TMTB Morning Wrap

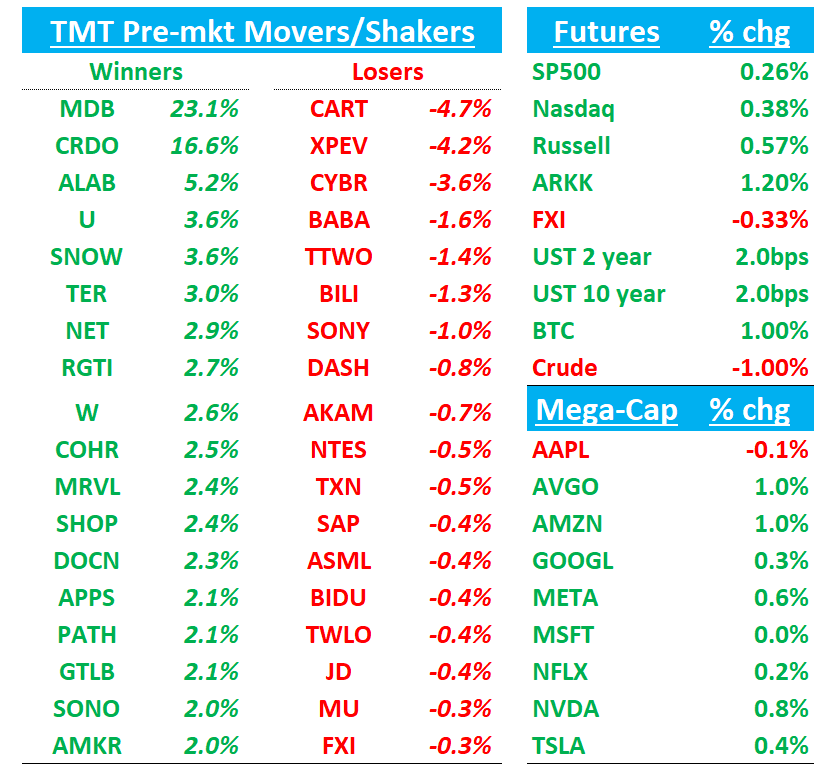

Futures +35bps. BTC +1% bouncing back a bit after yesterday’s declines. A couple big prints overnight with MDB +23% and CRDO +17% and both stocks hitting new highs in the pre. Asia stocks mixed: : TPX +0.08%, NKY flat, Hang Seng +0.24%, HSCEI +0.11%, SHCOMP -0.42%, Shenzhen -0.67%, Taiwan TAIEX +0.81%, Korea KOSPI +1.9%

UBS Conference Day 2 - agenda here … NVDA CFO at 11:35am est.

AMZN AWS CEO Keynote at 11am est. at Re:invent

We’ll hit up MDB/CRDO Earnings first then onto the usual…Lots to get to so let’s get to it…

EARNINGS

MDB +22% delivered a 3rd straight big beat-and-raise quarter with Atlas re-accelerating to ~30% growth and margins far above expectations

The #s / Key Takeaways

F3Q26 revenue was $628.3M, +19% y/y (last q +24% y/y) vs Street ~$595M (+~12% y/y) and non‑GAAP EPS was $1.32 vs Street ~$0.80, with non‑GAAP operating margin ~19.6% vs 12.1% consensus.

Atlas grew ~30% y/y (75% of revenue) vs mid‑20s Street and roughly in line with bogeys, while non‑Atlas ARR grew ~8% y/y, helping total NRR tick up to 120% vs 119% last q.

Q4 Revenue guide of $665–670M (+21–22% y/y) and $1.44–1.48 EPS is well above Street (~$626M / $0.94), and FY26 guidance moves to 21–22% growth and ~18% OM with >100% FCF conversion.

Atlas strength is broad‑based and driven by large customers. Atlas now represents ~75% of revenue; management highlighted consistent consumption patterns vs last year, with strength in large U.S. customers and EMEA, and growth coming from both new workloads and expansion of existing ones.

Non‑Atlas flipped from headwind to tailwind. Non‑Atlas ARR grew ~8% y/y and contributed meaningfully to the beat (roughly two‑thirds of non‑Atlas upside tied to multi‑year licenses), vs prior expectations for a decline. Management now expects upper‑single‑digit non‑Atlas growth in Q4 and low/mid‑single‑digit growth in FY27, easing concerns that term licenses would structurally drag growth.

Net ARR expansion returned to 120% (from 119%), >$100k ARR customers grew ~16% y/y to 2,694, and total customers grew ~19% y/y to ~62.5k, with strong self‑serve adds but a deliberate move up‑market causing direct‑sales customer count to dip ~5% y/y to ~7k.

Management repeatedly emphasized that current outperformance is driven by core workloads, with AI revenue still immaterial near term. But they highlighted a “structural advantage” for Mongo’s document model plus integrated search + vector + embeddings, top rankings on industry AI benchmarks, and early wins with AI‑native startups as well as enterprises building AI agents and recommendation systems.

New CEO CJ Desai framed MongoDB as a potential “generational modern data platform” and is prioritizing expansion in the Fortune 500/Global 2000 and public sector. MDB is consciously shifting GTM and PLG toward larger strategic accounts; fewer self‑serve customers are being pushed to the direct‑sales channel, but large‑deal activity and strategic expansions (e.g., a major global insurer modernizing on Atlas) are improving mix and durability.

