TMTB Morning Wrap

Good morning. QQQs +75bps helped by Trump’s semiconductor tariff proposal which would exempt companies making US investments, or those who have committed to doing so. So seems like will be pretty easy to be exempt if you have any mfg or investment in the U.S. (AAPL, TSM, NVDA, Samsung, and Hynix specifically called out as exempt so far) and the consensus read-through is this is a much better result than many anticipated and a clearing event.

A not so fun headline for INTC:

TRUMP: CEO OF INTEL IS HIGHLY CONFLICTED AND MUST RESIGN

Lots of earnings — and not much research — to get to so let’s dive straight in.

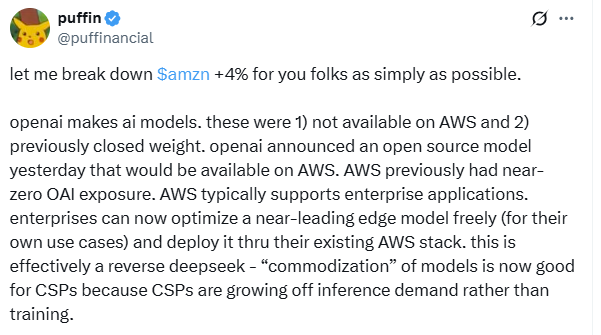

Re: AMZN’s +4% move yesterday, we thought this was an interesting take:

DDOG +6%: Larger than expected rev beat and q3 guide as OAI overhang looms in 2H

Strong numbers as expected by many, but this beat buyside bogeys by an additional 2% and the q3 guide looks good. Main concern on the name is the OAI overhang (hence the early fade) — OAI is likely driving significant upside to revs right now but part of the revs could roll off in 2H if OAI begins to bring some of their revenue in house and I’m sure there will some questions around that on the call although unlikely we get some definitive answer from mgmt. FundamentalBottom had a good note recapping potential scenarios a few days ago and what it could mean for DDOG revs. Without that tricky set up - DDOG would be a no brainer long for us - we have it our sw group of AI/infra beneficiaries. The OAI issue muddies things a bit for us.

Q revs came in at $826M above buyside at $815M at street at $791M. This is 4.5% upside, larger than the ~3% beats of the past two quarters and is 28% y/y growth, an accel from 25% the last two quarters.

DDOG guided Q3 ’25 revenue to $847-$851 million about 4 % above the Street’s $819 million view and bogeys closer to $830M, and should help alleviate some fears of OAI moving off in Q3. For the full year, it now sees revenue of $3.31-$3.32 billion versus Street’s $3.24 billion and EPS of $1.80-$1.83 , about 7 % better than street at$1.70 forecast. This implies only 19% growth in Q4, which bulls will say is conservative while bears will say its conservative bc of OAI headwinds.

APP -1%: So-so results overshadowed by bullish call and set up into 2H self-serve launch

Expectations weren’t high here heading into Q2 given mixed checks and APP noted it has purposely constrained advertiser onboarding “pretty heavily” while it gets the self-service product ready. Q revs came in at $1.26B in line with street. This was only a 4.5% beat vs the 6-9% beats we have seen the last 3 quarters.

However, we thought CEO Adam sounded very bullish on the call (“loads the Q4 bazooka”). Here are a couple key quotes which underscores how excited he is about the full self serve launch in 2H:

“The reality is, like Q4 is going to end up being a fun quarter. You've got the advertiser cohort that we didn't have last Q4 that was growing in the quarter to the point where we reported huge numbers and then had huge numbers in Q1, but we're going to have those advertisers primed and ready to go for the full Q4”

“We're going to have those advertisers inviting their friends onto our platform in Q4, and we're going to be opening up international all at the same time. So there's going to be a lot of fun moment, moments for us and our customers in this e-commerce or web-based category that'll set sort of a new baseline for that business. And then obviously, then we will go through hopefully another inflection when we really truly open up the platform and try to get into a state where we're more stable long-term”

Yup - sounds pretty good! Importantly, it sounds like they will open self serve on a referral basis and internationally in Oct. and full GA in 1H26. On the call back, APP said it does not expect all customers to use self serve and anticipates larger customers will likely still need to be onboarded manually at first APP believes if it can make its platform work for smaller companies, it should translate to success for bigger ones as well.

Bull vs. Bear Narrative

Bulls argue that AppLovin’s 77% top-line surge and 81% margin prove the Axon engine is still compounding returns while requiring minimal incremental opex. Confirmation of the 10 / 1 referral launch, plus a commitment to fully open the portal in 1H26, reinforces the view that e-commerce can unlock a new profit pool. They highlight cash-generation (61 % FCF margin post-divestiture) and a clear 20-30% Y/Y growth baseline in gaming even before non-gaming ramps.

Bears counter that Q3 guidance is only a mid-single-digit sequential lift, reflecting flat e-commerce revenue and a slower-than-hoped self-serve rollout. They question whether gaming can sustain hyper-growth once easy comps fade, and whether the second Axon model for web commerce can ever match the gaming model’s precision. Bear will say co. has been crushing numbers but now can barely meet street estimates. Some point to rising competitive noise (Unity, Meta) and potential privacy-regulation shocks that could dent targeting efficacy. Finally, sc=keptics note that margins are already lofty, leaving limited room for upside if revenue momentum stalls.

Our view: