TMTB Morning Wrap

Good morning. Futures flattish. Oil -1.4%. Not a ton on the macro/geopolitical front overnight.

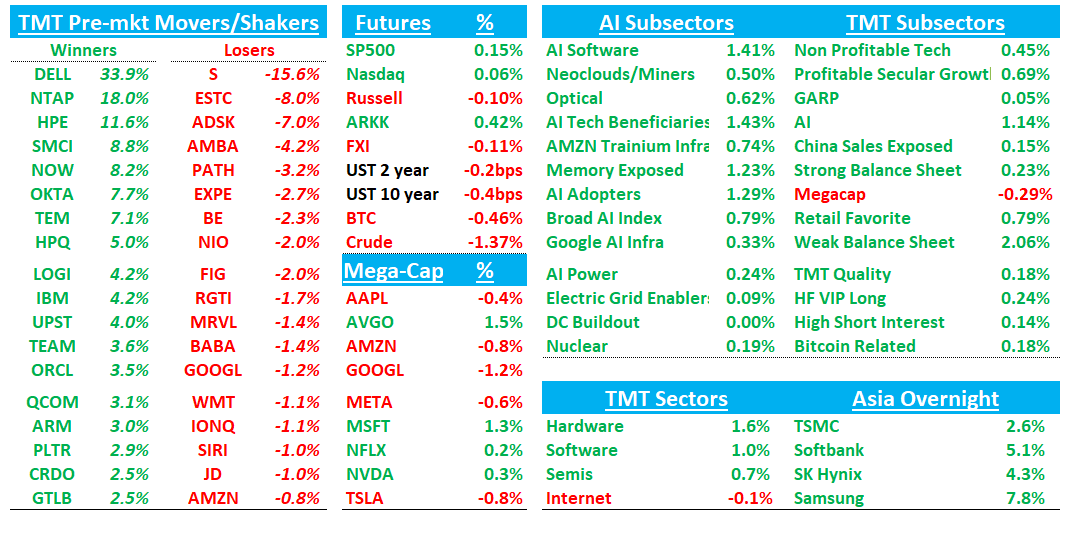

Asia mixed although many AI names in Korea and abroad ripped: TPX +1.41%, NKY +2.53%, Hang Seng +0.7%, HSCEI +0.73%, SHCOMP -0.73%, Shenzhen -1.9%, Taiwan TAIEX +2.51%, Korea KOSPI +3.55%. Samsung +8%; Hynix +4%; Softbank +5%

In Tech, Semis and software both up ~1% early while Internet lags.

We’ll hit up MDB and DELL first then get to the usual. We’ll have OKTA/NTAP recaps in the Slack.

Let’s get to it…

MDB +3%: Solid beat-and-raise, led by Atlas consumption and a better EA quarter, but narrative debate is now whether EA growth can outweigh Atlas Decel

Overall, print was solid with Atlas 29% slightly missing 30% bogey but above street of 26%. Q2 Atlas guide 26% vs bogeys of 25%. Wild ride in the aftermarket last night as stock went from down 20% on the print as Atlas was slightly below bogeys, then rallied 45% in 20 minutes as Q2 came above, then sold down as CFO’s forward commentary wasn’t received well: “We would encourage you to not expect large swings vs guidance for the current quarter as changes in consumption into quarter only have a modest impact on revenue within the period.”

Some debate around exactly what he meant but largely consensus taking it to me likely a smaller beat than Q1 and more in the Q4 range of a 2% Atlas beat which would imply 28%. All-in all we don’t think the numbers set up is all that bad as it would imply Atlas growth will only decel from 29% to 28% over the course of 2 quarter when comps got 5ppts tougher. The comp flattens out after this quarter, so it’s possible we see a re-accel in Q3 to something with a 3-handle when street is expecting a decel to low 20s and guide for 23-25% for the full year.

Overall, we think this was a solid print, the stock’s likely path is up, and the set up going forward is decent to good, but think narrative around DDOG and SNOW better in the AI consumption space.

The #s:

Q1: Revenue was $687.6M, +25.2% y/y (last q +26.7% y/y) vs Street $664.5M, +~21%, with Atlas $512.5M, +29.4% y/y (last q +29.2%) vs Street ~$499M, +~26%. Non-GAAP EPS was $1.32 vs Street $1.19, and FCF was $197.5M, 28.7% margin vs Street ~$125M

Q2: Rrevenue guide of $729–$734M, +23–24% y/y vs Street ~$700.5M, +~18.5% was meaningfully ahead, while FY27 revenue guide was raised to $2.92–$2.96B, +19–20% y/y vs Street ~$2.89–$2.90B, +~17–18%

FY27 Atlas growth guide was raised to 23–25% from 21–23%

Key Takeaways:

Mgmt highlighted frontier labs, AI-native customers, Voyage customers more than doubling q/q, MCP usage growing significantly, and vector search adoption far outpacing company growth. Still, mgmt said current results are driven primarily by core workloads, not AI.

EA & Other grew 13% y/y, with EA/Other ARR up ~11%, and Q2 EA/Other is guided to ~20% y/y due to ARR momentum and large multiyear deals. This is impt because bears historically focused on Atlas only, while bulls now have a second pillar in EA, hybrid deployments, and federal.

Non-GAAP OM was 17.9% vs Street ~16.4%, FCF margin was 28.7%, and FY27 guidance targets 20% revenue growth and 20% OM at the high end, implying Rule of 40.

In the callback, mgmt emphasized that the majority of Atlas strength came from core enterprise workloads, while frontier labs and AI natives are beginning to contribute. The more incremental AI points were persistent memory use cases at a frontier lab and multiple AI-native customers, plus a Fortune 50 customer with six customer-facing agents in production. The FY27 raise was described as primarily Atlas-driven, while Clarity adds roughly $5–6M in FY27 contribution and C-suite changes were not seen as disruptive. EA guidance moved from low-single/low-to-mid-single digit to mid-single digit, helped by longer-duration deals in Q2, but 2H remains constrained by tough compares.