TMTB EOD Wrap

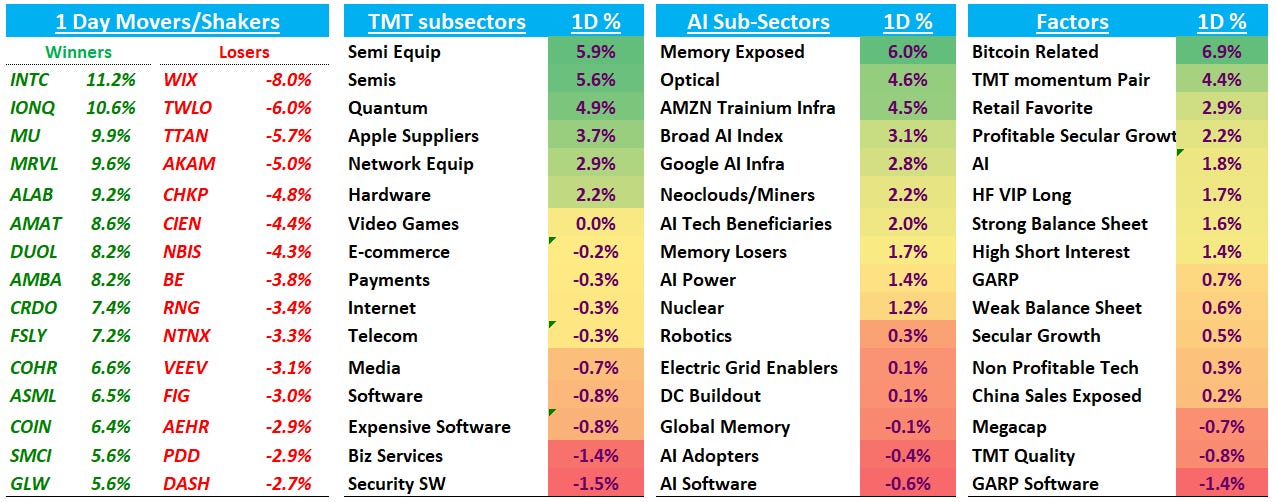

Good afternoon. QQQs +1.5% led higher by semis as large cap internet and software lagged. Memory and Semicap led the way higher for semis. From a factor point of view, Momentum outperformed. AAPL -2% as they disappointed on agentic AI at their WWDC event today. Yields fell 1-4bps across the curve.

Let’s get straight to the good stuff…

AI/SEMIS

MRVL +10% after announcement to join SP500. FLEX -1% lagged as only moving from SP400 to SP500. Digitimes had an interview withMRVL’s COO Chris Koopmans here where he said that MRVL has secured enough production capacity to meet its 50% growth target this year, 55% in 2027. He said MRVL’s SerDes now at 200G on the 2nm process and 500G on A14. Some other key quotes re: optical:

“Most people believe the limit is around 200G or 400G. Today, it is already very difficult to use copper transmission to interconnect 72 compute chips.”

“I believe NPO and CPO will be adopted gradually over the next five years... the scale-up field will basically move gradually toward optical transmission... it will move toward a CPO format.”

Semicap outperformed today. ASML +6% as Elon called it the greatest company in Europe and co. invite him to speak about Terafab. Other semicaps strong with AMAT +9%/LRCX +8%. Nothing to dislike in this group here as bulls continue to see a big disconnect between valuation and where earnings growth is going. The narrative is simple: if you believe the memory/AI supply story, the world is structurally under-supplied on the exact capacity that’s hardest to add (especially with HBM eating far more wafer capacity per bit than commodity DRAM), and equipment is the levered, lagging way to play it. If WFE goes to $250B in 2028, then implies AMAT multiple near 15x. Bulls think bottleneck noise is overplayed as higher-throughput litho platforms mean ASML won’t cap the ramp, so total WFE can keep climbing to 250B and beyond. Higher-throughput litho also means value acrruse to etch/depo, which is why some bulls prefer AMAT/LRCX vs. ASML.

INTC +11% after TheInformation confirmed GOOGL as a customer saying that GOOGL “recently placed an order with Intel to manufacture more than three million Tensor Processing Units in 2028, after months of testing Intel’s advanced packaging technology.” Some pointing that the word “manufacturing” is interesting, although this is very much likely for EMIB. GOOGL as a customer has been speculated by Asia press and others for a couple months now but the number of TPUs on order was new. TheInformation also confirming Nvidia running early trials on 18A.

GF Securities’ Jeff Pu was also out early morning with positive note on INTC saying they now expect Intel 3 capacity to increase ~80% and 18A capacity to double between 2026 and 2028, supported by external foundry customer commitments and improving manufacturing execution and highlighted Clearwater Forest as a meaningful server CPU catalyst, with production expected to begin in 3Q26.

Memory bouncing back nicely with MU +9% and SNDK +5% as street was out defending what was obvious late last week given the SoCAMM reductions at NVDA. Citi anod others said they expect no meaningful reduction in overall SoCAMM demand as memory suppliers remain capacity constrained and Nvidia prioritizes shipment volume, saying move actually helps NAND demand which we agree. We went into the rationale for better NAND demand in our weekly: