TMTB Morning Wrap

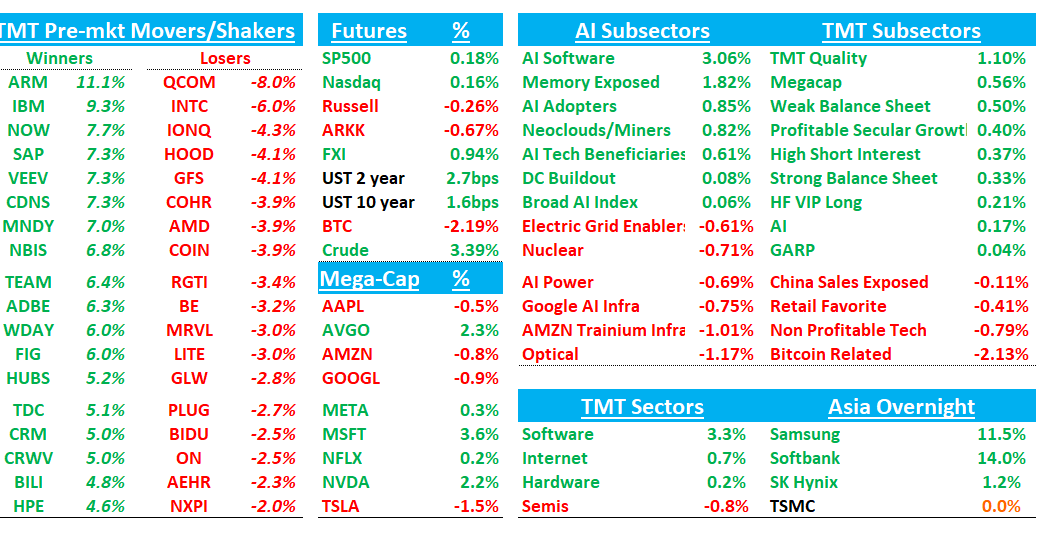

Good morning. Futures flattish as software +3.5% continues to squeeze higher at the expense of semis -80bps - software just had its best month in May since 2002 up 21 % (we had some thoughts on the move and what’s next in our weekly in case you missed it).

NVDA +2% announced they are entering the market with a new RTX chip, which has ARM +11% early and INTC -5%/AMD-4%/QCOM -9%. Memory the bright spot in semis while opticals continue to lag. Hyperscalers weak with GOOGL -1% following through on the neg 3p data from Friday while AMZN -1%.

Asia mixed but Korea continued to rip and many memory/robotics AI names up significantly: TPX -0.42%, NKY +0.91%, Hang Seng +0.86%, HSCEI +0.97%, SHCOMP -0.27%, Shenzhen -0.78%, Taiwan TAIEX +1.35%, Korea KOSPI +3.68%. Softbank +14%. Samsung +12%. Kioxia +8%

On the macro front, yields ticking up 2-3bps across the curve while Oil popping 3% as an Iran agreement continues to prove elusive.

In Tech, we have a busy week coming up with Earnings from AVGO, CRWD, CRDO, HPE, GTLB, PANW, CIEN, DOCU and more. Computex continues through the week with keynotes INTC’s Lip Bu Tan, and MRVL CEO. BAML’s and ISI’s TMT conferences start Tuesday as well as the William Blair Growth conf. We get SNOW and Kioxia Investor Days on Tuesday.

