TMTB Morning Wrap; Google, Amazon, MSFT, META KLAC EQIX & more earnings roundups

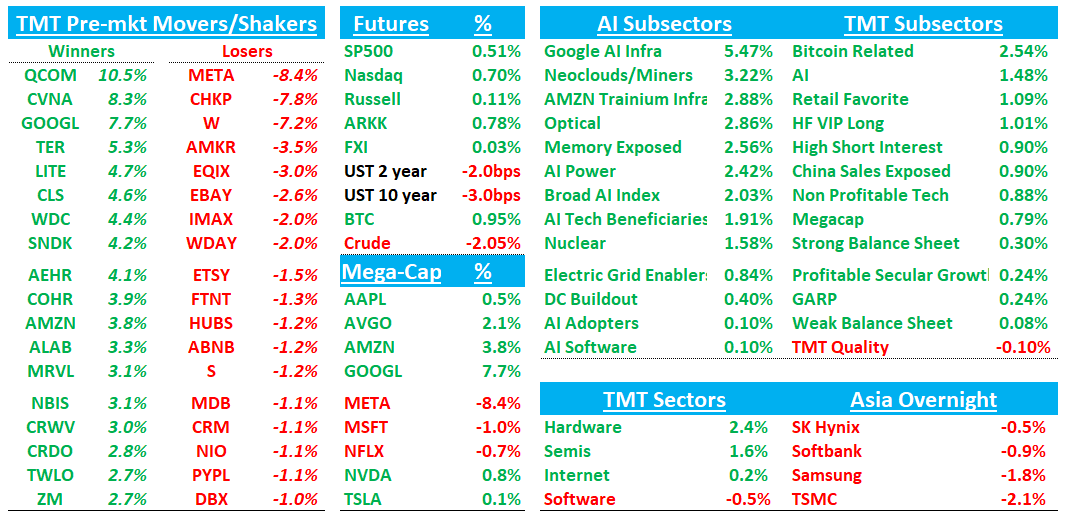

Good morning. Futures +70bps on the back of a set of solid prints from GOOGL and AMZN, a decent one from MSFT, and a so-so one from META. A lot of similarities among the 4 however with the obvious message that AI/compute is still the biggest priority and focus among all 4.

Capex roundup from last night:

MSFT: implying C2H26 capex at ~$59bn quarterly run-rate vs. F25 run-rate of ~$36bn +64% YoY

META: bump up capex from $125bn -> $135bn — +87% YoY

GOOGL: bump up capex from $180bn -> $185bn — +102% YoY…saying CY27 will be up significantly from 2027 (conversations overnight have buyside thinking $275B)

AMZN: no change at $200bn — +52% YoY

Trainium and TPU names catching a bid early….NVDA +1% / AMD +3%, the latter on a META mention.

We’re going to dive straight in since there’s a lot to get to…

We’ll hit GOOGL, AMZN, MSFT, META, KLAC, EQIX, Mediatek, and Samsung. Alright here we go…

GOOGL: Cleanest large-cap internet print of the night: Search and Cloud both beat, Cloud backlog/TPU disclosures supports bull narrative

Let’s start with the cleanest of the night. Overall, great numbers here with search growing 19% and GCP showing the 6-handle bulls wanted. YT inline-ish was only nit. Thought the call went very well with mgmt doing a great job describing why bulls love GOOGL: they’re only company that has silicon cloud and models and are top 3 in every category. Raised capex $5B and said 2027 capex would increase significantly to 2026. Bulls think this means ‘26 capex of $200B goes to $275B+, or 40% growth (significantly is a very wide band but commentary was very bullish around spend). Buyside numbers here going up to close to $16 in ‘27 EPS vs $15 previously. 25x = $400, which is less than 10% upside from here but bulls will make the case — and they have a good one - that this should trade closer to 30x in an “AI world” where GOOGL is arguably the best positioned hyperscaler. If GOOGL manages to accelerate search revs from 19% in the face of tougher comps the next few quarters (TBD) while GCP likely ramps into high 70s/80s, we think that 30x argument becomes even more credible. We love the narrative here and think it’s a must own in LT book, but think AMZN presents a higher upside bull case and better “rate of change” narrative (more below)…

The #s:

Revenue was $109.896B, +21.8% y/y (+18.7% FXN; last q +18.0% y/y) vs Street ~$106.9–107.0B, +~18–19%.

