TMTB Morning Wrap

Good morning. Futures +40bps to start the big day as all eyes on Jensen and NVDA post-close. CRM also the other key name reporting today. Bernstein conference also starts today with SNDK at 3:30 est. Agenda Here.

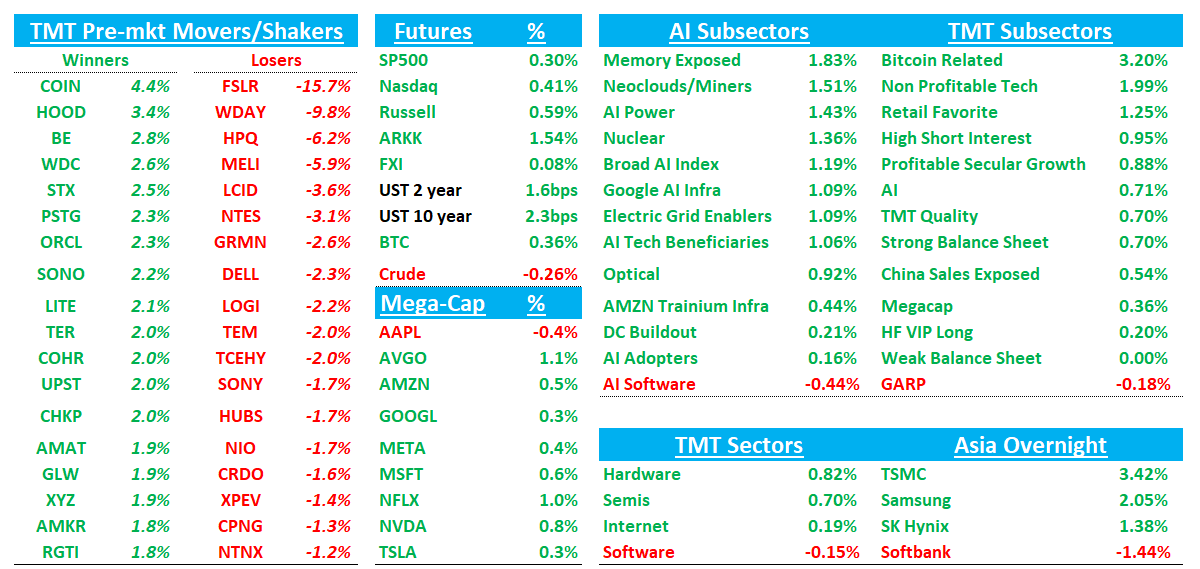

Asia saw green overnight: TPX +0.71%, NKY +2.2%, Hang Seng +0.66%, HSCEI +0.3%, SHCOMP +0.72%, Shenzhen +1.21%, Taiwan TAIEX +2.05%, Korea KOSPI +1.91%. Memory and Semi name particularly outperformed.

BTC +3% finally catching a bid overnight. Yields up 2-4 bps across the curve.

Should be a fun one. Earnings first then the usual. Let’s get to it…

WDAY -9%: Q4 steady/beat on margins, but FY27 guide steps down as AI spend ramps

WDAY put up a mostly in‑line/slightly better Q4 with a notable margin beat, but FY27 subscription growth and margin guidance came in below Street as management highlighted deal elongation and chose to accelerate agentic‑AI investment.

CEO Aneel Bhusri on AI “replacing” HR/ERP (h/t J. Kulina at Wedbush): “You've all heard the narrative out there that HR and ERP will be replaced or relegated to the background by AI. I personally just don't see that happening. Our application domains are really, really hard to build. These are true systems of record that must process transactions with absolute accuracy and speed, enforce complex security models, and comply with statutory and regulatory requirements all over the world. That kind of complexity is very hard to replicate. No amount of vibe coding is going to produce an HR or an ERP system. You can't have probabilistic outcomes in running a payroll. It needs to be 100% accurate and completed 100% of the time"

The #s:

FQ4’26:

Revenue $2.532B, +14.5% y/y (last q 12.6% y/y) vs Street $2.525B, +~14.2%

Subscription revenue $2.360B, +15.7% y/y (last q 14.5% y/y) vs Street $2.356B, +~15.5%

cRPO $8.83B, +15.8% y/y (last q 17.6% y/y) vs Street $8.82B, +~15.6%

FQ1’27 Guidance:

