TMTB Morning Wrap

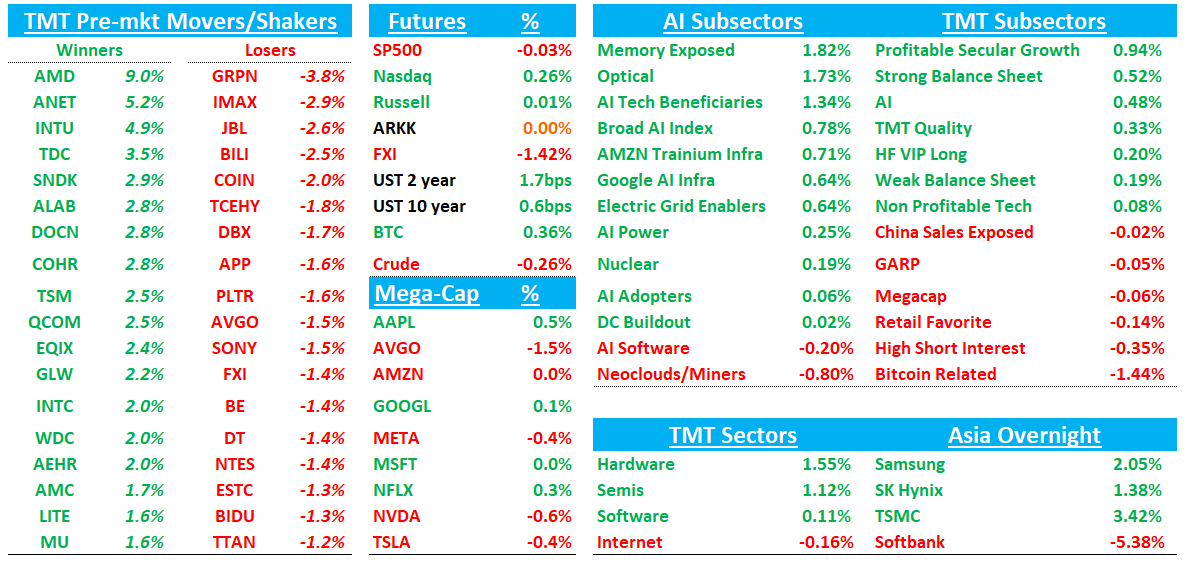

Good morning. Futures +30bps as all eyes still on NVDA tomorrow. Big META/AMD +10% deal today. Asia mixed with China down but Korea up: TPX +0.2%, NKY +0.87%, Hang Seng -1.82%, HSCEI -2.06%, SHCOMP +0.87%, Shenzhen +1.23%, Taiwan TAIEX +2.75%, Korea KOSPI +2.11%. Softbank -5%. TSMC +3%. BTC -2%

Bernstein Conference starts tomorrow. Agenda Here

Anthropic also at 930am ET today: Webinar to focus on Claude’s agent capabilities for enterprise workflows.

Let’s dive straight in

META/AMD: Meta and AMD Agree to AI Chips Deal Worth More Than $100 Billion to Deploy 6GW

ANET +5% / NVDA -1%

They saying every 1GW is double digit AMD revs. Running some conservative #s: Per GW, $15B at 50% GM and 15% opex including 10% dilution you get ~$2.7 in EPS, so call it $15-$16 in EPS over 5 years with this deal.

PR:

This agreement expands on the companies’ existing strategic partnership and aligns roadmaps across silicon, systems and software to deliver AI platforms purpose-built for Meta’s workloads. The first deployment will use a custom AMD Instinct GPU based on the MI450 architecture to deliver AI platforms that are optimized for Meta’s workloads at gigawatt-scale. Shipments supporting the first gigawatt deployment are scheduled to begin in the second half of 2026 powered by the custom AMD Instinct MI450-based GPU and 6th Gen AMD EPYC™ CPUs, codenamed “Venice,” running ROCm™ software and built on the AMD Helios rack-scale architecture. AMD Helios was developed jointly by AMD and Meta through the Open Compute Project to enable scalable, rack-level AI infrastructure.

DOCN +3%: Solid beat and raise; 4Q25 Beat ($243 vs $238M and in line with bogeys); Bit FY27 guide of 30% accel from 21% but expectations high for one of the few loved names in sw. Margins a bit softer

Net ARR of $51M (accelerating vs. prior quarters at 16% and 14%).

Q1 FY26 Guide:

Revenue $249–$250M (vs. Street $248.1M)

Adj. EBITDA margin 36–37% (vs. 38.5% Street)

Non-GAAP EPS $0.22–$0.27 (vs. $0.45 Street)

FY26 Guide:

Revenue $1.075–$1.105B (vs. $1.066B Street) → ~20.9% y/y at midpoint

Adj. EBITDA margin 36–38% (vs. 39.1% Street)

Adj. FCF margin 15–17% (vs. 19.0% Street)

Non-GAAP EPS $0.75–$1.00 (vs. $1.96 Street)

Mgmt raised growth expectations to 21% y/y in FY26 and 30% in FY27, driven by AI momentum, significantly above prior 18–20% and ahead of buyside expectations.

BKNG: Morgan Stanley Upgrades to Overweight, PT Raised to $5,500; Sees OTAs Retaining Control in Agentic Era

Morgan Stanley upgraded Booking Holdings to Overweight from Equal Weight and lifted its price target to $5,500 from $6,150, arguing BKNG remains central to online travel even as agentic tools evolve. The firm contends OTAs will continue to own the customer relationship, data, and merchant-of-record economics, with early agentic workflows largely redirecting traffic back to OTA apps/websites rather than disintermediating them. MS expects the industry structure to remain closer to paid search dynamics, supporting BKNG’s direct mix and long-term margin profile.