Lots to get to this morning, so let’s get right to it…

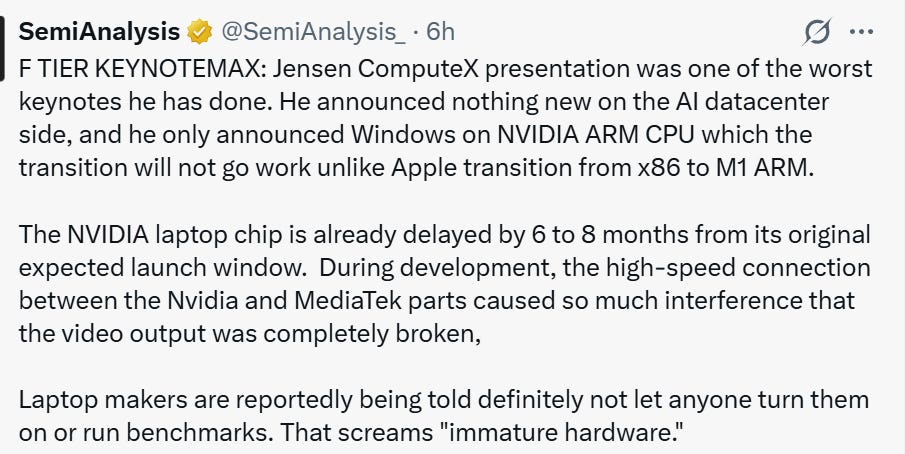

NVDA: Jensen speech at GTC quick notes

Key points are he said Vera Rubin is in full production, talked up CPU tailwind (Vera CPU 1.8x agentic sandbox performance vs. X86),and unveiled RTX Spark 3nm chip with Mediatek which offers up to 1 petaFLOP of local AI performance and 128GB of unified memory. He also announced a new opensource model Nemotron 3 Ultra, which is 5x faster and 30% cheaper than other leading open-source models including Kimi K2.6, Qwen 3.5, and GLM 5.1. Also said cost of AI DC will grow from $50B per GW to $80B per GW in coming years.

NVIDIA highlighted tokens have now become profitable, which is driving a significant demand for compute. Jensen further noted GitHub commits have increased nearly 3x in 2026 due to AI Coding tools improving the productivity of SW engineers. NVIDIA argues this will result in hiring more SW engineers as output per engineer is increasing

CDNS +7%: Cadence Unveils Industry’s First Fully Autonomous Virtual Engineer for Chip Design, powered by NVIDIA

PR:

At Computex 2026, Cadence (Nasdaq: CDNS) announced the industry’s first fully autonomous virtual agentic AI design engineer, extending the ChipStack™ AI Super Agent to Level-5 autonomy. Built on Cadence’s AI-driven electronic design automation (EDA) portfolio with NVIDIA Nemotron models, and secured by NVIDIA OpenShell runtime, the new agentic capabilities enable customers to run dynamic simulations in automated workflows

The company noted ChipStack can reduce verification cycles from weeks to hours (~40% reduction). NVIDIA noted it will hire 100s of thousands of ChipStack Agents

INTC: Intel targets new AI data centre chip by year end

Intel plans to ship an AI chip by the end of this year that uses cheaper memory and cooling technology than rival offerings from Nvidia and AMD, as the US chipmaker seeks to capitalise on a sharp turnaround in its fortunes. Kevork Kechichian, who leads Intel’s data centre group, told the FT that the company is “starting with the basics” as it tries to challenge its rivals in the booming market for semiconductors that power AI. Its new “Crescent Island” graphics processing unit is designed to speed up “inference” tasks, the stage when a user makes their request, rather than the training of models, an area where Nvidia’s processors are dominant.

AMD/INTC: Hearing Clev positive raising numbers saying CY26 CPU now +20% y/y as both continue to raise price. Also saying ARM feedback stepping up due to x86 shortage & strong Verea feedback

AMD: TD Cowen Raises PT to $600, Sees CPUs Emerging as Major AI Growth Driver

TD Cowen raised its PT on AMD to $600 from $500 following meetings with CEO Lisa Su and IR, citing growing conviction that agentic AI is creating a meaningful incremental CPU opportunity. The firm notes AMD’s recently increased $120B CPU TAM could still prove conservative as enterprises deploy AI workloads requiring high-performance, low-latency CPUs, benefiting the EPYC franchise alongside Instinct accelerators. Management also reiterated that MI450 and Helios remain on track for a 3Q26 launch, with volumes ramping through 4Q26 and 2027. While Cowen trimmed near-term accelerator estimates, it raised CPU assumptions meaningfully, resulting in higher FY27 revenue and EPS forecasts.

MEMORY:

Samsung/SK Hynix/Kioxia: Goldman Sees Memory Upcycle Extending Through 2028, Raises Targets and Upgrades Kioxia

Goldman argues the current DRAM, NAND, and HBM cycle is structurally different from prior memory upcycles, with tighter supply-demand conditions expected in 2027 than 2026 and shortages potentially extending into 2028. The firm cites three key drivers: stronger AI and server-driven demand, slower supply growth as HBM consumes more wafer capacity, and increasingly binding LTAs that improve earnings visibility and reduce cyclicality. Goldman raised its DRAM, NAND, and HBM pricing forecasts, including a bullish view that HBM ASPs could rise ~50% in 2027, and believes memory stocks deserve higher valuation multiples as elevated earnings prove more durable. The firm raised targets on Samsung and SK Hynix, reiterated Buy ratings, and upgraded Kioxia to Bu

