TMTB Morning Wrap

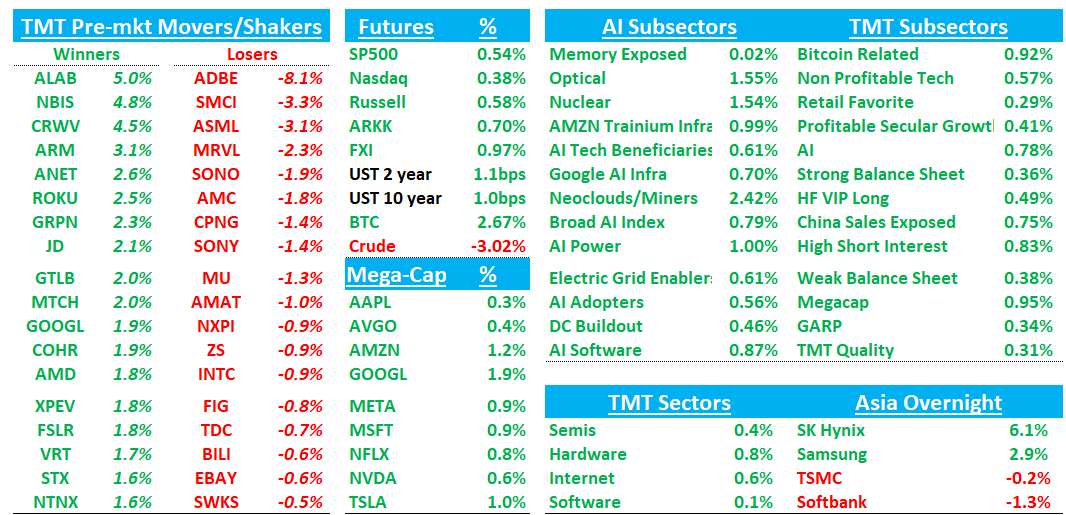

Happy Friday. Futures +30bps building on the strength yesterday as Oil -3% on the backs of continued optimism on a potential deal with Iran.

Asia generally green overnight: TPX +1.35%, NKY +2.81%, Hang Seng +1.93%, HSCEI +1.91%, SHCOMP +1.12%, Shenzhen +0.99%, Taiwan TAIEX +2.36%, Korea KOSPI +4.63%. SK Hynix +1%; Samsung +6%; Kioxia +8% (largest market cap in Japan now, beats out Toyota).

In Tech, some hyperscalers strength early with AMZN, META and GOOGL +1-2%. Some strength in ALAB, NBIS, CRWV (all +5%) as they get added to Nasdaq 100. ADBE -8% on organic growth and strategy shift concerns which are just fueling the competition bear fears. We cover it all below, starting with ADBE.

Let’s get to it.

ADBE -8%: Beat and raised FQ2 revenue/EPS guidance, but narrative worsened as FY26 organic ARR was effectively cut by ~$480-500M as mgmt prioritized freemium MAU growth over near-term monetization; CFO leaves (on top of unresolved CEO search)

Not much else to say on this one than the above. Organic growth the main nit that will fuel AI disruption/competitive fears despite an otherwise decent set of numbers against low expectations going in. Mgmt is essentially rebalancing traffic away from direct-to-paid journeys toward freemium (Firefly, Express, Acrobat AI Assistant), explicitly trading short-term ARR for MAU growth and LTV. Mgmt said the ARR impact is roughly split: about half from deferring Creative Cloud line optimizations/pricing and half from going “full steam” on freemium. Plenty of bear fuel. More details below:

The #s:

Revenue was $6.618B, +12.7% y/y (last q +12.0%) vs Street $6.454B, +~10%, and EPS was $5.96 vs Street $5.82.

The guide was optically fine on revenue/EPS, with FQ3 revenue $6.67-6.72B vs Street $6.516B and FY26 revenue $26.50-26.60B vs Street $26.06B.

Main negative ARR: total FY26 ARR growth stayed at 10.2%, but now includes ~$480M Semrush ARR, implying organic ARR growth was lowered by roughly ~190-200 bps.

AI metrics good; AI-first ARR > $500M, ~3x y/y, Firefly ARR approaching $300M, and creative freemium MAUs >90M, +70% y/y, but investors remain focused on whether that converts to paid ARR fast enough

Key Takeaways:

Mgmt is rebalancing traffic away from direct-to-paid journeys toward freemium (Firefly, Express, Acrobat AI Assistant), explicitly trading short-term ARR for MAU growth and lifetime value. Mgmt deferred previously planned 2H Creative Cloud "line optimizations" (pricing/packaging), removing a known growth lever for FY26. The combined hit is ~$480-500M (~2pp) to organic FY26 ARR, split roughly half pricing deferral, half freemium. On the callback, mgmt emphasized that the freemium shift is intended to access more demand, not simply defend against AI competition; creative traffic grew 50%, freemium MAUs accelerated to 70% y/y from 50% last q, and mgmt is more confident because usage is expanding beyond basic generation into editing, video and production workflows

FY26 total ARR growth held at 10.2% but now includes ~$480M of Semrush, so organic ARR growth falls to ~8%, implying organic NNARR down ~20-25% y/y in 2H. ARR will also skew more to 4Q than the historical ~40/60 3Q/4Q split, since changes begin implementation in 3Q.

FY26 non-GAAP OM ~45% maintained (Q3 ~44%, slightly below Street); mgmt was explicit it will not be short-term on spend (models, marketing, product). Per the callback, the freemium model is structurally more expensive and cost to acquire a dollar of ARR is rising.

AI metrics were the bright spot: AI-first ARR >$500M, ~3x y/y (~2% of total ARR); Firefly ending ARR approaching $300M, ~+50% q/q via apps and credit packs; Acrobat AI Assistant paid MAU +150% y/y; CXO AI-first ARR 4x y/y; generated assets in Firefly Enterprise +4x y/y; credit consumption driven by video/audio.

Engagement/funnel data is accelerating: adobe.com traffic +40% y/y (creative traffic +50%), Acrobat/Express MAU >850M (+20% y/y), creative freemium MAU 90M, +70% y/y (accelerating from +50% in 1Q). Mgmt argued LLM-driven, intent-based search is structurally changing user acquisition.

Mgmt still sees Creative Cloud pricing/line optimization as available later, but the decision to defer planned 2H actions while expanding freemium will make bears argue that ADBE’s ability to push price in creative/prosumer/SMB is deteriorating.

CFO Dan Durn is leaving (to become Marvell’s CFO); Steve Day (20-yr ADBE veteran) is interim CFO. No CEO successor named yet; goal is to have the next CEO in place to “put their stamp” on FY27 planning. CEO hire is prioritized ahead of the CFO hire.

. The lower 2H organic ARR outlook was described as roughly 50/50 between less pricing contribution and a harder freemium push, with benefits expected to show up in FY27 and more detail expected later on MAU/free-to-paid conversion. Pricing remains part of the growth algorithm, but mgmt does not want pricing to be the message while trying to capture heightened AI/LLM-driven traffic; guidance methodology was described as unchanged despite CEO/CFO transition, with more ARR expected to land in FQ4 than usual.

Bull vs. Bear Debate

Bulls start from the premise that ADBE remains one of the highest-quality franchises in software: ~97% subscription mix, ~90% gross margins, ~45% operating margins, $10B+ of annual FCF, and entrenched positions across creative tools, PDF, and the marketing/content supply chain. They argue this quarter actually delivered the AI proof points skeptics demanded: AI-first ARR tripled y/y to >$500M, Firefly ARR is approaching $300M with apps/credit packs up ~50% q/q on top of +75% last quarter, Acrobat AI Assistant paid MAU grew 150%+, and credit consumption is being driven by compute-heavy video and audio. The freemium pivot, in bulls’ view, is offense rather than defense: AI and LLMs are generating an explosion of high-intent search traffic (adobe.com traffic +40%, creative traffic +50%, freemium MAU +70% y/y and accelerating), and ADBE is replaying the Acrobat Reader playbook that built one of software’s most durable monetization funnels, this time with proven infrastructure for paywall placement and conversion. Bulls also point to the enterprise as a structurally underappreciated asset: AEP + apps growing 30%+, GenStudio 25%+, CXO AI-first ARR up 4x, 1,500+ agentic trials, and agency holding companies standardizing on ADBE. Add in commercially safe models (a differentiation sharpened by the Disney/Universal suit against Midjourney), distribution of Creative Agent inside ChatGPT, Claude, Copilot and Gemini, and Semrush extending ADBE into brand visibility/GEO at exactly the moment CMOs care about LLM placement, and bulls see a company repositioning from a position of strength.

