TMTB Morning Wrap

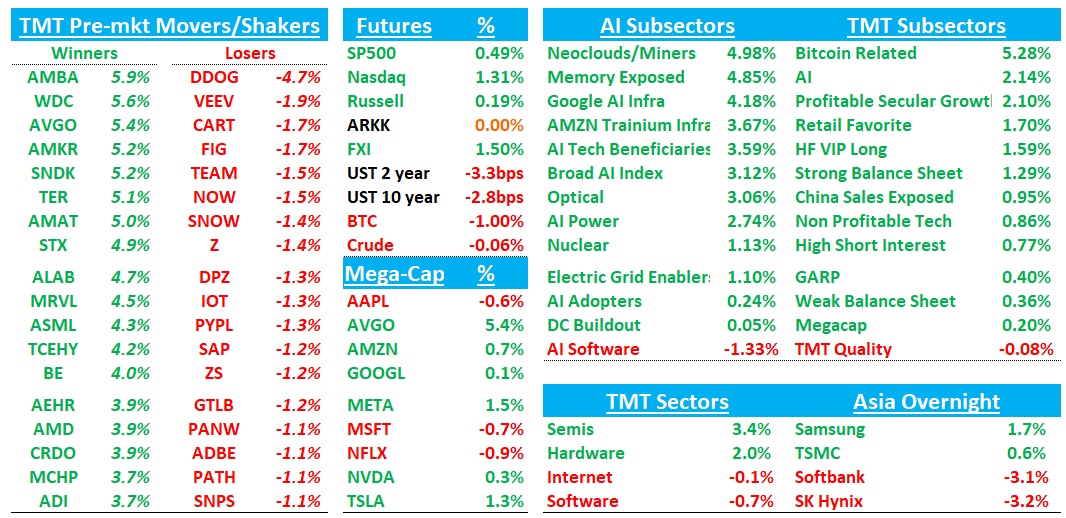

Good morning. Good to be fully back after some time off. Futures higher this morning with Nas +130pbps, S&P +50bps, Russell+25bps as we look to be rolling back some of the massive unwind from last week after Momentum baskets down close to 20% in 2 days. Yields down 2-4bps across the curve.

In Tech, Semis +3.5% while Software -70bps. AVGO leading the way higher after renewing with AAPL through 2031, the usual suspects on a semi up day (HDDs/Memory/semicap) outperforming early, and AMD catching a bid on the NVDA Kyber delay news getting passed around.

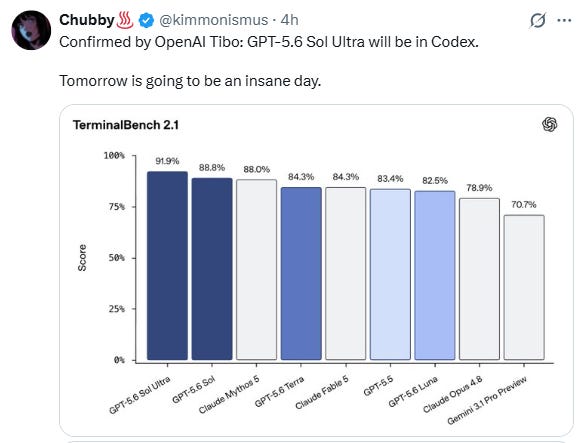

We get Samsung earnings this week and a likely GPT 5.6 release. Should be a fun one. Let’s get to it…

AVGO/AAPL: Broadcom, Apple extend chip partnership through 2031 - Reuters

Broadcom said on Monday that the chipmaker and Apple have agreed to expand their partnership through 2031 to develop and supply a range of custom chips. Broadcom has been a long-standing supplier to Apple, providing key components, including custom radio frequency chips used in iPhones, Wi-Fi and Bluetooth connectivity chips, and other networking semiconductors.