Revenue $2.515B, +12.3% y/y vs Street $2.531B, +~13.0%

Subscription revenue $2.335B, +~13% y/y vs Street $2.352B, +~13.8%

Non‑GAAP operating margin 30.5% vs Street 30.9%

cRPO growth +14.5% to +15.5% y/y vs Street ~+14.8%

FY27 Guidance:

Revenue $10.635–$10.660B, +~11.5% y/y vs Street $10.727B, +~12.3%

Subscription revenue $9.925–$9.950B, +12–13% y/y vs Street $9.993B, +~13.1%

Non‑GAAP operating margin ~30.0% vs Street 31.2%

Free cash flow $3.180B, +15% y/y vs Street $3.246B

Key Takeaways:

Mgmt cited net new large enterprise deals taking longer (Fed/SLED/healthcare and pockets of commercial) and that some deals slipped from Q4 into early Q1, which was incorporated into FY27 guidance. On the callback, the “why” sounded sector/process driven (federal shutdown dynamics, healthcare funding complexity) and AI adding education/decision steps, rather than a blanket pipeline collapse.

Mgmt implicitly pointed to a slower seat‑growth backdrop, while management leaned on installed‑base expansion + AI products to offset.

On AI, Mgmt emphasized 1.7B AI actions in FY26, >$100M of Q4 new ACV from emerging AI products (>100% y/y), and AI ARR >$400M. However, they also stressed the move to consumption/credits (ratable recognition) which can delay revenue visibility relative to product excitement. They outlined a plan to monetize API calls / data access / agent APIs (including third‑party agents) via Flex Credits, explicitly positioning WDAY as a consumption platform “like hyperscalers.”

Bull vs. Bear Debate

Bulls will argue the core franchise remains structurally solid: WDAY is a sticky HR/finance system of record with high retention and a very large installed base, and the quarter again showed that expansion is the primary growth engine. They’ll point to mgmt commentary that AI is already showing up in commercialization (AI involved in ~half of customer‑base transactions; AI‑attached expansions larger on average), and they’ll view the role‑based agent roadmap plus Sana becoming the “front door” as the clearest path in years to raise ARPU/expand wallet share even in a “lower seat growth” environment. On demand, bulls will emphasize management framing that the softer net new dynamic is timing/cycle elongation rather than pipeline deterioration, with some slipped deals already closing early in Q1 and an expectation that 2H improves as organic innovation (agents + data cloud) ramps.

Bulls also like the platform monetization pivot: shifting from a pure seat/FTE model to Flex Credits / consumption pricing (including third‑party agent access, data context, and premium “agent APIs”) is a credible attempt to capture value in an AI world where “intelligence layers” get built around systems of record. The near‑term tradeoff (more GTM and R&D investment) is framed as rational if it prevents disintermediation and expands the total monetizable surface area. In that framing, the FY27 guide is intentionally conservative (and management even hinted at a “guide conservatively, then beat” approach), setting up a potential cadence of better‑than‑guided quarters if macro timing normalizes and early agent adoption translates to measurable consumption and hope re-accel back to high end of 12-15% range.

Bears will focus on the pattern: another year, another forward guide step‑down. Even if Q4 was “fine,” the more relevant stock driver is that FY27 subscription growth and margin guidance came in below Street, and management attributed softness to net new core weakness and elongated cycles across important cohorts (Fed/SLED, healthcare, and parts of commercial). Bears will highlight the RPO shortfall and the decline in average contract duration (renewal mix) as signals that this isn’t just “timing” but instead it’s a business that’s increasingly reliant on renewal/installed‑base activity, with net new harder to land in a choppier macro. They’ll also point to notes calling out non‑recurring tailwinds inside cRPO, implying the headline backlog growth rate may be flattering underlying demand.

On AI, outside of the usual long-term sw seat/disintermediation bear case, bears don’t necessarily dispute the product momentum; they dispute when it hits the P&L and whether it can offset slowing core. A consumption/credits model can be strategically right, but it introduces recognition lag and forecasting complexity (exactly when investors want clean visibility). Meanwhile, the company is explicitly telling you that it will spend more (product + GTM, forward‑deployed engineers, specialized AI talent), which means less operating leverage and makes prior medium‑term margin aspirations harder to believe. Bears will also add execution risk: leadership transitions, sales org changes, and a multi‑quarter “activation” effort imply that even strong tech may take time to become repeatable, scalable revenue.