Search printed $60.399B, +19.1% y/y (last q +16.7%) vs Street ~$59.0B, +~16% and bogeys of 17-18%, while Cloud printed $20.028B, +63.4% y/y (last q +47.8%) vs Street ~$18.4B, +~50%. Backlog was $462B nearly double q/q. YouTube was the soft spot at $9.883B, +10.7% y/y vs Street ~$10.0B, +~12%, while GAAP OI was $39.696B, +29.7% y/y vs Street ~$36.2–36.4B.

FY26 capex guide moved to $180–190B from $175–185B, and mgmt said FY27 capex will “significantly increase”; TPU revenue starts small in 2026 with the majority recognized in 2027

Key Takeaways:

Search revenue accelerated to +19.1% y/y, the best growth in years, with mgmt saying queries are at an all-time high and AI Overviews / AI Mode are increasing usage rather than cannibalizing Search. AI is expanding query volume and helping monetize longer, more complex queries that were historically harder to serve ads against.

Cloud revenue grew +63.4% y/y and beat Street by ~9–11% and inline with bogeys, but the bigger surprise was backlog of $462B, nearly doubling q/q, with just over 50% expected to convert to revenue in the next 24 months. Mgmt said enterprise AI solutions became Cloud’s primary growth driver for the first time, revenue from products built on GOOGL GenAI models grew ~800% y/y, new customer acquisition doubled, $100M–$1B deals doubled, and existing customers outpaced initial commitments by 45%

OOGL will deliver TPU hardware to select customers in their own data centers, with a small revenue contribution later in 2026 and the majority in 2027. That supports the vertical-integration bull case and expands Cloud’s addressable market, but it also creates a bear pushback around the “quality” and comparability of Cloud revenue as GCP, Workspace, Wiz, and now TPU hardware become increasingly intermingled.

Mgmt cited Retail, Finance and Health as key Search vertical contributors, said all major verticals contributed, and said demand for AI compute was “unprecedented” internally and externally.

YouTube was not bad, but it was the “less clean” part of the print. YouTube ads grew +10.7% y/y vs Street around +12%, though mgmt highlighted living-room usage above 200M hours/day, 10M+ Shorts channels publishing daily, YouTube subscriptions growing faster than ads, and the strongest non-trial YouTube Music/Premium subscriber add quarter since launch.

Bull vs. Bear Debate:

The bull case is that GOOGL is now proving AI is not a threat to Search, but a demand and monetization accelerator while they own the full AI stack. The core Search business grew +19% y/y, queries are at all-time highs, AI Overviews and AI Mode are increasing usage, and Gemini is expanding the monetizable surface area by understanding intent in longer and more complex queries. Bulls also point to AI-enabled campaigns already representing more than 30% of customer Search spend, which supports the idea that AI is improving advertiser ROI rather than compressing it. The agentic commerce and UCP commentary adds another leg to the story: GOOGL is not just defending Search, it is trying to collapse discovery, comparison, checkout, and post-purchase flows into Search / AI Mode / Gemini.

The second bull leg is Cloud and infrastructure. Cloud revenue accelerated to +63% y/y, backlog nearly doubled to $462B, and enterprise AI solutions became the primary growth driver. Bulls see this as evidence that GOOGL’s vertically integrated stack, models, TPUs, security, data, Workspace, and GCP, is becoming a durable competitive advantage against AWS, Azure, and AI-native infrastructure platforms. TPU hardware sales to external customers are especially important because they could turn a historically internal advantage into a merchant-silicon-like revenue stream while increasing scale benefits across GOOGL’s AI infrastructure.

