TMTB Morning Wrap

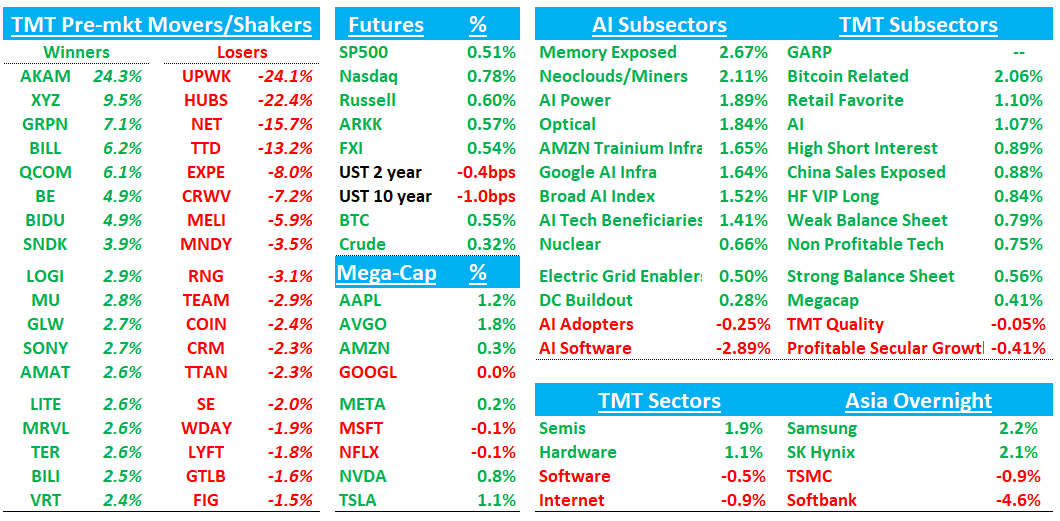

Futures +80bps to start this beautiful Friday morning as the market brushes up a flareup in tensions between US and Iran overnight (fire was exchanged around SoH) but ceasefire remains intact and Trump called it “just a love tap.” What a poet.

Asia mixed: TPX -0.29%, NKY -0.19%, Hang Seng -0.87%, HSCEI -0.34%, SHCOMP flat, Shenzhen +0.12%, Taiwan TAIEX -0.79%, Korea KOSPI +0.11%. Samsung/Sk Hynix +2% continue to rally.

In tech land, HUBS -22% blow up showing app sw not in same league as consumption sw after DDOG’s beat yesterday, AKAM rallying on a big deal, NET down on an expects miss, MCHP the latest analog to beat, CRWV down on a weaker guide, ABNB looks solid, QCOM continues to squeeze the shorts, and more. Outside of that, AI semis strong early with SNDK +4% / MU +3% leading the way higher.

We’ll cover earnings first then get to the usual.

NET -15%: Revenue beat on Revs, but Q2 guide only inline with street and missed bogeys. Surprise ~20% RIF, gross margin compression, DBNRR/RPO deceleration and tougher comps ahead