Memory: Irrational Analysis shifts from being bearish on DRAM to seeing meaningful upside

His core engineering thesis is that HBM (high-bandwidth memory) is fundamentally a mistake destined to lose ~90% of its peak volume within 7-10 years, because its bandwidth gains come from a poor PHY design and TSVs (vertical wiring) that consume valuable chip “shoreline” while driving untenable cost, power, and thermal problems—the messy HBM4 rollout being exhibit A. He argues the real future is disaggregated, optically-connected pools of commodity LPDDR memory (hinted at by Nvidia at ISSCC 2026), with intermediate fixes being hybrid-bonded HBM and CXL. Crucially, he believes a shift away from HBM back toward standard DRAM would actually benefit DRAM makers, not hurt them: HBM consumes roughly 3GB of regular DRAM capacity per 1GB produced, so reversing that would triple effective supply, let margins ease from ~80% to a more sustainable ~60%, and still leave vendors with higher total profits (3x revenue) while satisfying agentic AI demand and keeping customers happy. On the investment side, he thinks DRAM stocks may have another double or triple left—driven by genuine, structural agentic-AI demand rather than a demand pull-forward, putting the cycle top likely 18+ months out.

His top pick is Samsung, because it uniquely combines an in-house logic foundry, interface/IP and high-speed signal-integrity expertise, and a silicon-photonics/co-packaged-optics group, positioning it to co-design memory, packaging, and optical interfaces in ways SK Hynix and Micron can’t

Memory:

Kioxia: Goldman Upgrades to Buy, Sees NAND Tightness Supporting Peak Profits Through FY28

Reminder Analyst day is tonight

Goldman upgraded Kioxia to Buy and raised its PT to ¥93,000 from ¥48,000, lifting FY27-29 operating profit estimates to 16-48% above consensus. The firm argues NAND supply-demand conditions should remain tight through FY28 as Samsung and SK Hynix prioritize DRAM/HBM investment, constraining NAND capacity growth and supporting higher ASPs. Goldman now expects CY26 NAND ASPs to rise 4.3x y/y and sees Kioxia sustaining ~80% operating margins through FY29, well above historical cycle peaks. The analyst believes the market is underestimating the duration of peak profitability rather than NAND cyclicality itself

SNDK: TD Cowen Highlights Attractive LTA Structure, Says Gross Margin Floor Exceeds DRAM Checks

TD Cowen came away constructive on SNDK after management highlighted that roughly 30% of next year’s capacity is already locked under long-term agreements, with a goal of increasing that percentage over time. The firm noted the gross margin floor embedded in those contracts appears meaningfully higher than what its channel checks suggest for DRAM suppliers, estimating an ~80% floor for SNDK versus ~60% in DRAM. Cowen argues that with this type of margin protection, durability of pricing and contract structure matters more than continued NAND price increases. The key watch item is whether other hyperscalers adopt similar long-term procurement agreements.

STX/WDC/INTC: Wells Fargo Bus Tour Reinforces AI Demand, Supply Tightness Through 2027

Wells Fargo’s Silicon Valley bus tour found demand remains strong across AI infrastructure, with supply now the primary constraint and tightness expected through at least 2027. The firm highlighted NVDA revenue density approaching $40B per gigawatt, suggesting Street datacenter assumptions remain too conservative, while calling INTC one of the most actionable ideas given improving server CPU momentum, growing ASIC wins, and rising foundry confidence. Wells Fargo also remains constructive on STX and WDC, citing a durable >20% growth outlook and visibility extending beyond 2029. The firm argues the debate is no longer whether the cycle exists, but how long it lasts.

NVDA: Jefferies Says Jensen’s Korea Visit Highlights Growing Focus on Physical AI and HBM Supply

Jefferies views Jensen Huang’s Korea visit as a sign of Nvidia’s deepening reliance on Korea for both physical AI development and memory supply. The firm expects discussions to focus on expanding the physical AI ecosystem through partnerships with companies such as Hyundai and LG, while strengthening supply-chain relationships with Samsung and SK Hynix. Jefferies also expects Nvidia to source more than 80% of its HBM4 demand from Samsung and SK Hynix, reinforcing Korea’s critical role in next-generation AI infrastructure. The analyst sees robotics, humanoids, autonomous systems, and industrial AI as key areas of collaboration.

