TMTB Morning Wrap

Good morning. Futures +90bps early as AI vibes in full force: GOOGL Cloud Next starts today, OpenAI’s new image model getting some great reviews, Cursor getting bought for $60B, and TEL/ASMI/GEV/VRT all with some solid reports. On the macro front, Trump extended the ceasefire pending ongoing talks, while Axios reports he’s giving Iran ~3–5 days to present a unified counterproposal. Iran says it won’t reopen the Strait of Hormuz or resume negotiations until the U.S. lifts its naval blockade, and the IRGC seized two ships on Wednesday.

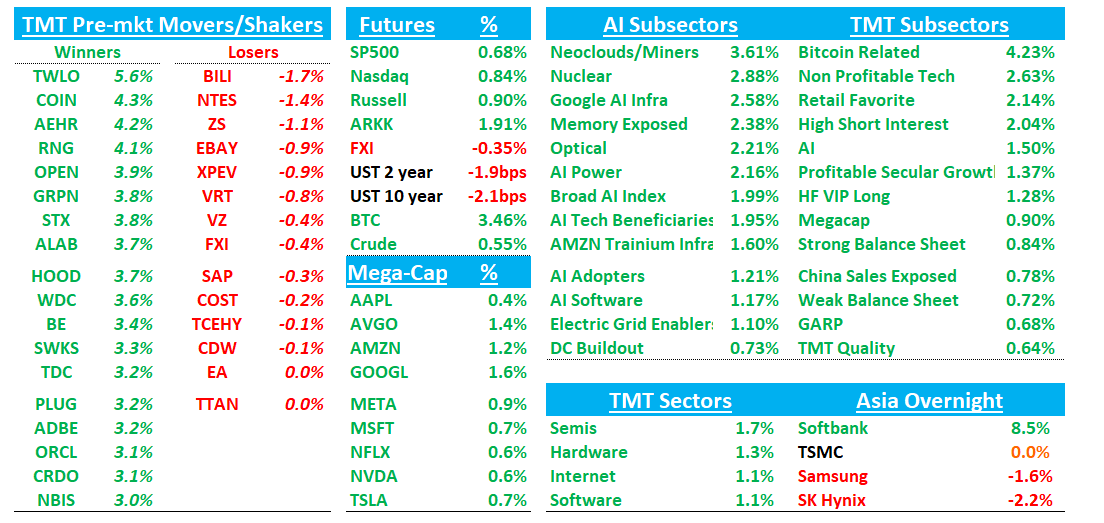

Asia mixed overnight: TPX -0.67%, NKY +0.4%, Hang Seng -1.22%, HSCEI -1.59%, SHCOMP +0.52%, Shenzhen +1%, Taiwan TAIEX +0.73%, Korea KOSPI +0.46%. Softbank +8% /ORCL +3.5% continue to rip on improving OAI vibes with their new image model and Spud/ChatGPT 5.5 likely coming out very shortly. BTC +4%

We get NOW, TXN, IBM, TSLA tonight.

Should be a fun one. Let’s get to it…

SpaceX obtains right to buy AI start-up Cursor for $60bn

Elon Musk’s SpaceX has struck a deal for the right to acquire code-editing start-up Cursor for $60bn in an attempt to catch up with AI rivals months before the rocket maker’s initial public offering. SpaceX said the companies were working together “to create the world’s best coding and knowledge work AI” and that it had an option to buy Anysphere, Cursor’s parent company, for $60bn this year. Cursor was valued at $29bn in November and has been one of the fastest-growing start-ups in Silicon Valley since it launched in 2022.

GOOGL: Google Cloud Releases New TPU Chip Lineup in Bid to Speed Up AI

Bloomberg:

The new lineup will come in two versions, the company said Wednesday at its Google Cloud Next event. The TPU 8t is tailored for creating artificial intelligence software, while the TPU 8i is designed to run AI services after they’ve been created — a stage known as inference.

This approach helps make AI responses more instantaneous because the component doesn’t have to go seek information stored elsewhere. It’s particularly useful when computers “reason” through problems, taking multiple steps and learning from their own actions.

The training chip, 8t, can be combined into groups of 9,600 semiconductors. Google said that when deploying such massive systems, power is increasingly the major constraint in data centers. Owners therefore need systems that are more efficient to get the best out of the limited availability of electricity. TPU 8t delivers 124% more performance per watt than the preceding generation, with TPU 8i providing a gain of 117%.

More from GOOGL early at Cloud Next:

-75% of all new code at GOOGL is now AI generated

-Gemini Enterprise 1Q Paid MAU +40% q/q

ABNB: Wells Fargo Upgrades to Overweight, $178 PT; Innovation Cycle Driving Re-Acceleration

Wells Fargo upgrades ABNB to Overweight with a $178 PT, citing a business inflection as innovation (sponsored listings, merchandising, AI search, loyalty) drives faster growth and margin expansion after a period of deceleration. The firm expects accelerating room nights (~8–10% growth) and improving monetization (~100bps take rate uplift by 2029), with ads becoming a meaningful revenue stream (~$1.5B LT). Net, Wells sees ABNB re-accelerating growth into FY27–28 with upside to consensus across revenue and EPS.

TWLO: BofA Upgrades to Buy, Raises PT to $190; Voice AI Positioning Driving Re-Acceleration

BofA upgrades TWLO to Buy (from Underperform) and raises PT to $190, arguing Twilio is emerging as a key infrastructure layer for AI-driven voice and messaging and is unlikely to be disrupted by AI. The firm highlights accelerating gross profit growth, improving FCF margins (~21% by FY28), and stronger positioning as enterprises adopt voice AI use cases, with ~10%+ revenue growth expected into FY28. Net, BofA sees improving fundamentals and growth durability not fully reflected in the stock, supporting further upside.

STX: Barclays Upgrades to OW/$625, Raises WDC PT to $405 — Denser Platters Drive Earnings and Multiple Expansion

Barclays upgrades STX to OW (PT to $625) and raises WDC to $405, seeing the most value in the storage/memory hierarchy in the drive names on both earnings upside and multiple expansion. The duopoly structure, commitment to not add capacity, and significant pricing upside suggest another leg — $/TB gains should approach the high teens vs. company guidance of up single digits over the next two years as STX transitions to 40TB with HAMR, driving material density improvements and cost advantages from a structurally similar BOM. HDD industry revenue estimates raised ~$4B for CY26 to $29.7B (+31% Y/Y) and ~$9B for CY27 to $38.8B (+31%).