TMTB Morning Wrap

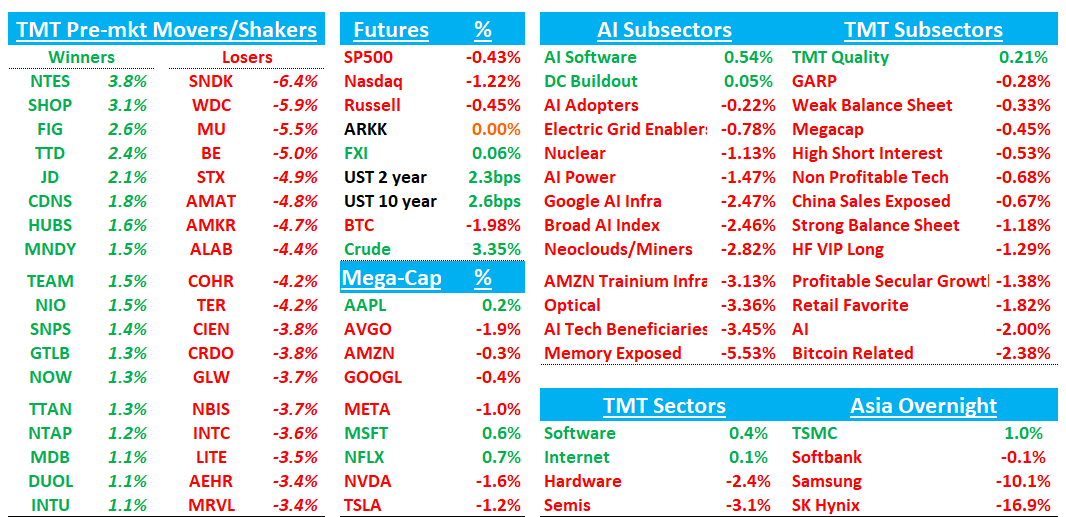

Good morning. QQQs -1.2% as tensions escalated in Iran over the weekend and has Oil +4%. Yields are ticking up 2-3bps across the curve. BTC -2%.

Korea fell 9% and is dragging down semis -3% with it early while Software +50bps and Internet +10bps are green. Memory names the weakest as Asian names were all down double digits: SNDK/WDC/MU/STX -5%.

Asia mainly red with Korea the big loser: TPX -0.72%, NKY -1.92%, Hang Seng +0.16%, HSCEI +0.33%, SHCOMP -2.06%, Shenzhen -4.01%, Taiwan TAIEX +0.06%, Korea KOSPI -8.95%. Memory names much weaker: SK Hynix -16%. Samsung -10%, Kioxia -13%.

Earnings start this week with TSM, ASML, and NFLX

Lots to get to, so let’s get to it…

SHOP: Jefferies Upgrades to Buy as Agentic Commerce, Pricing and Partner Economics Add Upside

Jefferies upgraded SHOP to Buy from Hold and raised its price target to $160 from $140, arguing the company is emerging as the infrastructure layer for agentic commerce while near-term fundamentals remain stronger than Street expectations. Third-party data points to roughly 32% y/y GMV growth in 2Q versus Street near 27%, while a potential non-Plus price increase could add about 3%–4% to 2027 revenue and provide meaningful profit upside. Jefferies also views the new partner-incentive model as a long-term positive because it should improve merchant acquisition and lower lifetime sales costs, despite higher near-term payouts. Jefferies also estimates agentic commerce could shift $9B–$72B of GMV toward independent merchants by 2028, with SHOP positioned to capture incremental GMV, merchant additions, retention and take-rate expansion.

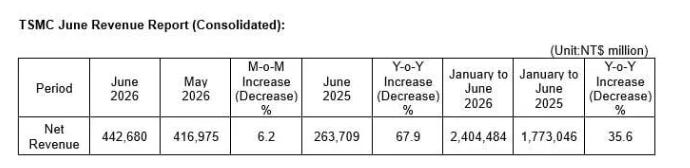

TSM: Reports solid June #s ahead of earnings on Thursday

June +6% above typical seasonality of -5%. Means June q should come in at $40.1B assuming NT31.7, at the top of the range and slightly above street. Earnings on Thursday.

TSM: BofA Raises Estimates and PT as AI Demand, Pricing and Capex Visibility Strengthen

BofA raises its price target to NT$3,100 and lifts 2026–28 EPS estimates to NT$107/NT$153/NT$178 from NT$103/NT$150/NT$177, citing firmer AI demand, better pricing and improved capacity visibility. The firm expects 2Q sales up 12% q/q and 3Q growth of 10%–15%, with gross margin holding near 67%–68% despite 2nm dilution and higher summer electricity costs. The bigger upside is capex, with BofA forecasting $58B in 2026 versus $56B guidance and $78B–$83B in 2027–28, while valuation remains reasonable at roughly 16x 2027 EPS.

SNDK: Evercore Raises PT to $3,100 as New Business Model Deals Reshape Earnings Visibility

Evercore reiterated Outperform and raised its price target to $3,100 from $1,400, arguing SNDK’s new business model agreements create a structural shift from commodity-driven earnings toward greater pricing and profit visibility. The firm estimates roughly $42B of RPO across three signed deals, with additional contracts potentially lifting secured commitments toward $62B; these agreements could underpin more than 20% of FY27 EPS, with the remainder benefiting from tighter NAND supply and higher merchant pricing. Evercore now forecasts FY27 revenue of $47.8B and EPS of $212.78, sees bull-case upside to $4,000, and believes valuation can rerate as investors gain confidence in a more durable earnings profile.