Bears read this quarter as confirmation of the structural thesis: when AI natives (Canva, Midjourney, Runway, Synthesia, Gamma, HeyGen) and frontier labs are scaling rapidly in consumer/SMB creative, a company that simultaneously defers price increases and gives more product away for free is, by definition, losing pricing power. The freemium pivot may be framed as offense, but bears note the inconvenient math: total NNARR still declined y/y despite AI-first ARR tripling, meaning AI gains are not yet offsetting core erosion, and the ~10pp increase in AI's share of TTM NNARR is happening inside a shrinking pool. Organic FY26 ARR growth now sits around 8% with 2H organic NNARR implied down ~20-25% depending on the quarter, the 2H is more back-end loaded into 4Q than usual (raising execution risk), and freemium is structurally more expensive: mgmt itself acknowledged the cost of acquiring a new dollar of ARR is going up, while leading AI labs are moving toward paid monetization just as ADBE moves the other way. Bears also question why this freemium-to-paid motion reignites growth in an era of rising commoditization at the low end, and worry about cannibalization of paid Creative Cloud seats and eventual margin drift below 45% as inference costs and S&M intensity rise.

Layered on top is an execution/credibility problem: the CEO and CFO are both departing within a quarter of each other with no permanent successors named, guidance philosophy is unchanged but the people who built it are leaving, and any new CEO is likely to rebase FY27 expectations, meaning Street numbers (~8-9% revenue growth, ~$26.5-27 EPS) may still be too high. With limited near-term catalysts until a new team is in place and freemium conversion data arrives (mgmt says FY27), bears will say "show-me" story where the multiple is a value trap, not a floor.

TECH RESEARCH/NEWS

AMD: Citi Upgrades to Buy, Sees Agentic AI Driving a Larger CPU TAM and Meaningful GPU Upside

Citi upgraded AMD to Buy and raised its PT to $575, arguing investors are underestimating both the CPU opportunity created by agentic AI and AMD’s position in custom AI accelerators. The firm now forecasts the server CPU TAM reaching ~$137B by 2030, up from ~$132B previously, as agentic workloads increasingly shift orchestration, reasoning, memory management, and tool-use functions toward CPUs. Citi also believes Meta could become a significantly larger AMD customer than currently expected, with custom MI450 deployments potentially translating into ~$15B of revenue. Against this backdrop, Citi raised CY26/27 EPS estimates 12%/13%.

ALAB, CRWV, NBIS, RKLB and TER will be added to Nasdaq 100

SPCX: Wolfe Initiates Outperform, Says the Real Bet Is Starship, Not the 2035 Targets

Wolfe initiated SPCX at Outperform with a $175 PT, arguing investors do not need to believe the company’s long-term space datacenter ambitions to own the stock—they simply need to believe in Starship. The firm views SpaceX’s near-zero launch-cost advantage as one of the strongest competitive moats in any industry, enabling growth across Starlink, launch services, communications infrastructure, and eventually AI-related opportunities. Wolfe expects Starlink EBITDA to exceed $90B and EBITDA-less-capex to surpass $70B by 2030, driven by continued subscriber growth and significant capacity expansion. While the longer-term AI and orbital compute opportunity remains highly speculative, the firm believes Starship’s successful commercialization alone can support substantial upside, making future AI infrastructure optionality effectively a free call option for investors.

U/APP: Morgan Stanley Says Direct Payments Could Become a Meaningful Earnings Tailwind for Mobile Ad Platforms

Morgan Stanley argues the shift toward direct payments in mobile apps and games is increasingly bullish for both U and APP as developers look to reduce app store fees and reinvest a portion of those savings into user acquisition. The firm estimates every 5% reduction in payment processing fees could drive ~19% upside to U’s 2027 EBITDA and ~5% upside to APP’s, assuming roughly half of the savings are redirected into marketing spend. Beyond the advertising benefit, Morgan Stanley also highlighted U’s new Commerce product, which could allow Unity to participate directly in payment processing economics, with every 10% penetration of global in-game transactions potentially driving ~20% upside to 2027 EBITDA.

NOK: JPM Raises PT to €18/$21, Sees AI Optics and Hyperscaler Switching Wins Driving Upside

JPM says Nokia generated €1B of AI and cloud orders in 1Q, with JPM expecting new optical products including 1.6T coherent pluggables, 3.2T solutions, and advanced transponders to drive further growth. The firm also highlighted datacenter switching wins with Microsoft and at least one additional hyperscaler, with Google viewed as a likely customer. JPM believes Street is not fully reflecting the revenue and operating leverage from Nokia’s optical and datacenter networking businesses, leaving its 2026-28 EBIT estimates meaningfully above consensus.