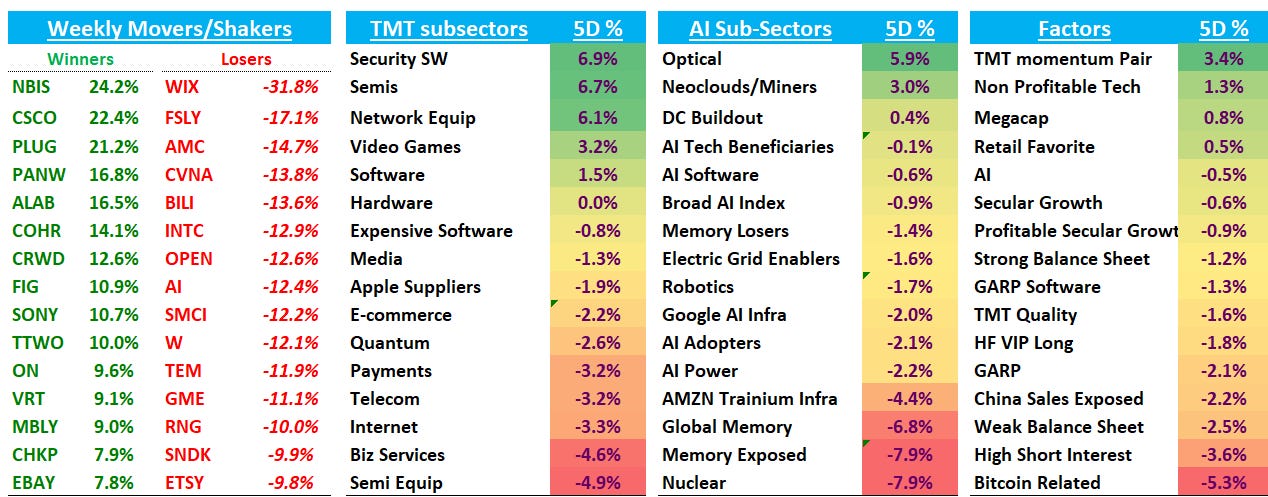

TMTB Weekly

Happy Sunday. We just got our first down week of the quarter with the NDX -40bps and SOX -160bps. After several weeks since the beginning of April where macro has been pushed to the kids table to make room for the HOT AI SUMMER vibes, it took a front seat again following hot CPI/PPI prints, Oil and yields hitting highs, fed expectations shifting hawkishly, and signs of a worsening consumer ahead of a critical week for Iran.

It’s been a while since we’ve touched on the macro — and we typically like it that way — but several crosscurrents are coming to a head that are worth paying attention to. Let’s start there before we dive in AI Semis and the rest of Tech.

First we got a raft of hotter inflation data, including US CPI/PPI, China CPI/PPI, Japan’s PPI, and the Empire State mfg survey (out Fri.) among other things.