Reminder, AAPL is AVGO’s largest customer (about low teens %). Some context from Claude:

Locking the relationship through 2031 does three things: it converts a business the Street was modeling as a melting ice cube into ~5+ years of contracted, high-margin revenue visibility; it kills the “RF is next after WiFi” narrative; and the “range of custom chips” language suggests the relationship is broadening rather than shrinking — likely formalizing the AI silicon work, since Apple has been working with Broadcom on its first AI server chip (codenamed Baltra, targeting mass production in 2026 on TSMC N3P).

DDOG: Bernstein Raises Long-Term Estimates but Downgrades on Near-Term Expectations

Bernstein raised its long-term estimates for Datadog, citing increasing confidence in the company’s AI platform opportunity, but downgraded the stock to Market Perform on valuation and elevated near-term expectations. The firm expects a strong 2Q, but believes growth could disappoint beginning in Q3/Q4 as ex-AI demand (~85% of revenue) flattens and AI lab growth starts to normalize. Bernstein expects Q4 revenue growth to slow roughly 500bps to ~29% y/y, well below investor expectations for 30%+ growth into next year and peak growth in the high-30% to 40%+ range.

Semis: Citi Expects Another Quarter of Earnings Upside as AI Demand Remains Strong

Citi expects another strong semiconductor earnings season, arguing AI infrastructure demand remains supply-constrained despite recent concerns around excess compute capacity. The firm continues to favor AMD, TXN, and AMAT, sees DRAM shortages as the biggest bottleneck for AI compute, and expects memory, semicap, compute, and analog to outperform. Citi also sees ASICs gaining share, forecasting custom ASIC revenue to grow at a 119% CAGR through 2030 as hyperscalers increasingly diversify AI architectures.

Semis: Goldman Sees Broad 2Q Earnings Upside but Prefers Selectivity After the Rally

Goldman expects broad upside across the semiconductor sector this earnings season, driven by continued strength in compute, semicap, storage, and analog, though it believes the strong year-to-date rally raises the bar for stocks. The firm’s preferred tactical ideas are AMAT, AMD, and ON, citing upside from server CPU demand, AI infrastructure spending, and analog pricing, while remaining cautious on KLAC, ARM, and Qorvo due to tougher near-term setups. Goldman also expects continued memory strength as tight HBM and NAND supply supports pricing through 2028.

SK Hynix: US ADR launching with $28B proceeds target, plans to price on Thursday.

AMD: Goldman sees server CPU upside and MI450 ramp as key catalysts; raises PT to $640

Goldman reiterates Buy on AMD and raises its PT to $640 from $450, with 2027 EPS moving to $14.50, ~13% above Street. The firm expects a strong quarter and guide, driven by server CPU demand tied to agentic AI/infrastructure spending, with commentary on MI450 timing, Meta/OpenAI deployments and new customer engagements potentially pushing 2027 datacenter GPU estimates higher. Goldman says the July 23 Advancing AI event should be a positive catalyst, while key risks are slower agentic AI adoption, weaker AMD GPU deployment at Meta, x86 share erosion and limited operating leverage.

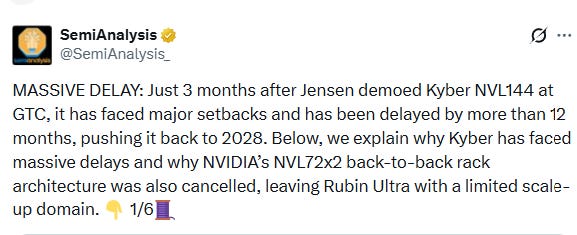

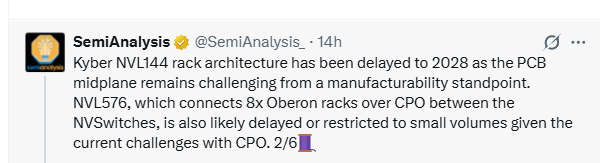

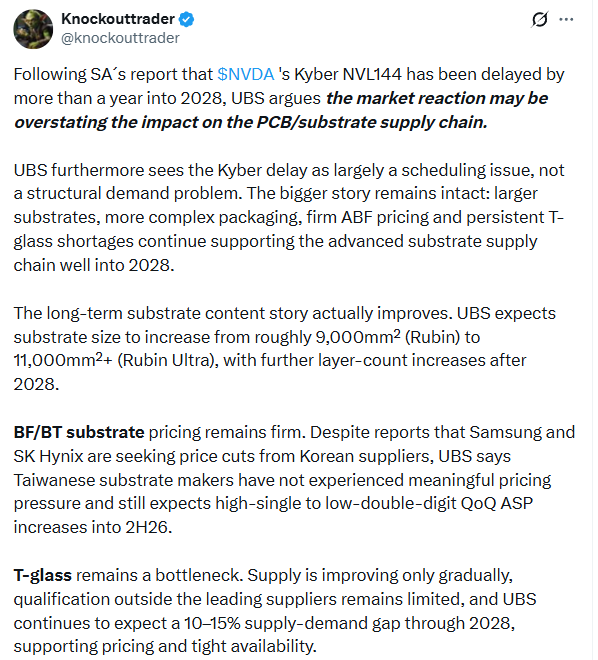

NVDA: Semianalysis says Kyber NVL144 delayed by more than 12 months

Kyber delay should ultimately be good for AMD’s MI competitive positioning, NPO, and Copper

PCB/CCL: Jefferies cuts AI PCB/CCL TAM on potential Kyber delay, but sees upstream material suppliers outperforming

Jefferies says potential delays to Nvidia Kyber/backplane PCB adoption for Rubin Ultra could create ~5–8% downside to its 2027 AI PCB/CCL TAM and another ~11–16% downside in 2028 if Kyber is ultimately cancelled. The firm now expects Kyber may slip out of Rubin Ultra in 2027 and possibly into a new Rubin Ultra variant in 2028, with Oberon structure likely used as the fallback. Jefferies sees this as negative for PCB supply-chain sentiment, but more positive for copper cable and upstream material vendors, where demand remains tight and suppliers should have better pricing power than downstream PCB makers.

OpenAI: GPT- 5.6 is likely to drop tomorrow

QCOM: Citi Adds 30-Day Downside Catalyst Watch on Smartphone Weakness

Citi added a 30-Day Downside Catalyst Watch on Qualcomm, citing worsening Android handset demand following smartphone shipment cuts from Xiaomi, Oppo, and Vivo. The firm models QCT handset revenue down 14% y/y in FY26 and expects June-quarter sales and EPS to come in modestly below Street expectations.

TSMC: Citi Adds 30-Day Upside Catalyst Watch Ahead of Earnings

Citi added a 30-Day Upside Catalyst Watch on TSMC ahead of its July 16 earnings report as Citi believes TSMC has a high probability of raising its 2026 revenue growth target and long-term CAGR outlook at its July 16 analyst meeting, supported by sustained leading-edge demand. The firm argues TSMC’s key advantage is its manufacturing scale, expecting combined N2/A16/N3 capacity to reach ~350-400k wafers/month by end-2028, supporting pricing power and margins. Citi also sees advanced packaging as an increasingly important growth driver beyond CoWoS and reiterated its Buy rating with a NT$3,800 PT.

MU: Citi Adds 90-Day Upside Catalyst Watch on DRAM Pricing

Citi added an Upside 90-Day Catalyst Watch on Micron, expecting stronger AI-driven DRAM pricing to drive upside into earnings. The firm raised its 2Q/3Q/4Q26 DRAM ASP forecasts to +44%/+20%/+13% QoQ (from +37%/+13%/+11%) and believes upside remains for the roughly 60% of Micron’s sales that are not yet covered by long-term agreements.

AAOI: B. Riley flags structural TAM risk from Amazon RNG/OpenAI MRC architectures

B. Riley says Amazon’s RNG and OpenAI’s MRC could become structural headwinds for optical transceiver TAM as hyperscalers shift to flatter, more passive network architectures. The firm estimates RNG could replace active aggregation switches with passive optical ShuffleBoxes, reducing active networking equipment by >60% and transceiver counts by ~40–50%. AAOI is most exposed given Amazon and Oracle are expected to be key anchor customers for the 800G/1.6T transceivers driving its growth outlook.