TMTB Morning Wrap: TXN, Tesla, ServiceNow (NOW), IBM, SK Hynix Takeaways and Bull vs. Bear Debates; & Research/News

Good morning. Futures hovering around flat while Oil +1.5%. Overnight, US said for a response from Iran before the warring sides can restart peace talks.

Asia mixed overnight: TPX -0.76%, NKY -0.75%, Hang Seng -0.95%, HSCEI -0.79%, SHCOMP -0.32%, Shenzhen -1.05%, Taiwan TAIEX -0.43%, Korea KOSPI +0.9%. Softbank +4%; Hynix flat after reporting results.

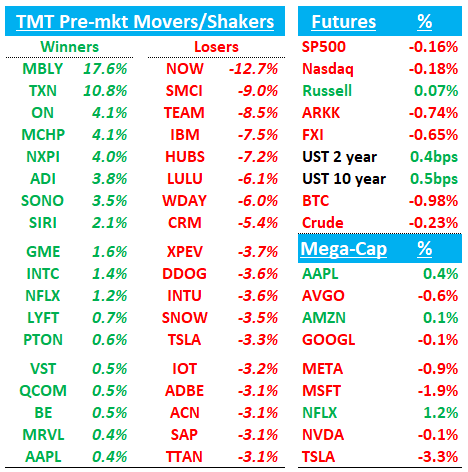

TXN +11% up big after a beat and raise, NOW -12% on weaker organic growth and margin guide; IBM -7% on a software decel getting dragged down by weakness in sw.

We’ll cover earnings first then get to the usual….

EARNINGS

NOW -13%: Decent Q1 with stronger AI, but the stock weaker on muddier organic growth optics because of “Middle East deal slippage”, acquisition noise, and lower near-term margin guidance. Bill with a sub-par performance on the call trying to explain away weakness

Subscription revenue was $3.671B, +22.2% y/y, +19.3% cc (last q +20.9% y/y, +19.5% cc) vs Street $3.653B, +~21.6% y/y; cRPO was $12.64B, +22.5% y/y, +21.0% cc (last q +25.0% y/y, +21.0% cc) vs Street $12.56B, +~21.8% y/y

The real issue was the guide. Q2 cRPO of +19.5% cc (below bogey of 20%) and FY26 subscription revenue growth of +20.5% to +21.0% cc both include 125 bps from Armis, so the organic read looked flat to down depending on which adjustments investors make, while Q2 operating margin of 26.5% and FY26 operating/FCF margins of 31.5%/35.0% came in below Street. Mgmt said Q2 and FY26 margin guides stepped down because of Armis dilution, Knowledge timing, and other integration/investment costs. Mgmt’s message was that the FY26 pressure is temporary and that margin expansion should normalize again in FY27

Offsetting that, NOW raised its 2026 Now Assist target to about $1.5B from $1B, said customers are moving from experimentation into broader enterprise deployment, and argued there was no broad demand deterioration outside timing-related Middle East disruption. Mgmt said pipelines remain healthy, public sector outperformed, large deals were strong, and customers are spending, but the environment is more complicated because enterprises are trying to sort out AI priorities and the Middle East conflict delayed several on-prem deals that hit revenue upfront. On the callback, mgmt said the cRPO beat was execution-driven rather than early-renewal-driven, that core enterprise renewals stayed solid, and that one of the slipped Middle East on-prem deals had already closed in Q2.

Bull vs. Bear Debate

The bull case is that this quarter did not break the long-term NOW story at all; it just made the bridge harder to see. Bulls will say the core platform remains one of the strongest large-cap software assets in the market, with real mission-critical status in IT workflows, expansion into CRM, employee, creator, security, and a new AI governance/control layer that is landing at exactly the right moment. The call was consistent with that view: mgmt framed AI as a tailwind, not a threat, argued that enterprise AI increases complexity and makes NOW more important, and highlighted differentiators like Context Engine, Workflow Data Fabric, AI Control Tower, and the hybrid pricing model. On top of that, the acquisitions are strategically coherent, not random. Armis adds visibility, Veza adds identity governance, and Moveworks strengthens the front door, all of which feed the same “control and compound” narrative.

Bulls will say they have enough quarter-specific proof points to stay constructive. Large-deal activity was strong, new logo ACV accelerated more than 50% y/y, CRM NNACV grew more than 5x y/y, AI Control Tower deal size more than doubled q/q, and customers spending more than $1M on Now Assist grew more than 130% y/y. In other words, bulls see the disappointing read-through as mostly optics, not evidence that demand or competitive positioning is cracking. They would also point to 50% of net new business now coming from non-seat-based pricing, which matters because it reduces the simplistic “AI kills seats, therefore NOW’s model is impaired” argument

The bear case is that the quarter confirmed exactly what skeptics feared: AI enthusiasm is real, but it is not yet showing up cleanly in underlying organic growth, and the M&A strategy may be masking a slower core. Bears will say the strongest datapoint for that view is not Q1 itself, but what happened to the organic setup once Armis, Moveworks, Veza, and Pyramid are stripped out. The FY26 guide looks basically flat organically at best, slightly down at worst depending on adjustments, and the Q2 organic cRPO read was below bogeys. For a stock that needed a clean organic re-acceleration, that’s a big hurdle to overcome. If the AI target went up by $500M, but the core guide did not go up with it, bears will ask whether AI is mostly incremental packaging optics today rather than material revenue acceleration.

Bears also have enough smaller negatives to keep pressure on the narrative. Q1 subscription beat magnitude was the weakest in years, renewal rate dipped to 97%, FCF missed, and margin guidance stepped down meaningfully. The company is also asking investors to look through a lot at once: a geopolitical issue in the Middle East, multiple acquisitions, termination-for-convenience contract treatment, lower profitability in acquired businesses, and a future analyst day where the long-term bridge will supposedly become clearer. That can work eventually, but in the near term it invites skepticism. Bears will also argue that while NOW clearly has strong AI products, it still has to prove that those products can outrun the Anthropic will eat software noise.

TXN +10%: Solid beat-and-raise, with the narrative shifting more clearly toward a broad industrial recovery, accelerating AI/data-center power content, and a much better FCF setup as capex rolls down.

All around solid print and bullish call. Revenue was $4.825B, +18.6% y/y (last q +10.4%) vs Street about $4.52B, +~11%; EPS was $1.68 vs Street $1.36; GM was 58.0% vs Street about 56.2%; and 2Q guidance was $5.20B at the midpoint, +16.9% y/y vs Street about $4.85B, +~9%, with midpoint EPS of $1.91 vs Street $1.57. The beat was driven by industrial and data center, while auto held flat sequentially and personal electronics was better than feared.

The key message from mgmt was that pricing did not drive 1Q, but the pricing backdrop is now better and could become a 2H tailwind if demand stays firm. Mgmt sounded bullish, but still conservative on calling the 2H too early, explicitly referencing last year’s false start and the broader macro/geopolitical backdrop.

Key takeaways:

Industrial was the biggest positive surprise. Mgmt described growth as broad across sectors, geographies, and customer sizes, not just a narrow recovery in a few hot pockets. With industrial still roughly 15% below the prior peak, matters for bull case

DC Revenue grew about 90% y/y and more than 25% q/q, and mgmt sounded increasingly confident that application-specific AI power sockets start layering in more meaningfully in 2H26 and into 2027.

Margins improved faster than expected. GM at 58.0% beat Street by roughly 180-190 bps, and the 2Q guide implies roughly 59.5-60.0%, supported by better mix, operating leverage, and a pricing environment that is no longer drifting down

Pricing was not the reason for the 1Q beat, but it is now an upside lever. Mgmt said price was flat in 1Q and should look similar in 2Q, but also acknowledged the analog pricing backdrop has improved and prices may rise in 2H if demand remains strong

Q1 auto was flat q/q, with China down and rest of world up. Mgmt framed auto as steady near peak levels and still supported by secular content growth

Inventory days fell to 209, lead times stayed stable, and mgmt repeatedly emphasized having enough inventory and Phase 3 analog capacity to serve demand and take share if competitors are constrained

