TMTB Morning Wrap

Good morning. Already a fun one as futures spiked from -1% to +2% on Trump’s attempt at a TACO:

“The United States and Iran have had productive discussions over the past two days toward fully resolving hostilities in the Middle East. As talks continue this week, I’ve ordered a five-day pause on any military strikes against Iranian energy infrastructure, contingent on progress.”

But early Iran comments show that it takes 2 to TACO in this conflict:

IRAN’S FOREIGN MINISTRY SAYS THERE ARE NO TALKS WITH WASHINGTON AND ACCUSES US PRESIDENT OF BUYING TIME WHILE REGIONAL DE-ESCALATION EFFORTS GO ON.

TASNIM SAYS CITING IRANIAN SOURCE THAT THE STRAIT OF HORMUZ WILL NOT RETURN TO PRE-WAR CONDITIONS AS LONG AS THE ‘PSYCHOLOGICAL WARFARE CONTINUES’MEHR CITING FOREIGN MINISTRY: TRUMP’S REMARKS ARE MEANT TO DECREASE ENERGY PRICES AND GAIN TIME FOR HIS MILITARY PLANS

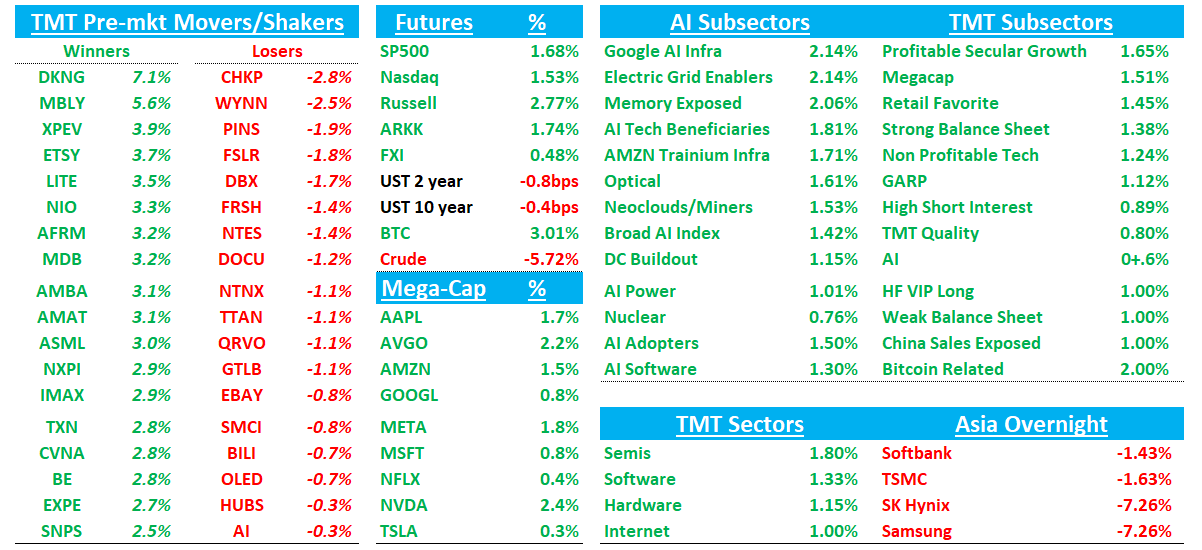

At time of writing futures still holding a +1.7% gain. Oil is down 6% after being double digits after the headlines hit. Yields aren’t moving much. BTC 3%

Asian red overnight: NKY -3.4%, Hang Seng -3.5%, SHCOMP -3.6%, TAIEX -2.4%, KOSPI -6.4%, India -1.8%. HSTECH -3.3%, Semis -4%. Sk Hynix/Samsung -7%.

The wild ride continues.

Lots to get to on the news/research front, so let’s get to it…

MDB: Mizuho Upgrades to Outperform on AI-Driven Growth Acceleration and Margin Upside

Mizuho upgrades MDB to Outperform with a $325 price target, citing improving growth trends and a compelling risk/reward setup following strong FQ4 results. The firm highlights accelerating customer adds (+60% y/y), improving NRR, and a retooled GTM driving momentum, with bottom-up work implying ~$3.07B FY27 revenue (~25% growth) vs. Street at $2.90B. Mizuho adds MongoDB’s evolution into a broader operational data platform positions it to benefit from AI workloads, with Atlas adoption and context-layer relevance supporting durable multi-year growth and margin expansion.

AMZN

Street out in full force today…

AMZN: Wells Fargo Flags Fuel Cost Headwinds, Sees ~$3.3B FY26 Impact

Wells Fargo says rising diesel prices (+43% YTD) could create meaningful near-term cost pressure for AMZN, estimating ~$280M/$880M headwinds in 1Q/2Q26 and ~$3.3B for FY26 (~330bps drag to operating income). The firm notes a 10% move in diesel prices (~$0.50/gal) equates to ~$1.3B annual cost impact, with AMZN lacking hedging exposure. Wells adds while not thesis-changing, fuel inflation likely tempers near-term margin upside.

AMZN: TD Cowen Sees AWS Reacceleration to Mid-30% Growth, Reiterates Buy and $300 PT

TD Cowen says AWS is set to reaccelerate meaningfully with revenue growth rising to ~25–30% in 2026 and ~30%+ into 2027, driven by GenAI demand across chips, models, and applications. The firm highlights improving unit economics with incremental revenue per capex dollar approaching historical levels by 2028, while margins remain stable in the mid-30% range with upside longer term. TD Cowen adds AMZN capex is ramping aggressively (~$266B in ’27), but sees peak intensity in 2026–27 with improving ROI thereafter, reinforcing AMZN as a top pick with a $300 price target.

AMZN: Barclays Raises Estimates on Agentic AI Tailwinds Driving AWS Acceleration

Barclays says AWS growth is set to accelerate meaningfully on agentic AI demand, with revenue growth potentially reaching ~34% in 3Q26 (above street at 25%) and remaining above consensus through 2027. The firm highlights the OpenAI agreement (~$138B spend over 7–8 years) and rising Anthropic momentum as key drivers, supporting backlog expansion and estimate revisions. Barclays adds AWS is well positioned to gain share in the agentic era, with improving visibility on long-term revenue potential and AI-driven workloads underpinning the next leg of growth.