TMTB Morning Wrap

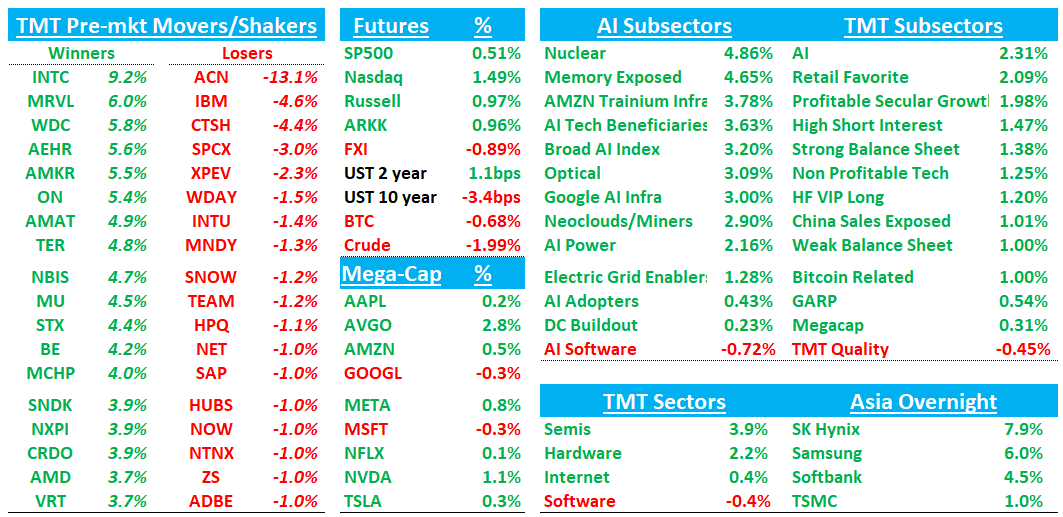

Good morning. Futures +1.5% more than clawing back yesterday’s post FOMC losses. Market is now pricing in ~36bps worth of hikes for YE up from 20bps prior to FOMC. The Iran MOU has now been signed by all parties and is in effect. Semis +4% strong early while software -50bps lags as ACN (-14%) #s look much worse fueling the AI disruption narrative. INTC +9%, HDDs and Memory leading the way higher.

Asia mixed overnight but Korea was strong: TPX +1.37%, NKY +1.65%, Hang Seng -1.59%, HSCEI -2.06%, SHCOMP -0.43%, Shenzhen +0.53%, Taiwan TAIEX +1.28%, Korea KOSPI +2.25%. Hynix +8% to more ATHs. Samsung +6%. Softbank +4.5%.

Last day of the week today as markets closed tomorrow. Let’s get to it…

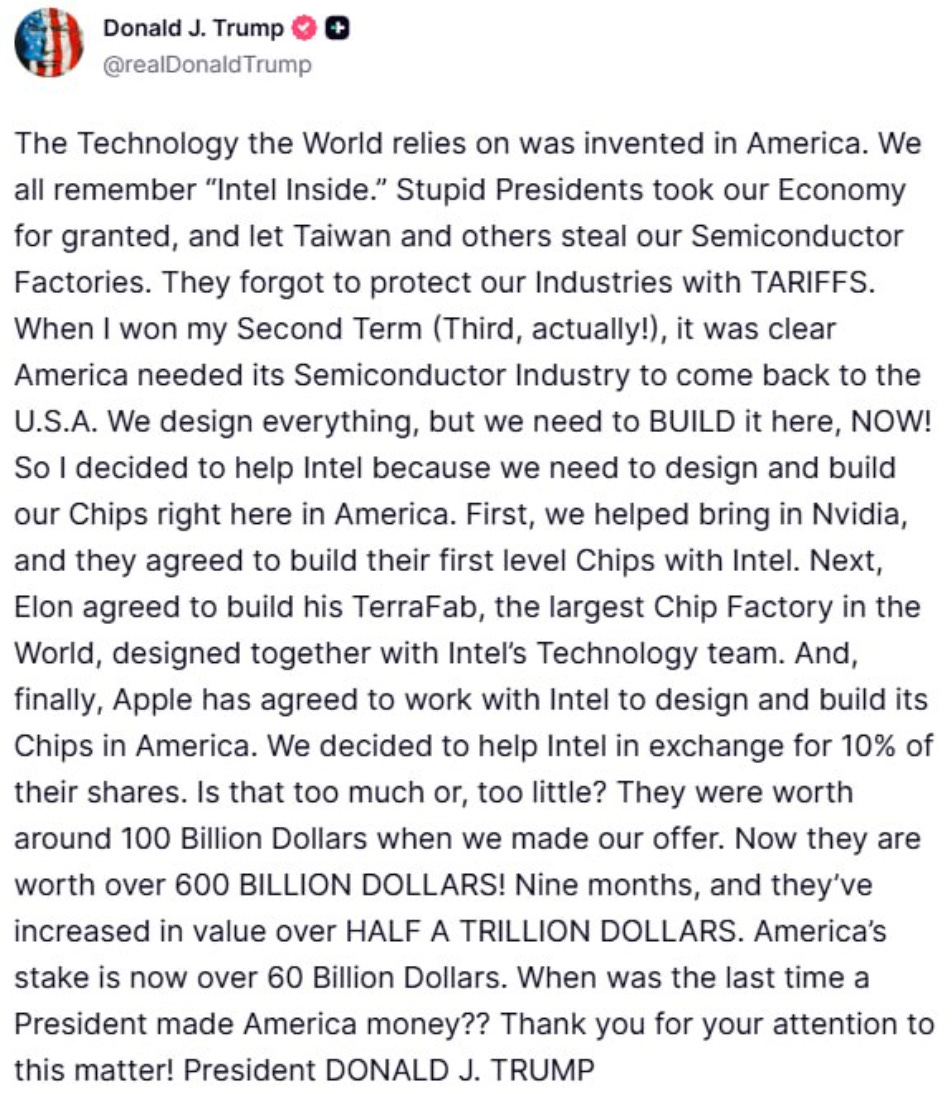

INTC +8%: Trump says INTC working to design AAPL chips

ACN -14%: Looks bad with revs, bookings and guidance all coming in weaker

Checks had been weak coming in, but this is even softer than expectations and will fuel the AI disruption narrative.

F3Q revenue of $18.72B missed street($18.80B) on soft Consulting, but adj EPS of $3.80 beat ($3.72) on stronger margins (17.0% vs. ~16.6% est.). Bookings -2% y/y vs +6% y/y las q with managed services -15% y/y. Guidance weaker: FY26 organic cc revenue cut to +3-4% (from +3-5%), and F4Q revenue of $17.75–18.40B guided below street(~$18.5B), pointing to softer discretionary demand.