TMTB Morning Wrap

Good morning. Futures flattish. Yields and Oil down slightly. On the geo-political front, Trump said talks continue at a “rapid pace”, “there will be no Troops going to Beirut, and any Troops that are on their way, have already been turned back”, “I had a very good call with Hezbollah, and they agreed that all shooting will stop — That Israel will not attack them, and they will not attack Israel”, and oil will “drop like a rock in the near distance.”

Asia saw mixed price action: TPX -0.43%, NKY -0.3%, Hang Seng +2.52%, HSCEI +3%, SHCOMP +0.43%, Shenzhen +0.77%, Taiwan TAIEX +0.48%, Korea KOSPI +0.15%. Memory names strong: Kioxia +7%; Samsung +3%; Nanya +10%. In China, optical theme had a strong rebound today with YOFC +10%, Hengtong +10%, Zhongtian +9%, Dongshan +10%, Eoptolink +10% and Innolight +5%.

Tencent+10% on launching their AI agent, helping BABA/BIDU/VNET/GDS all up early.

In Tech, semis +2% while software -3% taking a breather. MRVL +18% as Jensen said it would be the next Trillion dollar company on stage yesterday. Optical and Copper names up early while, the latter on the back of some positive comments on stage from Jensen yesterday (below the fold)

BAML’s big TMT conference starts today (line up below).

Lots to get to, so lets get to it…We’ll hit HPE/CRDO first then the usual…

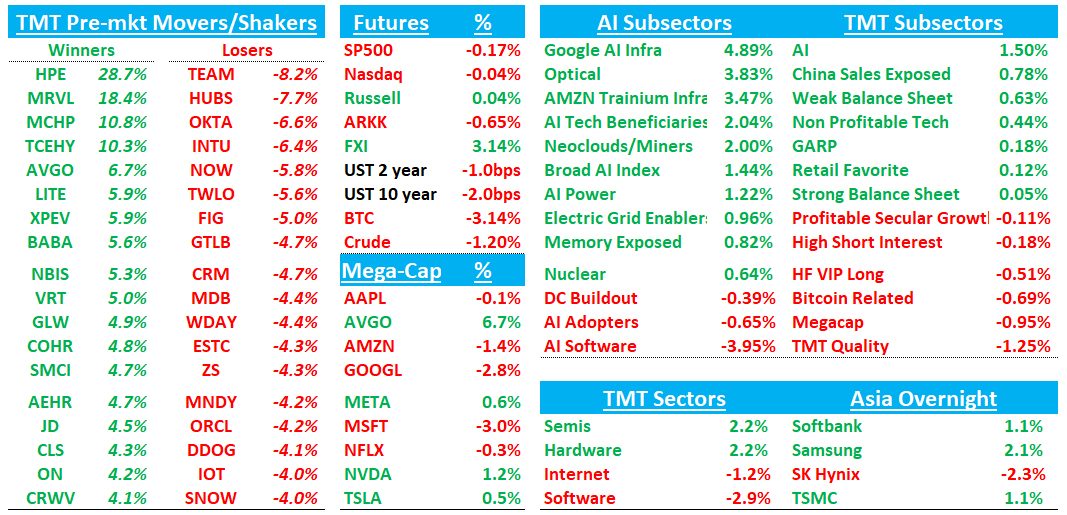

HPE: Huge beat/raise across the board as AI-inference-led server demand, strong orders, pricing, Juniper synergies and FCF visibility drove a much higher FY26/FY27 earnings/rev guide

Big beat on topline and EPS: Revenue was $10.678B, +40% y/y (last q +18% y/y) vs Street $9.78B, +~28% y/y; EPS was $0.79 vs Street $0.53; non-GAAP OM was 13.3% vs Street ~10.6%.

Raised FY26 guide by $1+ for FY26 $3.35-$3.45 from $2.30-$2.50

Initial outlook for FY27 well above street and bogeys as well at 8-12% vs street at 5%.

Just massive numbers which will give mgmt a lot of credibility and be a big boon to bulls who have thought this deserves a much higher multiple. Bulls likely going to $4+ in 2027 from $3. 15x = $60+ right where stock is. Bulls will say this is a new HPE which deserves something closer to high teens/20x. We still need to give some thought about what multiple to give it — we sold ours in the mid 30s thinking stock was near full at 12x $3, we were clearly wrong on both multiple and magnitude of upside so soon.

Key Takeaways:

Mgmt said orders more than doubled y/y and outpaced revenue, producing record backlog. This broadens the story beyond one quarter of pricing: AI systems, traditional servers, storage, Campus & Branch, DC networking and routing were all called out as strong.

Mgmt stated he pipeline remains multiples of the current record backlog, and all guidance reflects only secured supply allocations, with any improvement in supply availability representing potential upside to ‘27 guidance. They said they explicitly see no evidence of pull-in orders or cancellations. Across both Cloud & AI and Networking, mgmt described constraints in memory, NAND, DDR4/DDR5, wafer capacity and broader component availability. The FY27 guide embeds current supply assumptions, leaving potential upside if supply unlocks

Gross margin was 36.9% vs Street ~34%, and OM was 13.3% vs Street ~10.6%. Mgmt credited mix, pricing, Catalyst savings and Juniper synergies, while also saying FY27 Networking margin expansion should benefit from a full-year Juniper synergy run-rate.

Server revenue was $5.454B, +33% y/y vs street ~$4.666B, with traditional server revenue $4.197B, +35% y/y vs est. ~$3.445B. Mgmt highlighted triple-digit traditional server order growth as customers modernize compute infrastructure and deploy agentic AI / inferencing workloads.

The quarter benefited from higher ASPs driven by DRAM/NAND inflation and supply constraints, but mgmt said units were up slightly and should improve as pricing and unit mix rebalance. Bears will still ask whether customers are pulling forward server refreshes before more price hikes, while bulls will point to mgmt commentary that there is no pull-in, no demand cliff and no cancellation/double-ordering signal.

AI systems orders were $1.8B, cumulative AI systems bookings reached $16.4B, and AI systems backlog was $5.9B, primarily enterprise and sovereign. Mgmt framed inference as a new, growing market that uses both GPUs and CPUs, supporting both accelerated servers and traditional CPU servers.

Networking revenue was $2.690B, +148% reported and roughly +10% normalized, essentially in line with Street, but orders outpaced revenue. Networks for AI order guidance was raised to at least $2B by FY26 year-end, and the story is shifting toward HPE/Juniper scale-up, scale-out and scale-across AI networking