TMTB Morning Wrap

Good morning. Futures -20bps with oil higher by 5% as investors continue to digest durability of the ceasefire in Iran ahead of talks between two sides Saturday morning in Pakistan.

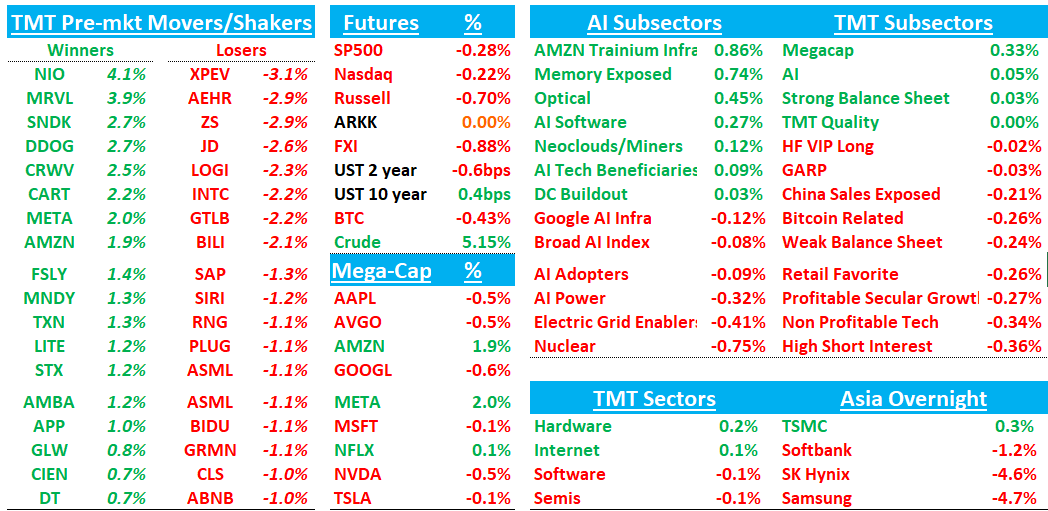

Asia slightly down overnight: TPX -0.9%, NKY -0.73%, Hang Seng -0.54%, HSCEI -0.75%, SHCOMP -0.72%, Shenzhen -0.61%, Taiwan TAIEX +0.29%, Korea KOSPI -1.61%. Samsung/SKHynix -5%. Yields aren’t budging much. BTC -40bps.

Lots of good stuff to get to this morning so let’s get straight to it…

CRWV/META: CoreWeave Expands AI Cloud Infrastructure Deal With Meta for $21 Billion

According to WSJ, CoreWeave expanded its long-term agreement with Meta Platforms to provide AI cloud infrastructure capacity through December 2032 for approximately $21 billion, building on their previous $14.2 billion deal from fall. The expanded agreement will deploy dedicated capacity across multiple locations, including initial deployments of Nvidia's Vera Rubin platform, to support Meta's AI development and deployment. CoreWeave shares rose 7.8% in premarket trading on the announcement.

META: Morgan Stanley Says Muse Spark Is First Step in Re-Rating, Sees ~25% Upside

Other sell side out positively similarly on Muse Spark. We had some thoughts in our EOD wrap yesterday

Morgan Stanley flags META’s debut of Muse Spark — its first homegrown model since forming Meta Superintelligence Labs — as a meaningful catalyst, noting benchmark gaps vs. frontier peers are narrower than feared and what matters most is META’s ability to productize 1P model capabilities across its Family of Apps. The firm highlights Muse Spark’s built-in shopping assistant as setting the stage for agentic commerce, with “trust” identified as a key gating factor for adoption where META’s user/influencer content corpus could be a differentiator. An API monetization bull case — Muse Spark is closed-source, currently offered to select partners — adds optionality not priced at 17x ‘27 EPS. META remains MS’s top pick with ~25% upside.

SNDK: Bernstein Raises PT to $1,250; NAND Pricing Driving Material EPS Upside

Bernstein raises PT on SanDisk to $1,250 (blue-sky $3,000), citing stronger-than-expected NAND pricing driving significant estimate upside. The firm sees TurboQuant fears as overdone, with efficiency gains likely increasing demand (Jevons effect). Bernstein lifts FY27 EPS to $144/$224 (base/bull), with upside driven by ASP strength (+~40% QoQ into FQ4). Net, the analyst sees the stock undervaluing cycle durability and earnings power, with asymmetric upside.

$3k! And I thought I was bullish….Cantor also out raising PT to $1k in their preview. $1k number going to begin to act like a magnet. Also heard some chatter around an MS note saying YMTC allocating more capacity to DRAM vs. NAND, but didn’t see it.

AMZN out with shareholder letter:

Our annual revenue run rate for our chips business (inclusive of Graviton, Trainium, and Nitro—our EC2 NIC) is now over $20 billion, and growing triple digit percentages YoY. To dimensionalize this versus other chips companies, that run rate is somewhat understated by our currently only monetizing our chips through EC2. If our chips business was a stand-alone business, and sold chips produced this year to AWS and other third parties (as other leading chips companies do), our annual run rate would be ~$50 billion. There’s so much demand for our chips that it’s quite possible we’ll sell racks of them to third parties in the future.