TMTB Morning Wrap

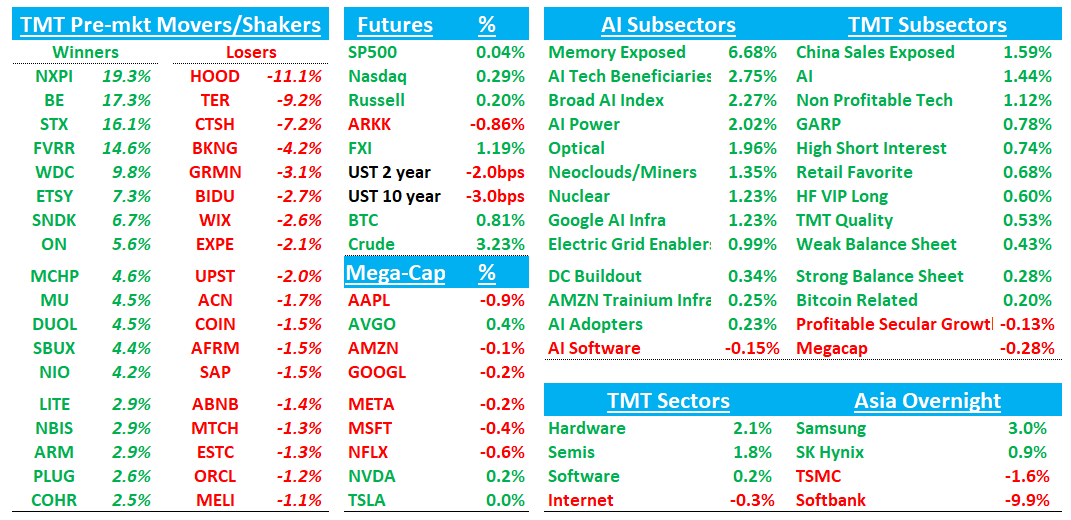

Good morning. Futures +30bps. Yields ticking down 2-3bps. Oil +3%. Asia generally green: Hang Seng +1.68%, HSCEI +1.86%, SHCOMP +0.71%, Shenzhen +1.66%, Taiwan TAIEX -0.55%, Korea KOSPI +0.75%. Softbank -10% / Samsung +3%

Some big moves in semi land following earnings with STX +16%, NXPI +19%, BE +20%. STX helping WDC +10% and the memory names ahead of SNDK earnings (SNDK +7%; MU +5%).

Big night tonight with META, MSFT, AMZN, GOOGL on the docket…should be a fun time in TMTB Slack.

We’ll touch on earnings first then get to the usual…

EARNINGS

STX +16%: Big and broad beat/raise, as narrative continues to shift further toward “structural AI storage growth + pricing power + HAMR margin expansion.” GMs the standout

Not much to pick at here. A stellar print by STX and mgmt sounded bullish as usual on the call. Buyside numbers here shifting to the bull case which is Low to mid 60s GMs and close to $45 in EPS for CY27. Bulls will say high teens/20x+ multiple on that given higher for longer structural growth, better pricing/margin, and better industry dynamics (two players with rationale supply)

The #s:

FQ3 revenue was $3.112B, +44.1% y/y (last q +21.5% y/y) vs Street $2.956B, +~36.9% y/y, with non-GAAP EPS $4.10 vs Street $3.50-$3.51 and non-GAAP GM 47.0% vs Street ~44.3-44.6%.

FQ4 guide was revenue $3.45B, +~41% y/y vs Street ~$3.15-$3.16B, +~29% y/y, with EPS $5.00 vs Street ~$3.96-$3.99 and low-40s OM vs Street ~36%. Implied GMs 50% vs street in high 40s.

Annual revenue growth target raised to minimum 20%, nearline capacity nearly allocated through CY27, build-to-order contracts through FY27, Mozaic 4+ ramping, and FCF approaching $1B.

Key takeaways:

Mgmt highlighted $/TB or $/EB moving higher, noting the largest HDD price increase per EB in over a decade. The durability of the pricing story rests on nearline capacity being nearly allocated through CY27, build-to-order deals through FY27, and conversations extending into CY28. Mgmt emphasized no change in pricing strategy, but demand continues to exceed supply.

Mozaic 4+ is qualified at two of the world’s largest CSPs, began revenue shipments in late March, and is expected to represent the majority of HAMR exabytes exiting CY26. Mgmt said qualification timelines were in line with PMR, which is important because it reduces concern that HAMR adoption will be slow, costly, or unreliable. Mozaic 5 at 50TB remains targeted for qualification shipments in late CY27

Mgmt reiterated STX is not adding unit capacity, and exabyte growth is being driven by areal density, not unit growth. That helps support the “rational duopoly / constrained supply” thesis.

Data center revenue was $2.5B, +55% y/y and +12% q/q vs Street around $2.37B, and data center was 80% of revenue. Mgmt cited AI inference, agentic AI, video, physical AI, sovereign cloud, neocloud, and enterprise tiered architectures as drivers.

The callback noted mechanical parts were sufficient, memory was short and more expensive, but HDDs require limited memory and STX expects internal yield/cost actions to offset

On the callback, mgmt also remained confident in pricing improvement for at least the next four quarters, with build-to-order contracts in place through FY27, nearline EB supply allocated through CY27, and planning discussions extending into CY28. Mozaic 4+ volumes were still small in March but expected to ramp in June and more in 2H FY26, with two qualified cloud customers consuming most of the ramp near term.

OpEx dollars are expected to be flattish for the next 3-4 quarters, while mechanical supply is sufficient and memory tightness is manageable given low memory content per HDD.

FCF deployment remains debt reduction first, especially remaining converts, followed by a greater focus on buybacks, with mgmt reiterating a 75% FCF return framework.

Bull vs. Bear Debate

Bulls see STX as undergoing a structural business-model upgrade, not just a cyclical HDD upturn. The core argument is that AI is turning data into a strategic asset, which creates more demand for low-cost, power-efficient mass capacity storage across training, inference, agentic workflows, video, autonomous systems, sovereign cloud, and enterprise tiered architectures. This quarter strengthened that argument because mgmt raised the annual revenue growth target to at least 20%, reported the 10th consecutive quarter of cloud revenue growth, and said nearline capacity is nearly allocated through CY27, with planning already reaching into CY28. Bulls also like that demand is not being chased through unit additions, which supports supply discipline and pricing power.

Bulls also see HAMR as the unlock for both revenue and margin. Mozaic 4+ gives STX up to 44TB drives with >30% more capacity versus first-gen Mozaic using largely the same number of disks/heads and minimal BOM change. If STX can add exabytes through density rather than units, the company gets more output, better customer TCO, and falling cost/TB without flooding the market. This quarter de-risked HAMR because two of the largest CSPs are qualified on Mozaic 4+, qualification timelines matched PMR, and Mozaic 4+ should become the majority of HAMR exabytes exiting CY26. Bulls will point to FQ3 GM at 47%, FQ4 implied GM around 50% as proof that the margin bridge is ahead of plan.