TMTB Morning Wrap

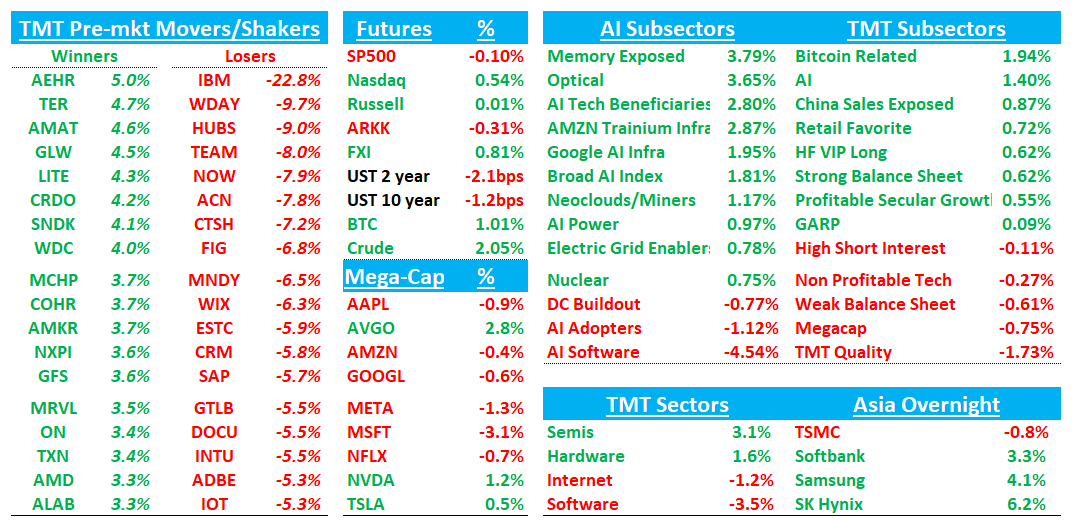

Good morning. QQQs +50bps in front of this morning’s CPI. Semis were already up early, but catching even more of a bid following IBM’s (-23%!) negative pre announcement which is taking down Software -3.5%. Here is the key quote from the IBM PR:

In the last few weeks of June, we saw purchases to secure supply-constrained infrastructure ahead of expected price increases. While we anticipated some supply chain related impact in our expectations, we did not anticipate the magnitude of the capex reprioritization. In addition, clients were distracted with rapidly-evolving, industry-wide cybersecurity concerns in the quarter.

The #s:

Revs $17.2B, vs street at $17.9B

Software Revs +5% y/y vs street at double digits

Consulting Revs flat vs street at +LSD

Infra Revs -7% vs Street at -1%

RHT accelerated to 11% the one bright spot

EPS: $2.93 vs street at $2.97

Lots of software names down high single digits, particularly those in the “AI loser bucket”: WDAY -9%, HUBS -9%, IT Services -8%, INTU -6%, etc…

IBM wasn’t the only one calling out higher component costs: ERIC -9% also lower after warning elevated component costs could pressure margins going forward…

In Asia, things were generally green: TPX +0.79%, NKY +0.74%, Hang Seng +0.52%, HSCEI +0.46%, SHCOMP +1.36%, Shenzhen +2.26%, Taiwan TAIEX -1.42%, Korea KOSPI +0.73%. Memory names higher with Samsung +4% and SK Hynix +6%. Softbank +3%.

Lots to get to so let’s get to it…

AAPL: KeyBanc Downgrades to Underweight as Hardware Growth Slows and Valuation Stretches

KeyBanc downgraded AAPL to Underweight from Sector Weight with a $250 price target, citing June hardware spending down 2% m/m and continued below-trend growth despite easier comparisons. The firm sees risks from slowing iPhone builds, weaker U.S. upgrades as carriers pull back subsidies, and softer Mac, iPad and Wearables expectations, while Services growth is also expected to decelerate to roughly 7% in FY27 versus Street near 12%. With AAPL trading around 24.5x FY27 EV/EBITDA and 35x P/E, KeyBanc believes the stock’s premium is difficult to justify absent a stronger hardware cycle or Services reacceleration.