AMZN: Evercore Says Amazon Supply Chain Services (ASCS) Could Be a $25B+ Revenue Opportunity

Evercore reiterated Outperform and a $315 PT following a deep dive on Amazon Supply Chain Services (ASCS), arguing the business could generate roughly $25bn of revenue and $2.5bn of EBIT over time by monetizing excess capacity across Amazon’s freight, logistics, and fulfillment network. The firm highlights early customer traction, including non-retail shippers, and estimates the opportunity could reach $40-60bn in a bull case if Amazon closes key operational gaps and gains broader share in third-party logistics. Evercore notes Amazon’s unique advantage is leveraging existing infrastructure and fixed costs, making incremental external volume highly margin accretive. The primary constraints remain limited LTL coverage, incomplete B2B pickup density, and internal capacity priorities as Amazon continues insourcing volume from third-party carriers.

AMZN: BofA Says Project Kuiper Nearing Commercial Inflection, Sees Attractive Long-Term ROI

BofA says Amazon’s Project Kuiper is approaching a key inflection, with satellite launches accelerating in 2Q and commercial service expected to begin in 3Q. The firm estimates Amazon will invest roughly $25B through 2028, but sees a sizable revenue opportunity, including ~$14B of consumer broadband revenue and $6-11B of enterprise/government revenue by 2032. BofA also highlights strategic benefits through AWS and logistics synergies, arguing Kuiper could generate attractive long-term returns despite near-term investment pressure. The firm reiterates Buy, viewing the project as an increasingly important and underappreciated asset within Amazon

ADYEN: BNP Paribas Downgrades to Neutral on Slowing Share Gains

BNP Paribas downgraded Adyen to Neutral and cut its PT to €890, arguing market-share gains are slowing and growth in Europe is likely to decelerate through 2027-28. The firm estimates Adyen now holds roughly 30% share of its European TAM and sees fewer opportunities for outsized gains as the market matures. BNP lowered 2027-28 revenue estimates by 3-4% and EBITDA estimates by 2-8%, leaving forecasts below both company guidance and consensus. While the stock has already corrected materially, the firm sees limited near-term catalysts for a re-rating as growth continues to normalize.

ZS: Guggenheim Upgrades to Buy, Sees De-Risked Growth and Improving Execution

Guggenheim upgraded ZS to Buy and introduced a $214 PT, arguing the post-earnings selloff has created an attractive entry point as revenue and ARR risks appear largely reset. The firm believes management has stabilized GTM execution under new leadership, with improving sales productivity and signs channel contribution is recovering. Guggenheim also sees the firewall market entering a hyper-growth phase driven by hardware displacement, positioning Zscaler as a key beneficiary. In addition, the firm views the Red Canary acquisition as strategically and financially accretive, adding meaningful ARR while strengthening Zscaler’s security platform.

IBM: Barclays Initiates Overweight, Sees Durable Software-Led Growth and Quantum Upside

Barclays initiated IBM with an Overweight rating and $350 PT, arguing the company’s transition to a software-centric model has created a more durable growth and margin profile. The firm notes software now accounts for nearly half of revenue and the majority of profits, with the mix expected to increase further as hybrid cloud and enterprise software adoption expands. Barclays also views IBM’s quantum computing efforts as a meaningful long-term option, positioning the company as an early leader in a potentially transformative market. The analyst believes IBM’s recurring revenue base, margin expansion potential, and quantum optionality are not fully reflected in the current valuation.

DELL: Morgan Stanley Upgrades to Equal-Weight, Cites Memory Advantage and Share Gains

Morgan Stanley upgraded DELL to Equal-Weight from Underweight and raised its PT to $448 from $170 after concluding the company is benefiting from preferential memory supply and pricing, driving share gains across PCs and general-purpose servers. The firm now models FY27 EPS of $19.67 and FY28 EPS of $22.40, both above Street expectations, and believes server demand can remain strong through FY28. Morgan Stanley’s supply-chain work suggests memory remains the key differentiator, while management continues to see demand outpacing supply, implying estimates may still be too low. The firm stops short of Overweight given the stock’s sharp YTD move and uncertainty around the durability of enterprise spending pull-forward.

AVGO: JPM Checks Suggest Google TPU v9 Program Shifting to MediaTek, Key Debate Moves to 2028

JPM’s supply-chain checks indicate Google may be shifting its TPU v9 program to MediaTek, with Broadcom’s TPU v9 design potentially canceled or deferred in favor of extending the current v8 platform. The firm now models 2028 TPU v9 revenue at ~$25.2bn and total DC ASIC revenue at $29.6bn, up from $10.8bn in 2027, while estimating MediaTek’s solution could be 40-50% lower cost than Broadcom’s. JPM notes packaging yields and the outcome of Google’s v10 TPU RFQ remain key swing factors, with MediaTek, Broadcom, Alchip, and Marvell all participating. Near-term estimates are largely unchanged, with the stock impact tied primarily to how investors assess Broadcom’s ASIC positioning into 2028.