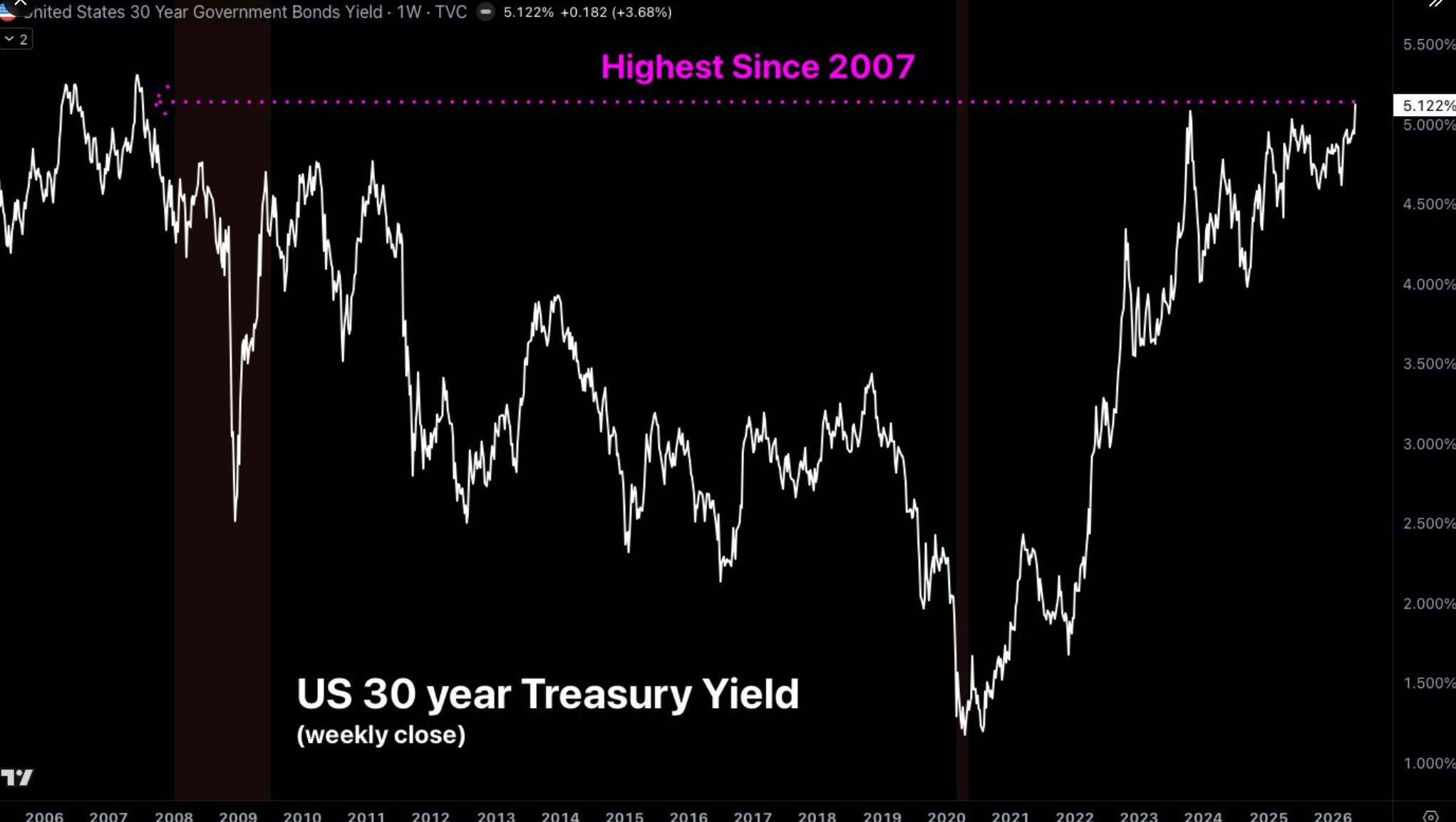

This caused yields to spike across the curve, with the 10 year above 4.5% and 30 year hitting 20 year highs:

This recent ramp in yields is not only driven by hotter inflationary prints but also the dynamics in Japan as higher JGB yields could cause Japanese investors to sell out of US Treasuries and repatriate cash back to Japan.

Fed expects are now pricing in a ~40% chance of a rate hike by the end of the year, which is a massive shift from not long ago when the market was expecting cuts. Yields and fed expectations are critical to us as they have typically been a catalyst for pullbacks in AI stocks. Remember back to the fall: Sam’s Splurge began in Sept and the SOX ramped through October, but it wasn’t until fed expects started shifting more hawkishly at the beginning of November that the market swooned and the narrative shifted.

While some argue that CPI/PPI readings are transitory and will normalize once the Iran situation is resolved, we believe that view oversimplifies a far more complex reality. The situation with Iran remains v. uncertain and as VK puts it “the best-case outcome is a vague, non-binding understanding that reopens Hormuz but leaves Iran in effective control of the waterway while a JCPOA-like understanding is reached on the nuclear issue.” While it seems very unlikely to us Trump will escalate, we still don’t know whether the White Hours will resume hostilities against Iran or engage on a variety of kinetic options.

There’s also an argument to be made that an Iran deal could trigger some “sell-the-news” action as the consensus view already anticipates an agreement and the focus would then shift to supply chain disruptions that aren’t likely to be alleviated for a longer period of time.