Bull vs. Bear Debate

Bulls see this quarter as confirmation that MongoDB is emerging as a durable 20%+ grower with an increasingly attractive FCF profile. The core thesis is that MDB has become the de‑facto standard for modern, document‑oriented operational data, with Atlas now 75% of revenue and re‑accelerating to ~30% y/y growth even before meaningful AI monetization. The Atlas comp gets easier again next quarter which means we likely see y/y growth with a 3-handle for the first time since ‘25 Q1. The rebound in NRR to 120%, broad‑based demand across industries/regions, and improved non‑Atlas trajectory suggest that the consumption wobble of 2023–early 2024 is behind the company and that growth is underpinned by large, mission‑critical workloads rather than transient experimentation. On AI, bulls argue that MDB is one of the best‑positioned “data layer” plays: the document model, integrated search/vector/embeddings, and cloud‑agnostic platform are all well‑suited for RAG and agentic AI workloads. Management and analysts highlight early traction with AI‑native startups and enterprises replacing legacy search or Postgres‑based stacks with Atlas + vector search, and the company’s top rankings on AI retrieval/embedding benchmarks support the narrative that Mongo is technically differentiated.

Bears focus first on deceleration and quality of growth. While 19% y/y growth and a 22% Q4 guide look strong, they are down from mid‑20s+ levels in prior years, and some of the upside this year has been driven by non‑Atlas multi‑year renewals and EA timing. Two‑thirds of non‑Atlas upside in Q3 came from multi‑year licenses, and some of the Q4 uplift reflects revenue‑recognition dynamics around EA deals rather than purely run‑rate growth. Second, skeptics argue that the AI narrative is ahead of monetization. Management itself says AI revenue is still immaterial, and most of the current outperformance is driven by core modernization workloads. Bears worry that AI‑native startups are inherently more volatile customers and that large‑enterprise AI projects are still in pilot stages; if AI ramp takes longer, the premium “AI platform” multiple may not be justified. In bears’ view, MDB is still primarily “just” a database company competing in a brutally competitive, maturing market. Lastly, competition is another central bear point. MDB faces well‑funded hyperscalers (AWS, Azure, GCP) pushing managed document/NoSQL services, as well as entrenched relational vendors and the improving PostgreSQL ecosystem. Some bears see MDB’s move up‑market and emphasis on multi‑year deals as partly a response to this competitive pressure. They also flag that Atlas’ growing share of revenue structurally pressures gross margins and may cap long‑term profitability if price competition intensifies, especially as hyperscalers bundle databases into broader cloud deals.

CRDO +18% posted a blowout F2Q26 beat with an even bigger F3Q26 and FY26 raise, reinforcing the “AI connectivity pure‑play” narrative

The #s / Key Takeaways

Q2 Revenue was $268M, +272% y/y and +20% q/q, vs Street $235M (+~226% y/y), with non‑GAAP EPS $0.67 vs Street $0.49 as AEC demand at hyperscalers stayed extremely strong and margins surprised to the upside.

F3Q26 revenue is guided to $335–345M (midpoint $340M), +152% y/y and +27% q/q vs Street ~$247.5M (+~83% y/y), with implied non‑GAAP EPS around $0.77 vs Street $0.51 and OM ~44% vs 40.5% Street.

For FY26, management now expects >170% y/y revenue growth, translating to ~ $1.18–1.19B (+~172% y/y) and ~45% non‑GAAP net margin, vs Street previously at ~$0.97B (+~126% y/y) and ~41% net margin. Management also reiterated an outlook for mid‑single‑digit sequential growth through FY27, effectively underwriting ~30%+ y/y growth even off the raised FY26 base.

Management said they expect to be talking about wafer foundry capacity constraints at advanced nodes more frequently as overall AI demand ramps, and suggested the market could become “self‑regulated” by advanced‑node capacity. They argued Credo’s “N‑1” process strategy (12nm “workhorse” vs 3/5nm), small die sizes, and the critical nature of connectivity to GPU shipments should give them a relative advantage in securing foundry capacity

AEC revenue grew “healthy double digits” q/q and is now displacing optics up to 7m. Four hyperscalers each contributed >10% of revenue, with the largest at 42%, second at 24%, third at 16%, and fourth at 11%; a fifth hyperscaler began contributing revenue and is expected to ramp over time. Customer forecasts have “strengthened across the board” over the last several quarters.

Management highlighted three new multi‑billion‑dollar pillars beyond AEC and ICs:

• ZeroFlap Optics – optical modules using a customized DSP plus telemetry (“pilot”) software to deliver AEC‑class reliability; in live DC trials with a lead hyperscaler, with another U.S. hyperscaler sampling later this fiscal year; initial revenue expected in FY27.

• Active LED Cables (ALCs) – microLED‑based pluggable optics delivering AEC‑like power/reliability but up to 30m reach, targeting “row‑scale” networks; sampling in FY27, revenue in FY28; ALC TAM expected to be more than double AEC TAM.

• OmniConnect gearboxes / Weaver – new gearboxes addressing the “memory wall,” enabling up to 30x more memory capacity and 8x bandwidth vs on‑package HBM by bridging 112G VSR SerDes to DDR. Initial revenue expected FY28.