AVGO: JPM Raises FY27 AI Backlog View to $150B+, Reiterates Overweight/PT $500

JPM raised its FY27 AI backlog estimate for Broadcom to more than $150B from over $120B, citing stronger AI inferencing demand and increasing visibility across Google TPU, Meta MTIA, and OpenAI custom silicon programs. The firm notes Broadcom’s next-generation Tomahawk 6 switching platform is nearly sold out for next year, while incremental upside is emerging from TPU v8i, Meta ASIC ramps, and OpenAI’s XPU efforts. JPM also expects improving AI shipment trends through 2H26 and sees potential upside to FY27 revenue estimates, with AI revenue now tracking toward roughly $60B. The analyst remains constructive on Broadcom’s positioning across AI ASICs and networking, viewing the company as a key beneficiary of ongoing AI infrastructure spending.

ACN: Truist Downgrades to Hold, Sees Core Revenue Growth Under Pressure Despite AI Momentum

Truist downgraded ACN to Hold and cut its PT to $210, citing pressured enterprise budgets, increased competition, and ongoing shifts toward outcome-based pricing models. The firm reduced FY26 estimates after channel checks pointed to slower discretionary spending, particularly in Energy and Travel, and now expects growth to remain below historical levels. While AI-related revenue continues to grow rapidly and should become a more meaningful contributor over time, Truist believes it is not yet large enough to offset weakness in the broader business. The firm also notes recent softness across peers suggests demand conditions are becoming more challenging across IT services.

Robotics: OpenAI enters the arena

AI Tokens: Companies Begin to Ration AI as Cost Soars

WSJ:

Use of artificial intelligence by big companies is exploding—and the soaring cost has some of them pumping the brakes in a way that could complicate AI’s triumphal march across the economy.

All that enthusiasm has resulted in skyrocketing costs for so-called tokens, the basic unit of measurement for AI computing, as AI model providers seek to balance supply and demand and manage their own costs. Some enterprises have hit their annual budget in just three months or reported seeing their AI spending bills double or triple.

Now corporate leaders are scrambling to bring down expenses by finding ways to ration AI use in their organizations, steer workers toward cheaper, homegrown tools and help them hone their skills to improve returns.

For companies using advanced AI coding tools, only 18% of spending on tokens is translating into shipped coding products that reach real users, according to EntelligenceAI, a startup that aggregated data on more than 2,000 companies using advanced AI tools for coding.

META: RBC Sees AI-Driven SMB Creation as an Underappreciated Long-Term Growth Driver

RBC argues the market is underestimating META’s opportunity to create and monetize new small businesses through AI tools, framing it as a potential sixth growth pillar not reflected in current valuation. The firm notes META already reaches roughly 250M businesses across its platforms, with only a small percentage spending more than $20k annually on advertising, creating a large monetization runway. RBC estimates ~10M new SMBs are formed globally each year, representing a sizeable pool of future advertising demand, while early AI products such as Andromeda are already showing measurable improvements in ad performance. The analyst believes META’s AI stack could lower the barriers to business creation and eventually drive incremental advertiser growth, though adoption and monetization remain in the early stages.

META: Meta Memo Outlines Ambitious Hardware Plans, Including New AI Pendant

Meta Platforms plans to start testing an AI pendant in the next year as part of an ambitious roadmap for wearable devices aimed at reversing the huge losses in its hardware division.

An internal memo describing the roadmap, reviewed by The Information, also lays out plans to significantly expand its selection of AI glasses and to add a business-focused service called “Wearables for Work.” The memo, from Alex Himel, Meta’s vice president of wearables, says the strategy is in part to drive more use of Meta’s AI models and products such as subscription versions of its apps and a consumer AI agent it is developing called Hatch.

GOOGL/RDDT/META: Piper Sees AI Search Expanding Rapidly, Raises GOOGL PT to $445

Piper’s analysis of Google AI Overview and AI Mode citations suggests AI-assisted search is scaling quickly, with daily citations up ~16x since early 2025 and increasingly concentrated among a handful of content providers. The firm views Google as the primary beneficiary, raising its PT to $445 and increasing Search revenue estimates, citing strong citation share, accelerating AI Mode adoption, and management commentary that AI Mode queries are running at record levels. Piper also highlights RDDT and META as notable winners, with Reddit ranking #3 in citation share and Meta ranking #2, reinforcing their growing importance as source material for AI search results.

ORCL: Deutsche Bank Deep Dive Says AI OCI Economics Are Better Than Bears Appreciate, Reiterates Buy/PT $300

Deutsche Bank argues Oracle’s AI infrastructure business is already value-creative and that investor concerns around cloud profitability are overstating the impact of near-term margin pressure. The firm estimates OCI gross margins are currently in the mid-30s and should trough in the low-30s before recovering toward ~40% by FY30 as scaling costs normalize and operating leverage emerges. DB’s work suggests AI infrastructure contracts can generate high-teens IRRs under a traditional cloud model, while OCI AI gross margins appear consistent with management’s 30-40% target range. The analyst believes the market is underappreciating both the temporary nature of pre-revenue scaling costs and the contribution from higher-margin Cloud Database and SaaS businesses, which should help offset AI mix headwinds over time.

MSFT: Wells Fargo Raises PT to $650, Sees AI Driving Higher Azure and Copilot Estimates

Wells Fargo raised its PT on MSFT to $650 from $625 following a deep dive on AI, arguing investor focus is shifting from infrastructure spending to monetization across Azure, Copilot, and software models. The firm raised Azure estimates through FY30, citing accelerating capacity expansion and stronger AI demand, while also increasing Microsoft 365 Copilot forecasts and now modeling roughly $4B/$10B/$20B of annual revenue in FY26/FY27/FY28. Wells Fargo estimates OpenAI remains the primary contributor to Azure AI revenue today, but expects Microsoft’s own software and model layers to become a more meaningful driver over time. The firm remains constructive on Microsoft’s AI positioning, citing improving monetization visibility ahead of Build.

PANW: JPM Raises PT to $300 Ahead of Print, Sees AI Security Demand and CYBR Upside

JPM raised its PT on PANW to $300 from $200 ahead of earnings, citing peer multiple expansion and PANW’s positioning as a key AI security beneficiary. The firm’s channel checks point to healthy demand, with AI-related security spending increasingly supplementing traditional IT budgets and accelerating pipeline activity. JPM also highlights Project Glasswing as a differentiated near-term catalyst and views CYBR guidance as conservative, leaving room for upside as integration progresses. The analyst expects continued strength in SASE and software mix, supporting margins and reinforcing the AI security narrative.

AMAT/LRCX: TD Cowen Sees WFE Tracking Toward $180-200B in 2027, Potentially $220B+ by 2028

TD Cowen said management teams remain constructive on the multi-year WFE outlook, with little pushback to investor expectations for $180-200B WFE in 2027 and potentially $220B+ by 2028. The firm highlighted pricing power across front-end equipment, strong AI-driven demand, and incremental AGI-related CPU demand as a potential driver of another leg of spending growth. LRCX was flagged as a key beneficiary given NAND upside, foundry/DRAM exposure, and readiness for a larger WFE ramp.

ANET: Evercore ISI Deep Dive Highlights EOS as Key AI Networking Moat

Evcore ISI argues Arista’s Extensible Operating System (EOS) is an underappreciated competitive advantage and a key reason the company is positioned to benefit from AI networking growth. The firm highlights EOS’s reliability, automation, observability, congestion management, and programmability, arguing these capabilities become increasingly valuable as AI clusters scale and network complexity rises. EOS is viewed as a full-stack differentiator that enables Arista to expand beyond traditional networking into AI fabrics, scale-up architectures, and eventually enterprise AI deployments.

AAPL: Morgan Stanley Sees WWDC as Opportunity to Recast Apple as an AI Winner

Morgan Stanley views WWDC as a pivotal catalyst that could shift investor perception of Apple from an AI laggard to an AI winner, with successful agentic Siri and Apple Intelligence updates potentially supporting a $365-385 valuation range. The firm expects Apple to unveil a more conversational Siri, deeper system-wide AI integration, and broader third-party model support, positioning Apple as an AI distributor rather than a single-model provider. Morgan Stanley believes faster iPhone upgrades and incremental Services monetization are the primary financial levers, while privacy, model flexibility, and ecosystem integration remain key differentiators. The main debate is execution, but low expectations create a favorable setup if Apple delivers a credible agentic AI roadmap.