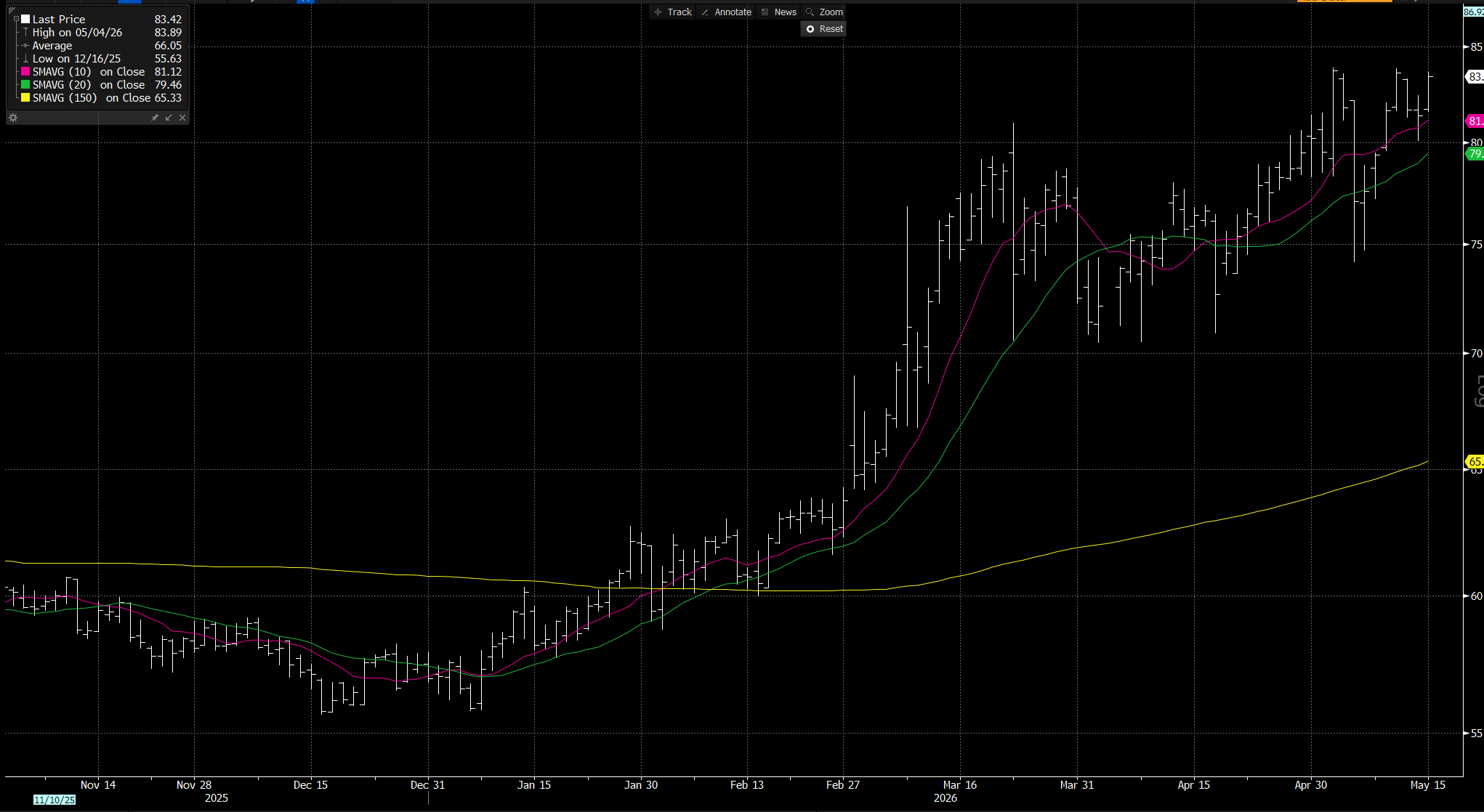

On that front, Oil inventory has helped keep a lid on Brent prices over the last 2.5 months, but excess supply will soon be depleted. December crude is already touching new highs:

The front-month chart looks like it wants to follow it higher: