TMTB Morning Wrap

Good morning. Futures -70bps rallying close to 1% after a CPI that was slightly cooler up 0.2% m/m vs expects of 0.3% m/m. Fed expects moving very slightly in a dovish direction while yields are flattish. In Tech, no big discrepancy among sectors with both software/internet/semis down about the same following the big Fable/Mythos release yesterday from Anthropic.

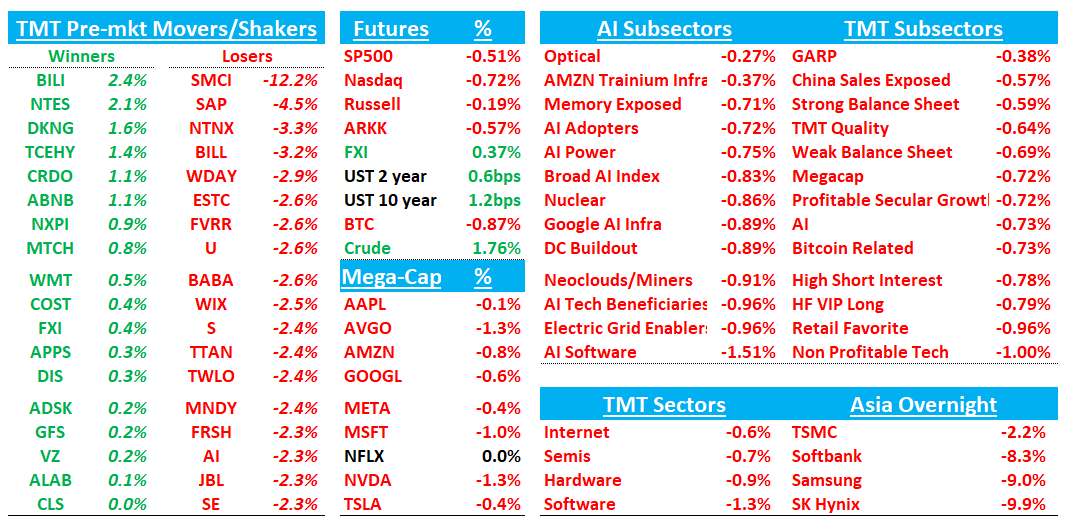

Asia generally weaker overnight although AI names were down: TPX -1.25%, NKY -1.89%, Hang Seng -0.64%, HSCEI -0.07%, SHCOMP -0.42%, Shenzhen -1.97%, Taiwan TAIEX -3.31%, Korea KOSPI -4.52%. Kioxia -8%; Softbank/Samsung/SK Hynix -8-10%

Lots to get to so let’s get straight to it…

OpenAI: OpenAI in Talks to Lease 10 Gigawatt Ohio Data Center with Backing From Nvidia

OpenAI is in advanced negotiations to lease a proposed 10 gigawatt data center campus on federal land in Ohio as part of a deal that could include financial backing from Nvidia, according to two people with direct knowledge of the discussions.

The campus under discussion would be among the biggest of its kind, with a total cost of at least $500 billion if fully built out based on today’s prices for chips, labor, power and other materials, the people said. OpenAI would control the equipment in the facility under a long-term lease and would be on the hook for payments once the project starts operations, with the first phase expected in 2028. The discussions haven’t been finalized and plans could change.

OpenAI: SoftBank Attempt to Get $6 Billion OpenAI Margin Loan Stalls

SoftBank Group Corp.’s talks with potential creditors to raise at least $6 billion from a margin loan backed by its OpenAI stake have stalled, people familiar with the matter said, just weeks after the Japanese conglomerate cut its initial target from $10 billion.

The company is considering various fundraising options, according to the people, who asked not to be identified discussing private matters. It could still move forward with the margin loan at a later stage, they added.

It’s unclear why the margin loan discussions stalled.

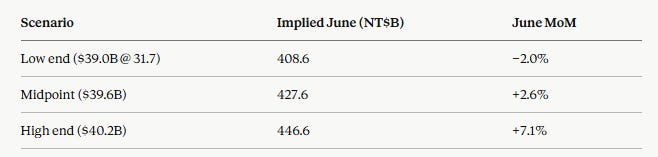

TSMC May 2026 revenue: NT$417.0B (+1.5% MoM, +30.1% YoY)

5 year median is 0.9%, so this is roughly in line with that.

QTD through two months: April NT$410.73B + May NT$416.98B = NT$827.7B, i.e. 66.9% of the low end and 65.9% of the midpoint. For reference, Apr+May has made up 67–72% of Q2 revenue in each of the last four years (67.1% in ‘22, 67.5% in ‘23, 69.1% in ‘24, 71.8% in ‘25).

For reference, June has been down MoM four straight years (−5.3%, −11.4%, −9.5%, −17.7% from ‘22 to ‘25; ~−11% average), which would imply they would need to outperform June to hit their guide.

However, given stronger TWD and assuming flattish June (March/April/May have plateaued at NT$410–417B, which looks like supply-constrained) gets you right at the midpt.

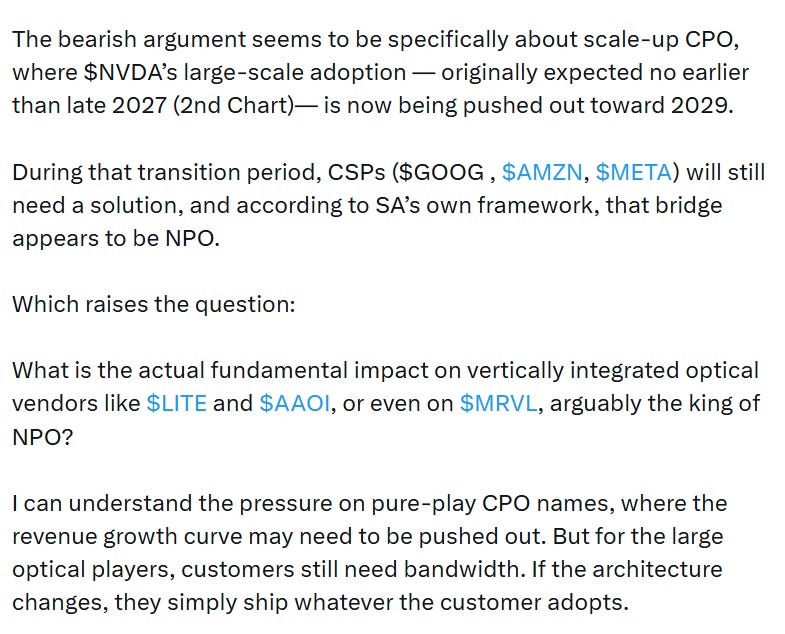

Optics: Morgan Stanley Says CPO Sentiment Has Reset, but the Long-Term Opportunity Remains Intact

Morgan Stanley addressed growing investor concerns around CPO and argued the recent pullback reflects a reset in expectations rather than a change in the long-term thesis. The firm now models 2027 optical engine shipments of roughly 6-7M units, well below some market expectations, citing downstream assembly yields of 20-50% and broader manufacturing bottlenecks as key constraints. While this pushes out the near-term CPO ramp, Morgan Stanley believes the industry remains at an inflection point, with CPO adoption beginning around 2028 and becoming increasingly important as scale-up and scale-out AI networks expand.

Power Infrastructure: Morgan Stanley Pushes Back on Rumors of an 800V AI Datacenter Delay

Morgan Stanley believes reports from Semianalysis that Nvidia may delay large-scale 800V datacenter deployments are being overstated and do not change its broader power infrastructure thesis. The firm notes 800V power racks are already being prepared for mass production and that development activity across hyperscalers remains on track, even if some standalone deployments slip modestly. Morgan Stanley argues the transition to 800V is being driven by fundamental increases in rack power requirements and remains necessary regardless of timing. The key takeaway is that any delay would likely reflect qualification, safety, and deployment timing considerations rather than a change in the industry’s long-term direction, with the broader 800V opportunity across power infrastructure and components remaining intact.