Gets an upgrade at BofA

Bull vs. Bear debate

The bull case is that TXN is finally lining up all the pieces bulls have wanted for the last two years: industrial is broadening beyond a narrow set of verticals, data center and AI power are becoming large enough to matter, pricing has stopped declining, and the company is moving out of its heaviest capex phase. Bulls will say 1Q beat was not just a restocking quarter. It was the first clean look at a model where better mix, better loadings, lower capex, and share gains can happen together. The added bull twist this quarter is that data center is no longer just a vague AI adjacency. Mgmt talked explicitly about general-purpose rack content, Stage 1 and Stage 2 power conversion, VRMs, GaN, advanced BCD, and application-specific sockets ramping in 2H26 and into 2027. Bulls can now argue for roughly 11-15% revenue CAGR from 2025 through 2028, with a much steeper EPS and FCF inflection than street had embedded before the print, which means something like $11-13 of EPS power over the next few years and desreves a premium multiple of 30x +

The bear case is that this still looks like TXN at the early stage of an analog upcycle, which is exactly where false starts and over-extrapolation often happen. Mgmt itself kept coming back to caution, explicitly noting that 2025 also started strong before cooling, and that it wants to see 2Q play out before getting more confident on the second half. Auto is steady but not accelerating, China within auto was down in 1Q, personal electronics has not yet fully reflected the possible knock-on effects from higher memory costs, and inventory days at 209 are still elevated in absolute terms even if the direction is better. Bears will also argue that industrial can look deceptively strong in the early innings because distributor and customer replenishment can masquerade as durable end demand. And while margins improved sharply, bears can still point to depreciation, inventory, and utilization as variables that can cap upside if growth softens again. Bears will say 30x is too high a multiple for a cyclical analog and deserves closer to ~25x

TSLA -3%: Headline beat, but the stock is weaker as nits are 1Q quality was helped by one-timers while Elon raised Capex to $25B, FCF neg for the year, pushed back back AI5 chip / robotaxi monetization while Optimus and Semi ramps expect to slow

TSLA reported Revenue $22.387B, +15.8% y/y (last q -3.1% y/y) vs Street $21.417B, +~10.8% y/y; Non-GAAP EPS $0.41, +51.9% y/y vs Street $0.33.

Auto GM ex-credits was 19.2% vs Street 15.4%, but that included roughly $230M of warranty benefit plus some tariff relief;

Energy GM was 39.5%, but also included more than $250M of tariff recognition benefits.

FCF was $1.444B vs Street -$1.575B, helped in part by capex of just $2.493B vs Street roughly $4.109B.

FY26 capex now expected above $25B with negative FCF for the rest of the year

Key Takeaways:

Mgmt raised FY26 capex to >$25B from >$20B, framed 2026 as the start of a multi-year heavy investment cycle, and explicitly said FCF should be negative for the rest of the year. The spend is going into six factories, AI infrastructure, the Austin research chip fab, solar equipment, Cybercab, Semi, Optimus, and battery/manufacturing capacity

Mgmt said EMEA rebounded strongly, with France and Germany up more than 150% q/q in deliveries, APAC improved in South Korea and Japan, the U.S. was modestly up q/q, and the quarter ended with the highest Q1 order backlog in over two years. Mgmt also emphasized that the order-rate improvement started before the recent rise in gas prices, implying the demand improvement was not purely a commodity-price bounce

Mgmt said tariffs and sustained high rates continue to pressure automotive costs via financing subvention, and the energy business remains especially exposed because many cells are sourced from China. On top of that, several analysts in the pack still frame 2026 as a slower EV demand year with tougher competition and reduced subsidy support.

Said FSD customers reached roughly 1.28M to 1.3M, bulk growth came from subscriptions, churn is falling, and mgmt said it now markets FSD as the product with the vehicle acting as the delivery mechanism. The Netherlands approval set up a potential EU-wide supervised rollout later in 2Q, while China approval is targeted for 3Q.

The most important incremental negative from the call was the HW3 admission. Mgmt said Hardware 3 cars cannot achieve unsupervised FSD, which means discounted trade-ins, computer/camera retrofits, and potentially a new cost burden via local retrofit “micro-factories.”

Unsupervised service is now in Austin, Dallas and Houston; mgmt still targets roughly a dozen states by year-end; and it said there have been zero injuries or fatalities so far. But mgmt also said robotaxi revenue will not be super material this year, with more meaningful revenue only next year.

Cybercab, Semi, Megapack 3, and Optimus all remain “on track,” but the common theme was slow initial ramps. Cybercab and Semi have started or are about to start production, but mgmt repeatedly described the normal new-product S-curve and warned initial output would be very slow. Optimus production is now framed around a late July/August start in Fremont, with no real unit guide for this year and a second factory only next summer