TMTB Morning Wrap

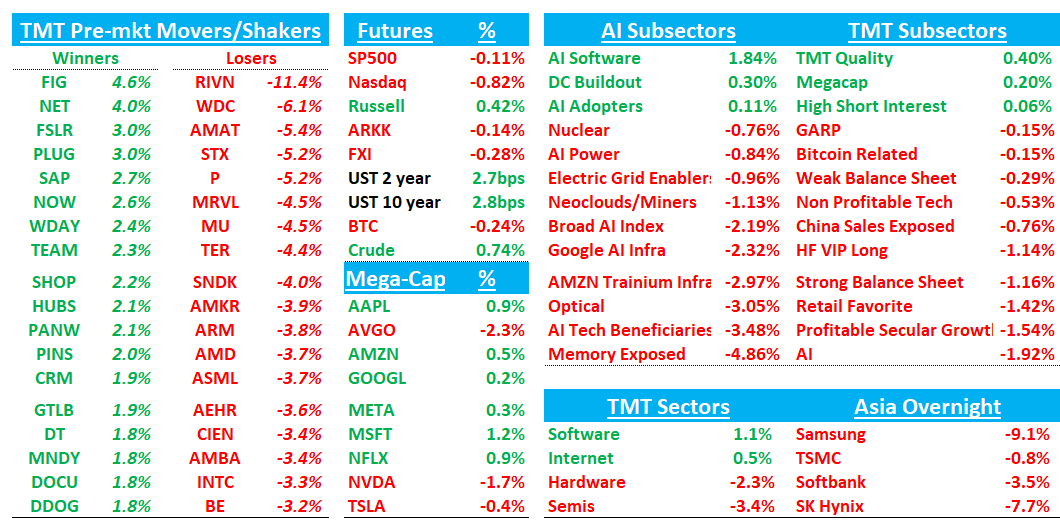

Good morning. QQQs -85bps / SPX -10bps / Russell +50bps as factor/mo vol continues. Yields higher this morning as market continues to price in 30bps worth of rate hikes in ’26. Semis -3.5% leading the way lower while Software +1.2% / Internet +50bps getting a bid. HDDs/Memory down 4-5%; CPU names ARM/INTC/AMD -4%; Semicap -4%.

Overnight, Asia was mainly red: TPX -0.97%, NKY -2.12%, Hang Seng -0.51%, HSCEI -0.54%, SHCOMP -1.26%, Shenzhen -1.92%, Taiwan TAIEX -2.31%, Korea KOSPI -4.91%. KOSPI hit circuit breakers as vol continues with memory names down significantly following Samsung’s lighter than expected #s: Samsung -9%; SK Hynix -8%; Kioxia -11%.

Let’s get straight to it…

Samsung: Samsung 2Q26 prelims comes in a shy of buyside expects

Revenue W171tn (+28% q-q / +129% y-y) vs street at W169tn and buyside looking for W174Tn+ and OP W89.4tn, 6% ahead of street. Revenue beat only 1% vs street vs 7% last q, and average of 3% over the past 4 quarters. Op profit beat of 6% was lowest in over 8 quarters.

DRAM/NAND drove the beat as expected: DRAM ASPs ~+45% q-q (bits +12%), NAND ASPs ~+57% q-q (bits +3%), on server DRAM and eSSD demand. Everything else was soft: foundry/LSI remained loss-making (deficit wider after bonuses), display profitability fell on pricing despite better-than-expected shipments, and MX swung to a loss as memory cost inflation hit with a lag — handset price hikes look likely in 2H (peers expected to raise 15–25%).

Commodity DRAM/NAND prices seen up another 15–20% q-q in 3Q before growth moderates as LTAs expand; HBM margins expected to converge up toward commodity DRAM. Supply stays tight through at least 2027.

Historical beats:

NET: Scotiabank Upgrades to Outperform, Says AI and Enterprise Momentum Create Attractive Entry Point

Scotiabank upgraded Cloudflare to Outperform from Sector Perform and raised its price target to $300 from $225, arguing the company’s AI and enterprise execution warrant owning the stock. The firm sees Cloudflare increasingly winning leading AI-native customers while recent CIO/CISO channel checks point to strengthening traction in SASE and edge compute, reinforcing confidence that enterprise adoption is accelerating. Scotiabank believes this combination of AI leadership and improving enterprise momentum supports a more constructive outlook for growth and shares.

APP: Wells Fargo Sees Softer 2Q Gaming Trends but Maintains Overweight

Wells Fargo expects AppLovin’s 2Q upside to be more modest than in recent quarters as mobile gaming checks point to weaker ROAS from CPI inflation, maturing optimization gains, and app user acquisition share plateauing around 45%. Web advertising trends remain stable but lack a meaningful acceleration. Despite lowering its FY26 web advertising revenue forecast by 10%, Wells Fargo modestly increased game revenue estimates, reiterated its Overweight rating, and raised its price target to $575 from $571, arguing the long-term thesis remains intact despite a tougher near-term setup.

FSLR: Deutsche Bank Upgrades to Buy, Sees Pullback Creating Attractive Entry Ahead of Section 232 Clarity

Deutsche Bank upgraded First Solar to Buy from Hold and raised its price target to $272 from $202, arguing the recent ~27% pullback has created an attractive entry point ahead of expected policy clarity. The firm believes investors are underappreciating the combination of a normalized 2027 earnings profile, a strong net cash balance sheet, and potential upside from Section 232 tariff clarifications, which could strengthen the competitive position of U.S. solar manufacturers. Trading at roughly 9x 2027 EV/EBITDA versus a historical 10–11x range, Deutsche Bank sees meaningful re-rating potential as execution improves, domestic capacity ramps, and policy uncertainty fades.