The bear case not very strong and is not that the quarter was weak; it is that the market may already be capitalizing a lot of the AI upside while underestimating the capex, depreciation, and FCF drag required to sustain it. FY26 capex is now $180–190B, FY27 is expected to “significantly increase,” and buyside conversations are moving toward numbers like ~$280B. That creates a real duration problem for FCF, especially with FCF down ~47% y/y in Q1 and no share repurchases during the quarter. Bears will argue that AI demand looks outstanding today, but if demand normalizes or pricing weakens, the fixed-cost base, depreciation, power, and data center operating costs could pressure margins faster than consensus expects.

The second bear argument is competition and revenue quality. AI-native products from OpenAI, Anthropic, Perplexity and others still represent long-term risk to Search distribution and commercial queries, especially if consumer agentic workflows move away from classic search pages. Bears will also argue that Cloud’s reported number is becoming harder to parse as Workspace, Wiz, GCP, AI infrastructure, and TPU hardware are all in the same segment. TPU revenue may be attractive, but it could also make Cloud growth lumpier, lower-quality, and less comparable to hosted cloud revenue. YouTube and Network were also reminders that not every ad bucket is accelerating.

AMZN: 1Q26 #s looked solid despite AWS +28% coming in slightly below bulls hopes for a 3-handle. Stock narrative continue to flip from “AWS AI laggard / capex drag” toward “AWS AI demand, Trainium visibility, and margins better than feared.”

Overall, solid set of numbers and call commentary was bullish helping stock reverse from -3% to +3%. Q2 EBIT guide of $24B at the high end better than fears of lower and AWS margins near 38% upticked q/q vs. concerns that the Anthropic ramp would eat into that.

Call also had some pretty bullish points: 1) $225bn+ in rev commitments for Trainium. Mgmt said they see potential to sell Trainium racks externally “very much a possibility” over the next few years; 2) 1Q backlog $364bn (+49% q-q), and is exclusive the $100bn+ from Anthropic last week. Mgmt also called out accelerating customer conversations of on-prem to cloud migration due to supply chain inflation.

Numbers maybe going up slightly here, but don’t get sense they are moving much with bulls still at $13 for ‘27 GAAP EPS. While GOOGL has cleanest narrative, AMZN continues to have the biggest “rate of change” narrative (meaning, most exiting) among the 4 and also the most upside as bulls hope EBITDA gets back in the 15x+ range with an AWS accel getting close to a 4-handle later this year. Stay the course long here.

The #s:

Revenue was $181.5B, +16.6% y/y, +15% FXN, versus Street $177.2B, +~13.9%; OI was $23.9B, +29.6% y/y, 13.1% margin, versus Street $20.8B, 11.7%.

AWS was the center of the print: revenue $37.6B, +28.4% y/y, versus Street $36.7B, +~25.3%, with AWS OI margin 37.7% versus Street ~33.9%.

2Q revenue guide of $194-$199B was above Street $189.9B; 2Q OI guide of $20-$24B bracketed Street, with the $24B high end better than feared despite SBC, fuel, and Leo headwinds.

Key Takeaways:

AWS OI was $14.2B, +22.6% y/y, with margin 37.7% versus Street ~33.9%. Investors had worried AI workloads, Anthropic ramp, GPU dependence, and depreciation would push AWS toward low/mid-30s margins. Instead, the quarter showed AWS can absorb heavy AI investment while still printing high-30s margins, though hearing some on buyside still assuming a low-30s steady-state.

Mgmt disclosed the chips business is now >$20B annual revenue run rate and growing triple-digit y/y, or ~$50B if treated like a standalone chip vendor selling to AWS and third parties. Trainium2 is largely sold out, Trainium3 is nearly fully subscribed, and much of Trainium4 is already reserved roughly 18 months ahead of broad availability. Mgmt also said selling Trainium racks externally over the next couple years is “very much a possibility.”