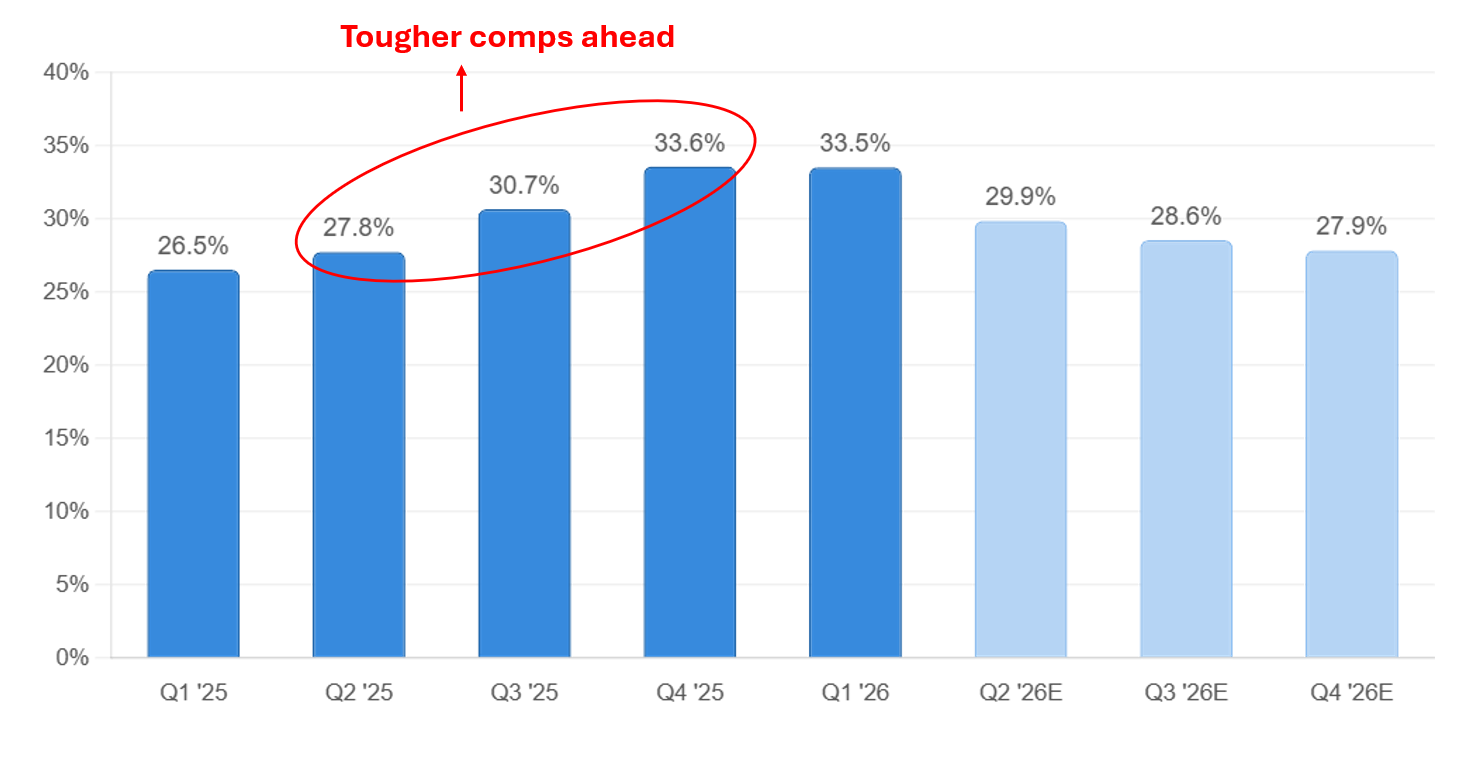

Top line numbers looked fine for the quarter with a beat of ~3%, about in line for the last several quarters, but the GM miss and DBNRR/RPO decel a bit concerning. Still not all was bad: huge workers adds, customer adds strong, raised FY guide on a Q1 print for first time in 3 years, new customer bookings highest since 2023, pipeline generation fastest sequential growth in five years, and gross retention highest in four year. Call sounded bullish with mgmt talking up AI agentic tailwinds. In terms of optics, what’s concerning for us is that you have a period of tougher comps ahead where it’s possible to see NET revs decel back to ~30% or lower range after a period of easier comps when revs were accelerating:

Despite NET having one of the strongest Agentic AI tailwinds and Workers momentum remains strong (1M adds in Q1 alone vs 1.5M in all of 2025; large customer additions strong), we typically don’t like to be involved in a high multiple stock when revs are likely going to decelerate/flat line in the upcoming quarters, especially on the back of several quarters of acceleration and a q with some mixed metrics. We are still biased long, but we sold our small position last night and we’ll wait for stock to digest before a potential better set up/entry for a long. Overall - stock deserves to be down on expects miss, but underlying numbers still strong and we think bull case remains intact.

The #s:

1Q26 revenue was $639.8M, +33.5% y/y (last q +33.6%) vs Street $620.8M, +~29.6%, and EPS was $0.25 vs Street $0.23. Gross margin was the weak spot at 72.8% vs Street ~75.1%-75.2%, while FCF was better than expected at $84.1M, 13% margin.

2Q26 guide was $664M-$665M, +~29.7% y/y vs Street ~$663M, +~29.4%, and FY26 revenue guide was raised to $2.805B-$2.813B, +~30% y/y vs Street ~$2.790B, +~28.7%.

Key Takeaways:

Mgmt framed agentic AI as a tailwind across Act 1, Act 2 and Act 3: more agentic requests for application traffic, more need for fine-grained data access in Zero Trust/SASE, and more developer demand for Workers. Workers added 1M developers in 1Q alone, bringing the platform to 5.5M+ developers, versus 1.5M additions in all of 2025. Agentic traffic was described as growing exponentially, with January doubling and April reaching hundreds of billions of requests; this is already pulling demand into request-cap increases, bot management, and legacy application/security products.

Customers paying >$100K reached 4,416, +25% y/y, and revenue from that cohort grew 38% y/y, contributing 72% of revenue vs 69% y/y. Deals over $1M grew 73% y/y, and NET added as many $5M+ customers in 1Q as it did in all of 2025. New customer bookings highest since 2023, pipeline generation fastest sequential growth in five years, and gross retention highest in four year

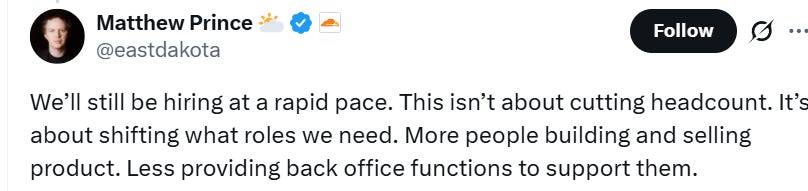

NET announced a reduction of 1,100+ employees, roughly 20% of the workforce, across functions and geographies. Mgmt insisted it is not a cost-cutting exercise and said quota-carrying sales capacity is protected, with net AE capacity still expected to accelerate in 2026. The callback framed the RIF as a growth acceleration move with AI being used to collapse sequential workflows into parallel processes, support ratios for AEs are improving, and roughly half of savings were described as flowing through while the rest is reinvested into growth functions like quota-carrying reps.

FY26 operating income guide was raised meaningfully to $418M-$421M vs Street ~$382M, implying ~15% OM. But gross margin fell to 72.8%, well below Street, due to free-to-paid traffic reclassification and Workers mix. Mgmt said operating margin and unit economics are better indicators than gross margin as product mix shifts.

DBNRR fell to 118% from 120% q/q, though still up 7 pts y/y. RPO grew 36% y/y, down from 48% last q, with q/q RPO adds viewed as light. Bulls will point to the tough comparison from a large prior-year $100M+ deal and the mechanics of pool-of-funds contracts

Bull vs. Bear Debate

Bulls see NET as one of the cleanest software infrastructure beneficiaries of AI. The core argument is that agentic workloads multiply internet requests, increase the value of programmable edge infrastructure, and expand the need for security and identity controls around agents. This quarter gave bulls more evidence: mgmt talked about “hundreds of billions” of agentic requests, Workers added 1M developers in a single quarter, large AI customers signed seven-figure deals, and mgmt described AI demand as a tailwind across Act 1, Act 2 and Act 3. Bulls also like that the platform is not just selling into AI labs, but also helping enterprises manage AI crawlers, bot traffic, data access, privacy, and agent execution.

Bulls also argue that the RIF is misunderstood. They frame the ~20% workforce reduction as a structural AI-first re-architecture rather than demand weakness, especially because quota-carrying AE capacity was protected and is expected to accelerate. The strongest version of the bull case is that NET can keep revenue growth around ~28%-30% while expanding operating margins meaningfully, potentially reaching Rule of 50 in CY27. That would make NET scarce in software: a $3B+ revenue business growing near 30%, with a credible path to 20%+ EBIT margins. This quarter’s raised FY26 OM guide, plus commentary about Rule of 40 north of 46% and visibility to north of 50% next year, supports that view.

Bears agree that AI is a real tailwind, but argue the stock already priced in near-perfect execution. The immediate issue is that 1Q was good, but not a blowout relative to elevated expectations: revenue beat by ~3%, the FY26 revenue guide was only raised by the beat, and 2Q guidance implies a deceleration to ~30% y/y. For a stock trading at a premium multiple, that is not enough. Bears also focus on leading indicators: DBNRR declined to 118% from 120%, RPO growth slowed to 36% from 48%, and q/q RPO adds were viewed as light. Even if there are explanations around pool-of-funds and tough comps, bears worry that the acceleration narrative is not showing up cleanly in the numbers yet.

The RIF is another bear concern. A ~20% workforce cut at a ~30% top-line growth company is unusual, and even if mgmt says AE capacity is protected, bears worry about disruption to support, renewals, implementation, product velocity, morale, and customer experience. Gross margin also creates a second-order debate: mgmt says the decline is due to free-to-paid traffic and Workers mix, and that operating margin is the better metric. Bears respond that lower gross margins, elevated network capex, and heavier Workers/inference mix could make the unit economics harder to model, especially if NET must invest more behind AI infrastructure.