TMTB Weekly: A tactical bounce coming? What Tech Stocks to Buy

Another wild week in the books with QQQs -3.2% (dn 11% from highs at one point).

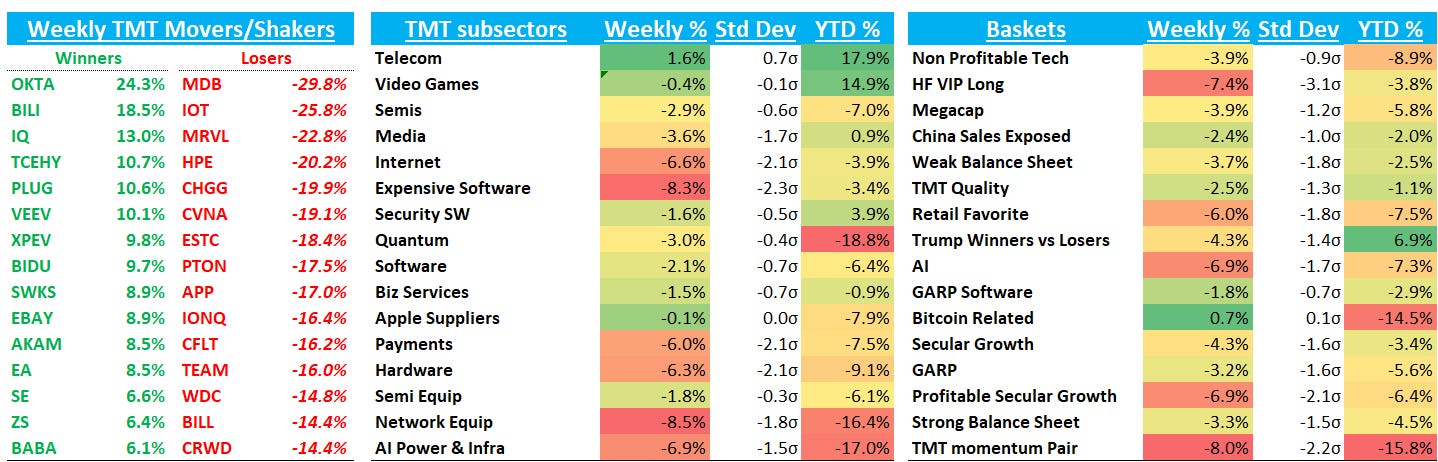

Here’s some of the carnage over the last 3 weeks in each sector:

Another wild week in the books with QQQs -3.2% (dn 11% from highs at one point).

Here’s some of the carnage over the last 3 weeks in each sector: