TMTB Morning Wrap; HPE Earnings Takeaways & Tech Research/News

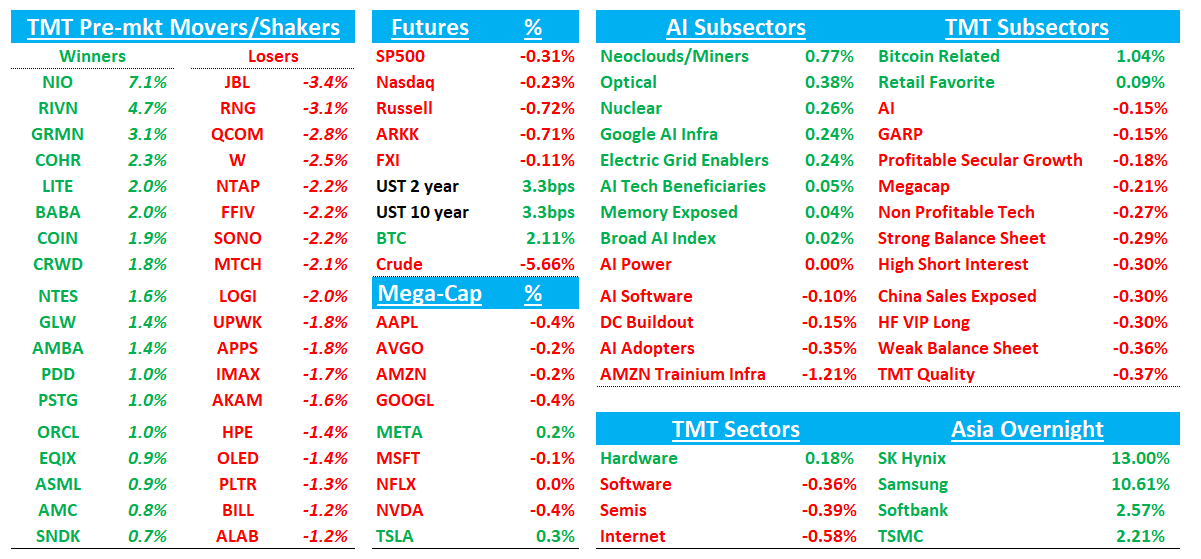

Good morning. Futures -25bps and Oil down another 5-6%. BTC +2%. Yields ticking up 3bps across the curve. Asia green across the board: TPX +2.47%, NKY +2.88%, Hang Seng +2.17%, HSCEI +1.5%, SHCOMP +0.65%, Shenzhen +1.84%, Taiwan TAIEX +2.06%, Korea KOSPI +5.35%. Memory names strong with Hynix +13% and Samsung +10%.

We get ORCL Earnings tonight.

Lots to get to so let’s get straight to it…HPE Earnings First then the usual…

HPE: Solid Q although revenue was a touch light, but EPS, margins better than feared given memory inflation. Networking up LDD% including DC switch orders up mid 40s and routing up mid20s.

Key #s / Takeaways:

Revenue was $9.301B, +18.4% y/y (last q +14.4% y/y) vs Street about $9.33B-$9.35B, +~18.8%-19.0% y/y; EPS was $0.65 vs Street $0.58-$0.59; non-GAAP gross margin was 36.6% vs Street 35.8%

Networking revenue was $2.706B, +152% y/y reported / +~7% normalized vs Street about $2.70B, and HPE raised FY26 networking growth to 68%-73%

Cloud & AI revenue was $6.334B, -2.7% y/y vs Street about $6.4B, and HPE again pushed most AI revenue weight into 2H, with Q3 called out as the biggest AI revenue quarter and AI backlog above $5B

FY26 revenue guidance stayed at +17% to +22% reported / +5% to +10% normalized, but EPS moved to $2.30-$2.50 and FCF to at least $2.0B. Mgmt noted better mix, not higher volume: networking up, Cloud & AI down, with HPE assuming ongoing memory inflation, some 2H elasticity, and still saying supply is the main constraint.

Mgmt repeatedly said demand is very strong, there are no pushouts, no cancellations, and no signs of double ordering, while also acknowledging some pull-ins and embedding some 2H demand elasticity into the outlook

AI server revenue is still expected to be heavily back-half weighted, with Q3 the biggest AI quarter, and the callback reiterated that this is more about customer readiness and sovereign timing than HPE losing demand.

Mgmt’s callback tone was cautious on 2H, but not because demand is weakening. The message was that customers are still accepting higher pricing, orders remain healthy, and HPE is simply baking some elasticity into 2H planning.

JNPR synergy execution remains on track, with about $200M expected in year one, and the callback was clear that AI networking is running ahead of prior expectations and is the more structurally accretive part of the AI story.

Bull vs. Bear Debate

Bulls say HPE is no longer just a low-multiple server/storage name. JNPR acquisition has materially changed the mix, networking is now nearing 30% of revenue and more than half of operating profit, and the networking growth engine is broadening across campus, switching, routing, and networks-for-AI. That matters because networking carries structurally better margins, lower memory exposure, and a cleaner AI-adjacent demand profile than AI servers alone. Bulls also like that HPE is seeing demand across traditional servers, storage, and networking at the same time, which suggests this is not purely an AI server story. This quarter helped that argument: the networking guide went up, the overall revenue guide stayed intact, and profitability beat despite the exact cost backdrop most investors were worried about.

Bulls will also argue that HPE is setting up for a multi-year EPS/FCF improvement cycle, not just a one-quarter beat. Juniper synergies are on track, HPE reiterated long-term targets of at least $3 EPS and more than $3.5B of FCF by FY28, and the callback added that services attach should improve as enterprise and sovereign AI projects scale. On valuation, the bulls say this deserves 11x-12x P/E, with the top end defendable if HPE keeps proving it deserves to trade more like a higher-margin networking name; on $3.0 of CY27 EPS, that = $33-$36 per share.