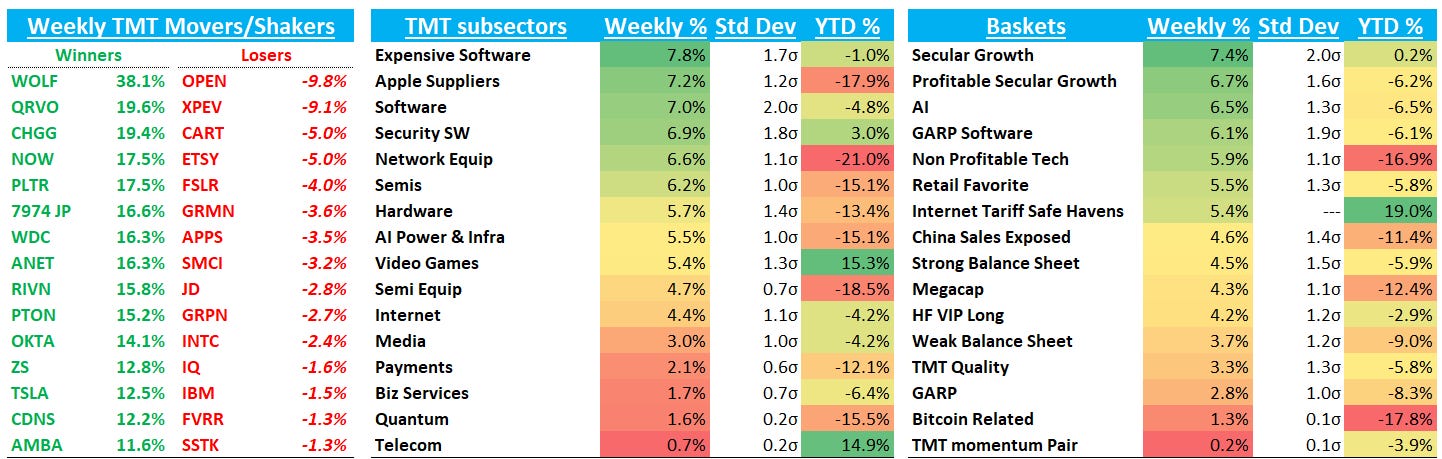

Weekly snapshot:

On the macro front, let’s recap the bull vs. bear debate:

Bulls continue to point to bullish price action (lots of “thrust” indicators close to being triggered” which usually point to v positive forward returns), very healthy Q1 earnings, some positive tea leaves between China and the U.S., peak tariff rates, potential for deals to get signed any day (India, South Korea, Japan, UK at the top of the list), admin’s focus will shift to tax cuts and de-regulation in 2H, and hard data still holding up (see the better NFP report on Friday) pointing to no recession. DOGE has lost its teeth (See Washington Post article this weekend: Republicans in Congress highly unlikely to approve even a fraction of DOGE’s cost cutting). Oil is below $60 and could head lower given Opec’s decision increase production. The yield tantrum seems to have subsided for now and the 10 yr sits at 4.3%. Investors have significantly reduced net exposures and a cross over the 200d will force investors to begin to re-gross up and CTAs to start buying again and the pain trade is higher to $6k on SP500.

Bears will say the view that the worst of the tariff-related economic damage is behind us is premature as the true impact will now begin to filter through the data while pointing to companies like AAPL and AMZN where brunt of tariff hit will only begin to be felt after the June Q. Bears will say while tariff rates will go lower, they are poised to stay well above where they stood back in January, particularly China’s. The impact of supply chain disruptions and increasing prices will begin to filter through the econ data over the next few months. Just take a look at comments from the ISM survey: they cite shipments stuck at the border, suppliers demanding tariff surcharges, and customers refusing to place orders without price clarity. The index still trades at 20x+ EPS of $265 , which likely has 2H downside risk and bears will argue than in times of uncertainty, the index should at best trade in high teens. The snap back has been a sentiment/positioning rally off extremely oversold levels. Bears will also point to the reconciliation bill that could carry a massive price tag, especially given deep divisions among Republicans over meaningful cost offsets — a scenario that could potentially be bad bond markets.

Seems pretty fair on both sides although we think bears have a slightly more compelling argument; our view, however, continues to be choppy and upwards trending given the price action we are seeing in stocks. As our friend Shrub has taught us, the most hilarious outcome is sometimes the most likely: I’m open to the possibility that we bottomed on peak tariff fears and will top on a day with tariff deal announcements.

For us, the stock picking environment has felt better, and we continue to focus on longs where there is little tariff/China exposure. The breadth and pace of the market rally has been wider and faster that we have expected but the strength in tariff/China safe havens hasn’t been surprising as we saw a similar dynamic during Covid times in stay-at-home winners.

Even in days with positive tariff news flow, we find that names with smaller tariff/China exposure are exhibiting outsized strength: just look at Friday with names like DUOL, CART, RBLX, SPOT, DASH leading the way higher in Internet. NFLX is up 11 straight days (META was up 20 days earlier in the year which coincided with the market peak so I am watching this name closely as a tea leaf for market/tariff safe haven exhaustion).

Stock picking in this environment comes down to picking spots where you can feel more comfortable adding gross. For example — as we wrote on Friday — one has to ask why go long AMZN with significant 2H tariff/China risk, when you can just go long MSFT: