TMTB Morning Wrap

Good morning. Futures +1.3% despite some fire between Iran and US overnight as media reporting negotiations are still containing as efforts to reach a deal are intensifying. Oil -1% as yields tick down 2-4bps across the curve.

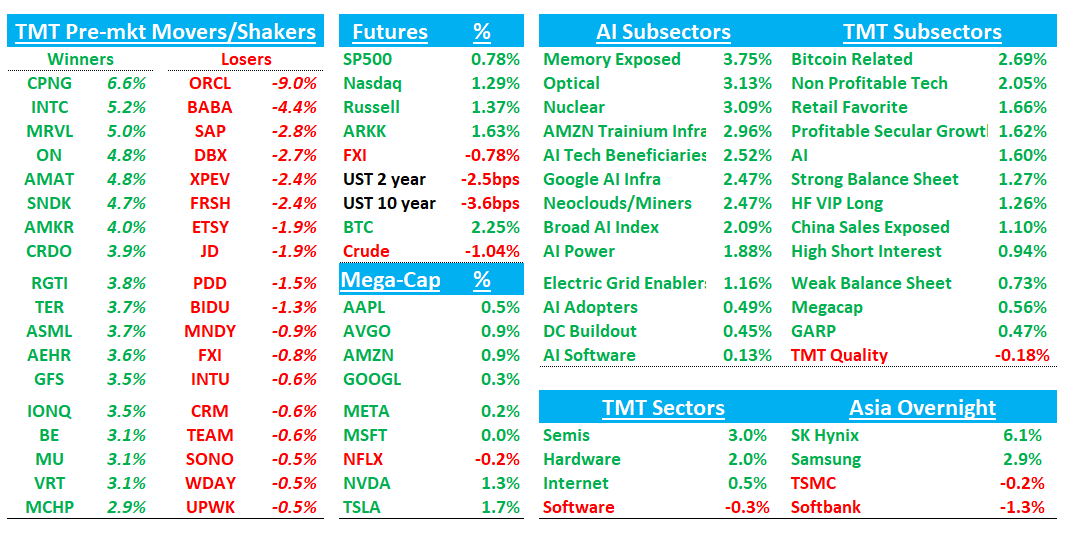

In Tech, semis are leading the way higher with INTC (+5%) up on a dbl ug at BofA, Memory following Asia strength overnight (SNDK/MU +3-5%), and semicaps looking to be the first AI semi group to be regaining 52wk highs (ASML/AMAT +5%). ORCL -5% as print did nothing to change the bull/bear debate although bears had more fuel this morning with the IaaS miss and lack of FY27 raise. Apps missed as well which has software underperforming early.

In Asia, mixed px action: TPX -0.45%, NKY +0.06%, Hang Seng -0.65%, HSCEI -1.22%, SHCOMP -0.16%, Shenzhen -0.66%, Taiwan TAIEX -0.18%, Korea KOSPI +0.43% but Samsung +3%, Kixoia +4% SK Hynix +7%.

SpaceX (SPCX) starts trading tomorrow (we have some Starlink 3p data below).

Lots to get to so let’s get to it…

ORCL -8%: Solid AI-infra/RPO quarter with better revenue, EPS and OM, but IaaS missed buyside bogeys, and debate continues between accelerating OCI visibility and concerns on unchanged FY27 revenue guide, SaaS decel, & FY27 GM/capex and financing.

The #s:

Revenue was $19.184B, +20.6% y/y / +20% CC (last q +21.7% / +18% CC) vs Street ~$19.10B, +~19.5-20%; EPS was $2.11 vs Street $1.96; non-GAAP OM was 44.8% vs Street ~43.3-43.5%.

Cloud was $9.913B, +47% y/y / +46% CC, slightly below Street, with OCI/IaaS $5.787B, +93% y/y / +92% CC vs Street roughly low-90s growth and buyside in mid 90s, while SaaS/Cloud Apps slowed to $4.126B, +10% y/y / +9% CC vs Street closer to low-teens.

RPO was the stock-moving standout at $638B, +363% y/y, up $85B q/q vs Street around $577B, with $67B of AI infra contracts signed and BYOH/prepaid commitments now $75B.

F1Q27 guide was above Street: revenue +27-29% y/y, cloud +58-64% USD / +57-63% CC, EPS $1.72-$1.76 vs Street ~$1.68-$1.69;

FY27 revenue guide stayed $90B, +34%, above Street but unchanged, and EPS guide moved to $8.05. FY27 capex of $90-95B was well above Street (~$62-85B range), though net cash capex of ~$70B (after $20-25B of customer prepays) was in line to slightly better than feared.

Key Takeaways:

RPO was $638B, +363% y/y, up $85B q/q, and cRPO accelerated to +68% y/y from +65%. The RPO add was driven largely by AI infra contracts, including four customers signing $8B+ deals, while reports also noted a base of smaller $100-$300M deals, which helps push back on OpenAI-concentration concerns. 12% of RPO converts to revenue in the NTM (implying cRPO of $76.6B, +68% y/y), 34% in months 13-36, with both percentages expected to rise as capacity ramps.

The majority of Q4 bookings were prepaid or bring-your-own-hardware; these now total $75B of RPO with "no degradation in margin," some at better gross margins and meaningfully higher ROIC (mgmt cites high-20s ROIC at steady state). Customer prepays cut FY27 net cash capex to ~$70B vs $90-95B reported.

ORCL delivered >1.2GW in FY26 and expects F1Q27 delivery approaching 1GW, nearly the same as the prior four quarters combined. Abilene is 42% delivered with another 35% expected in the next 90 days, and several large sites are scheduled for 1H/2H CY27 delivery.

ORCL plans ~$40B of FY27 debt/equity raises (including the $20B ATM), no incremental debt in CY26; credit metrics improved q/q (gross/net leverage 3.5x/2.7x) and bonds rallied ~10bp even as the stock fell.

Margins were mixed: OM beat, GM pressure remains the FY27 overhang. F4Q non-GAAP OM beat on opex discipline, but gross margin compressed as OCI/AI infra mix rose. Mgmt guided FY27 gross margins lower due to data-center ramp timing and mix, while saying infra margin should improve rapidly as sites hit full contractual revenue levels.

Apps grew +9% CC, down from +11% CC last q and below Street, which keeps the “SaaSpocalypse”/AI disruption debate alive. Mgmt pushed back by pointing to +16% SaaS deferred revenue, AI agents embedded in apps, Oracle Health/VA deployment momentum, and a new OPM Fusion HCM award not in Q4 bookings.

Mgmt sees AI infra demand "massively higher" than supply with a trillions-per-year market; agentic coding demand shows "no slowdown." On SaaS, the "SaaSpocalypse" delayed decision cycle of two quarters ago has passed, with SaaS deferred revenue +16% y/y (faster than revenue) signaling re-acceleration; new token-bundle and outcome-based pricing launched to monetize agents.

Bull vs. Bear Debate

Bulls see ORCL as one of the clearest large-cap software beneficiaries of AI infra demand, with a unique combination of contracted backlog, database ownership, applications, multi-cloud distribution and a capacity ramp that is now becoming visible. The $638B RPO, up 363% y/y and up $85B sequentially, gives near-contractual visibility into a 30%+ revenue CAGR through FY30, and this quarter's $67B of bookings demonstrated both scale and improving diversification (four customers at $8B+ each, plus a long tail of $100M-$300M deals, with concentration declining vs a few quarters ago). Execution is matching the demand: 1.2GW delivered in FY26, ~1GW coming in F1Q27 alone, all five major sites on or ahead of schedule, capacity sold out for six months and 97.5% GPU utilization. Critically, the BYOH/prepaid model ($75B of RPO) answers the two biggest historical pushbacks, financing risk and returns, since these deals carry equal-or-better gross margins, high-20s steady-state ROIC (higher on prepaid structures), and cut FY27 net cash capex to ~$70B with only ~$40B of funding needed and no new debt in CY26. That gives bulls confidence that OCI growth can sustain or even exceed 100% as sites turn on, especially with Abilene and other named data centers moving toward delivery.

Bulls also argue the capex debate was partially de-risked. The reported FY27 capex number is large at $90-$95B, but net cash capex of ~$70B is lower than feared by some investors, and BYOH/prepaid structures move part of the capital burden to customers while preserving similar or better margins. The bull narrative is that ORCL is not just renting GPUs at poor returns, but is building a high-ROIC infra business with embedded database and application pull-through. Multi-cloud database revenue growth of 404% and bookings growth of 325% reinforce the idea that ORCL’s installed database base becomes more valuable in an AI world where proprietary enterprise data matters.

Bears argue the backlog is impressive but increasingly disconnected from the P&L: despite adding $85B of RPO in a single quarter, ORCL did not raise the $90B FY27 revenue guide, the Q4 revenue beat was just $81M (under 1%) vs $300M+ a year ago, and only 12% of RPO converts over the next twelve months. The structural concern is that ORCL is transforming from a 70%+ gross margin software franchise into a capital-intensive GPU landlord: gross margins have now compressed y/y for 20 consecutive quarters, FY27 GMs step down further, AI infrastructure tops out at 30-40% gross margins, and FY27 EPS grows only ~5-6%. Meanwhile, the cash demands are enormous: $90-95B of reported FY27 capex (2H26 capex roughly equaled net income), FCF negative through at least FY28-29, $40B of new financing including $20B of dilutive ATM equity, ~3.5x gross leverage, plus counterparty risk to AI labs, GPU obsolescence/depreciation risk, and rising competition from hyperscalers and neoclouds for the same capacity. Layer on the apps business decelerating to 9% cc (NetSuite SMB softness, tougher compares, lingering AI-disruption fears about seat-based SaaS), and bears see a company taking on hyperscaler-level risk without hyperscaler-level cash generation.

TECH RESEARCH/NEWS

INTC: BofA Double-Upgrades to Buy, Sees Much Larger CPU and Foundry Opportunity Emerging

BofA double-upgraded INTC to Buy and raised its PT to $135 from $96, arguing investors are materially underestimating both Intel’s long-term CPU opportunity and the value of its foundry business. The firm now models server CPU revenue exceeding $40B by 2030, driven by the expansion of the CPU TAM in an agentic AI world, while also seeing a $45B+ external foundry opportunity spanning Apple M-series production, MediaTek AI accelerators, custom CPUs, edge AI, and advanced packaging. BofA believes recent datapoints—including improving 18A execution, the CDNS 14A partnership, and Terafab-related engagements—support higher confidence in Intel’s IDM strategy. BofA thinks Intel’s earnings power and foundry optionality are increasingly visible, with BofA now modeling CY30 EPS potential above $6 and arguing ownership remains unusually low relative to the scale of the opportunity.

CPUs/AMD/ARM: BofA Raises Server CPU TAM to $170B, Says Agentic AI Fundamentally Expands the Opportunity

BofA argues agentic AI is creating a structural renaissance for CPUs, raising its CY30 server CPU TAM estimate to $170B from $125B as AI workloads increasingly require planning, orchestration, reasoning, memory management, tool use, and other sequential tasks that are better suited for CPUs than accelerators. The firm believes agentic AI shifts part of the value creation from GPUs/XPUs toward CPUs, creating a new standalone agentic CPU opportunity while also increasing demand for head and compute-node CPUs within AI clusters. Against this backdrop, BofA raised targets across CPU-exposed names, double-upgraded INTC to Buy, remains constructive on AMD and ARM, and continues to view NVDA as the top overall AI beneficiary.

OpenAI: OpenAI Considers Drastic Price Cuts, Anticipating War for Users With Anthropic

WSJ:

The company is weighing significant cuts to what it charges for tokens, the unit of measurement artificial-intelligence firms use to bill for their products, according to people familiar with the matter. The move would be in anticipation of similar cuts the company expects at Anthropic, the people said.

Business executives have begun to balk at the high prices for AI usage. OpenAI Chief Executive Sam Altman said at a recent event that costs had become “a huge issue.”

“I think we’ll have a lot of ways we can help people get more value for less spend,” he said.

SpaceX (SPCX) starts trading tomorrow:

3P check: According to Apptopia, Starlink growth is accelerating in Q2 and continually hitting monthly download highs; June is on pace to be another new high: