TMTB Morning Wrap

TMTB Vacation schedule:

This is the last post of the week.

Only Morning Wraps next week June 29th through July 2nd

No posts July 20th - July 24th

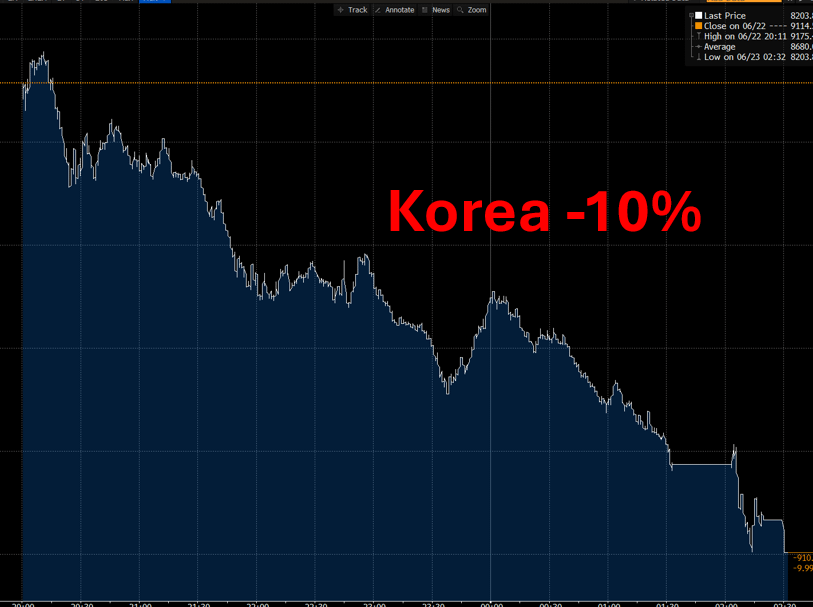

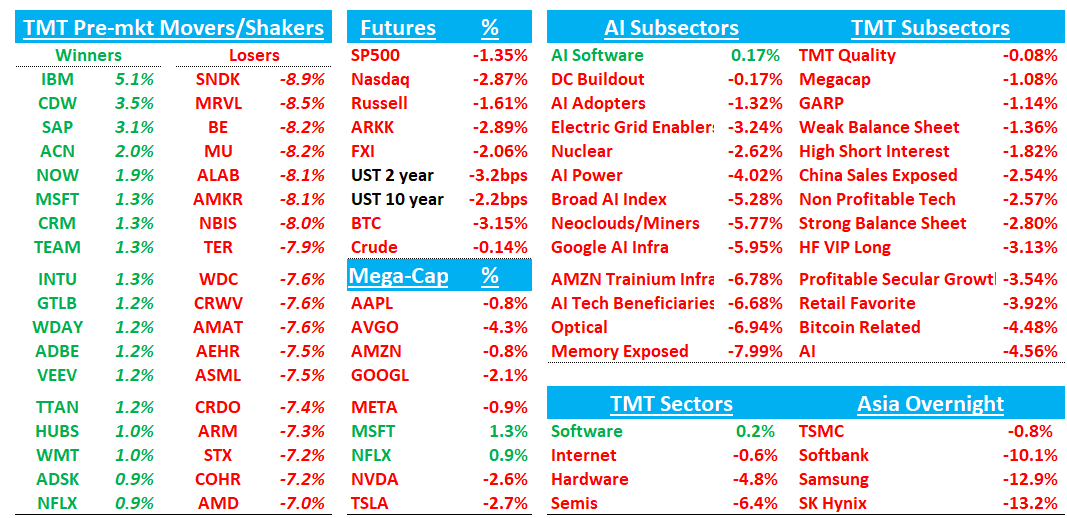

Good morning. Futures -3% to start the day following a big move down in Korea overnight which sold off all day from start to finish.

Hynix -13%. Softbank -10%. Kioxia -10%. Samsung -13%. Big volume in those names overnight with some hitting notional volume records. Chart, leverage, sentiment, and retail participation obviously very extended and some also pointing to comments by lawmakers proposing to transition to a comprehensive income tax system that recognizes unrealized gains as income.

In Tech, semis -6%+ following Korea lower. What’s been strong lately is down the most: Memory -7-8%; MRVL/ALAB -8%, BE -7% and so on…Nothing being spared in the sea of red.

Software +30bps is in the green with IBM +5% leading the way higher after a JPM upgrade and what’s been weak there recently - mainly app sw - is up early as we are seeing some Mo unwind.

Let’s get to it…

IBM: JPM Upgrades on Growing Confidence in Software Reacceleration and Margin Expansion

JPM upgraded IBM to Overweight, arguing investors are underestimating the company’s ability to accelerate software growth in 2H26 and beyond. The firm sees multiple catalysts, including stronger AI adoption, OpenShift momentum, continued automation demand, Red Hat growth, and revenue synergies from the HashiCorp and DataStax acquisitions, while consulting becomes less important to the overall story. JPM believes software’s higher-margin, recurring-revenue profile can drive faster earnings growth than the market expects, with room for both estimate revisions and multiple expansion as IBM continues its transition toward a software-centric business model.

Trump was also out during the day on Monday

CDW: Morgan Stanley Upgrades on Underappreciated Server and AI Infrastructure Demand

Morgan Stanley upgraded CDW to Overweight, arguing enterprise server demand is proving far more resilient than expected as compute shortages, refresh cycles, and AI infrastructure deployments continue to drive spending. The firm views CDW as one of the cleanest ways to play accelerating server demand and believes concerns around broader IT spending weakness are overstated. Morgan Stanley expects positive estimate revisions to return in 2H26 as investors increasingly recognize the durability of infrastructure demand and CDW’s leverage to the ongoing AI buildout.

SNPS: Piper Upgrades on Intel Foundry Momentum and a Faster-Than-Expected IP Recovery

Piper upgraded Synopsys to Overweight and raised its PT to $550, arguing the setup for the IP business has improved materially as Intel’s 18A and 14A nodes gain credibility. The firm believes Intel’s emergence as a viable alternative to constrained TSMC capacity could drive a meaningful rebound in design activity at Synopsys’ largest IP customer, with potential upside from both Google’s reported TPU production plans and Apple’s interest in using Intel Foundry for future devices. Piper sees the market underestimating the pace of an IP recovery, with renewed Intel foundry activity and future customer agreements creating a more favorable demand environment than investors expected just nine months ago.