TMTB EOD WRAP

Good afternoon. QQQ -1% after what was largely interpreted as a more hawkish (we like to call it “non dovish) Fed update and presser. Here’s VK doing what he does best:

What was so hawkish about the Wed decision? It wasn’t just the 2026 dot (which jumped 40bp and is now penciling in 1 hike) or upward shift in the PCE forecast. Instead, it was the statement’s vow to deliver price stability, something Warsh strongly reiterated during the press conf. (“Members of the FOMC are unambiguous and unanimous in delivering price stability”). Every Fed chair commits to achieving price stability, but Warsh’s tone seemed particularly adamant.

Warsh declined to provide forward guidance, either hawkish or dovish: “financial market prices are the most important source of data, but we don’t want financial markets to simply react to Fed commentary and reflect back to us what we’ve already said.

So we’ll see if the market ends up testing him…

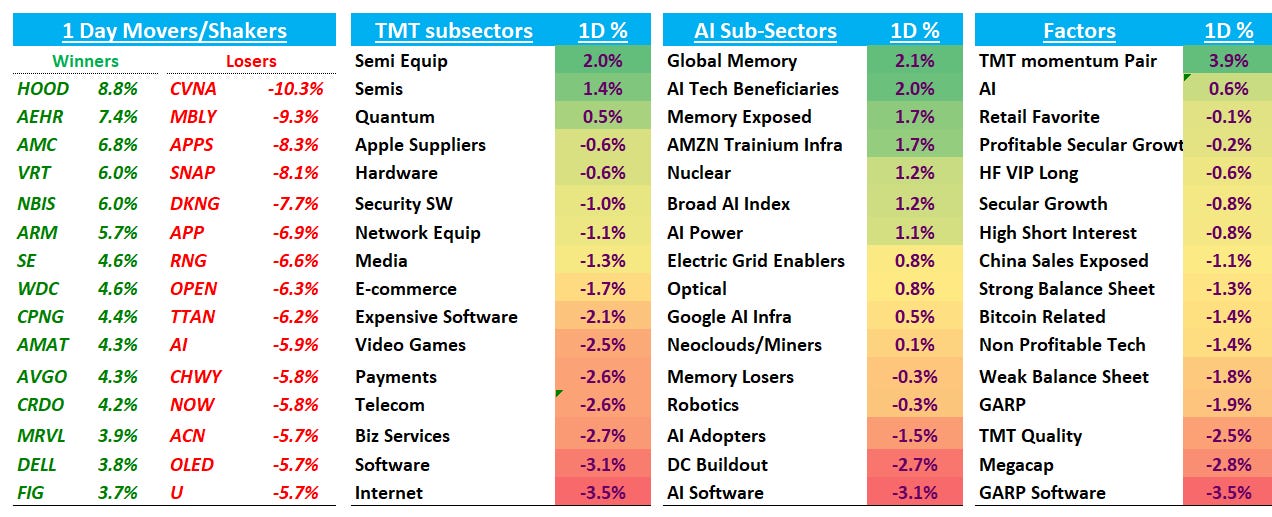

In Tech land, Semis outperformed while Internet and Software saw a lot of red. From a factor persepctive, TMT Mo outperformed +4% on the day while Megacap was particularly weak.

Let’s dive right in…

AI/SEMIS

AVGO +4.3% as JPM put out a pretty bullish note arguing elays or cancellation of Broadcom’s TPU v9 2nm program are unfounded, with checks indicating no delays and the TPU roadmap already extending through at least the next four generations. Harlan thinks TPU v9 could drive ~$250-300M of incremental FY28 XPU revenue and believes Broadcom is positioned to capture increasing TPU content through 2031 under its expanded agreement with Google. Wolfe was out saying Apollo/Blackstone financing vehicle could support triple Anthropic’s AI XPU volume versus FY25 levels, implying an incremental ~$250-300B of FY28 XPU revenue. Bulls continue think AVGO can do low to mid 30s of EPS in FY28 and prefer if focus stays on those numbers instead of margin/competitive concerns during this vacuum of news flow.