Mgmt cited AI revenue run rate of >$15B, Bedrock customer spend +170% q/q, Bedrock processing more tokens in 1Q than in all prior years combined, and 125k+ Bedrock customers. The broader IT spend point was also constructive: AI spend is pulling through core AWS demand, and memory/storage inflation is pushing some on-prem customers faster into cloud migration.

Retail demand looked resilient. Units grew +15% y/y, the strongest since the tail end of COVID lockdowns. Mgmt cited strong 3P seller performance in the U.S., Europe, and Brazil, plus grocery and same-day perishables as frequency drivers. Customers using same-day perishables add nearly 3x as many items and spend >80% more than those who do not, which supports the bull view that grocery can increase retail frequency even if near-term mix can be lower margin.

Ads revenue was $17.2B, +23.9% reported and +22% FXN, versus Street $16.9B. Rufus monthly active users were up >115% y/y and engagement nearly +400% y/y. Mgmt pushed back on agentic-commerce disintermediation risk, arguing that multi-turn shopping conversations create more opportunities to surface relevant organic and sponsored products.

Bull vs. Bear Debate

The bull case is that AMZN has moved from being perceived as an AI infrastructure laggard to one of the clearest AI beneficiaries in mega-cap tech. AWS reaccelerated to +28.4% y/y on a $150B annualized run-rate base, AI revenue is already at a >$15B run rate, and backlog has stepped up to $364B before including the latest >$100B Anthropic deal. The quarter also showed that AI demand is not purely a GPU capacity story. Mgmt’s pitch is that AI workloads pull through core AWS services, CPU demand, storage, security, databases, and analytics, and AMZN’s integrated Trainium plus Graviton stack can deliver differentiated economics. That matters because the biggest historical bear case was not “AI demand will not exist,” but “AMZN will spend heavily and earn lower returns.” This quarter gave bulls data points against that: high-30s AWS margins, accelerating AWS growth, very large Trainium commitments, and better visibility into the revenue pipeline.

The second bull argument is that retail, ads, and services mix are doing more work than investors appreciate. Units +15% y/y, 3P services +13.9%, ads +23.9%, and NA OI margin of 7.9% all point to operating leverage outside AWS. Grocery and same-day perishables increase purchase frequency, Rufus can raise conversion and create new sponsored ad inventory, and the service mix shift toward AWS, Ads, Subscriptions, and 3P is structurally margin accretive. Bulls also like the optionality from Leo, Alexa+, Health AI, and Zoox, although Leo is the one that is starting to become more visible as both a cost drag and a potential medium-term revenue platform.

The bear case is that the quarter did not eliminate the two hardest questions: whether AWS can keep accelerating enough to justify the capex cycle, and whether AWS margins can stay near high-30s as AI capacity, depreciation, and large AI customer commitments ramp. AWS growth of +28.4% was strong, but the setup into the print had some investors looking for ~30% in 1Q and mid-30s in 2Q. The 2Q revenue guide can be interpreted as low-30s AWS growth if the Prime Day contribution is small, but it is not an unambiguous mid-30s signal. Bears also note that Azure and Google Cloud are still growing faster in AI-related workloads in several comparisons, and that AMZN remains in a catch-up phase after a period when the market viewed it as capacity constrained.

The second bear argument is that FCF and capital intensity are still deteriorating. Q1 FCF was negative $17.2B and cash capex was $43.2B. Even if mgmt says investments will monetize 6-24 months later, investors still have to underwrite hundreds of billions of dollars of capex with a long lag before cash returns. Leo, Zoox, and other long-duration bets add complexity, and Q2 OI guidance embeds another ~$1B of Leo cost, a seasonal SBC step-up, and fuel inflation. Bears also worry that retail growth mix may be less profitable if grocery, perishables, and 1P everyday essentials grow faster, while tariffs, fuel, memory inflation, and macro pressure could erode consumer or infrastructure margins. Agentic commerce is another theoretical risk if third-party agents weaken AMZN’s control over the shopping journey, even though mgmt pushed back strongly on that.

Yup the bulls have it…