TMTB Morning Wrap

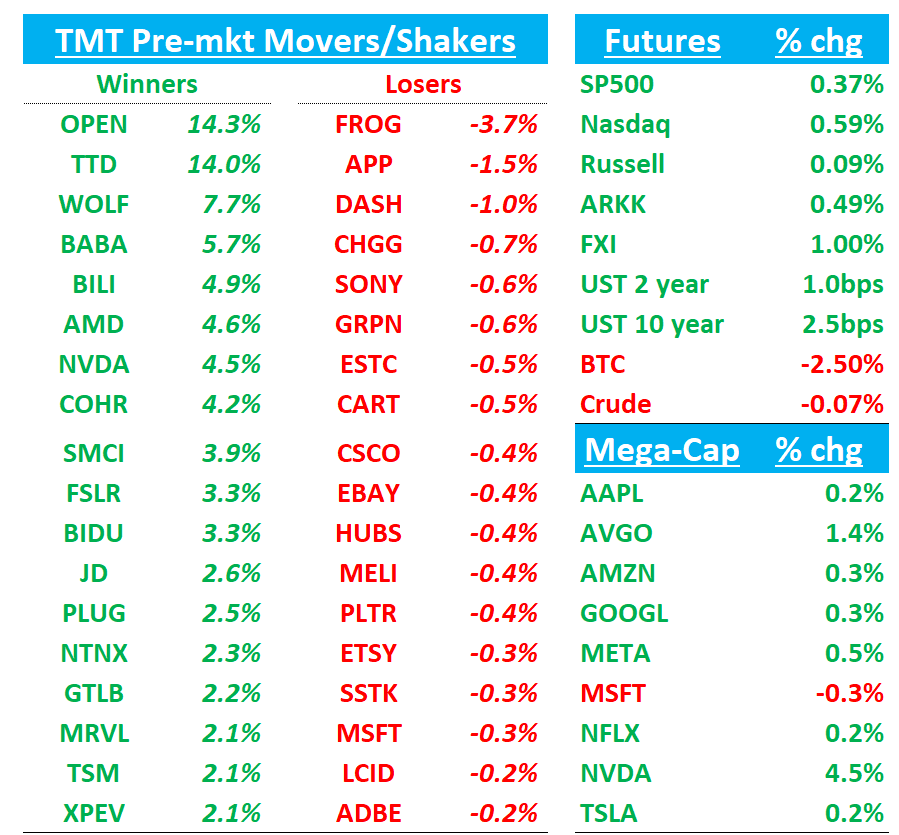

Futures +55bps higher to start the day as the big story in Tech this morning is that U.S. gov’t is now lifting NVDA’s H20 Chinese export restrictions. Here’s Bloomberg:

US government officials told Nvidia they would green-light export licenses for the H20 artificial intelligence accelerator, the company said in a blog post on Monday — a move that may add billions to Nvidia’s revenue this year, restoring its ability to fulfill orders it had written off as lost due to government restrictions. Nvidia designed the less-advanced H20 chip to comply with earlier China trade curbs from Washington, which Trump’s team tightened in April to block H20 sales to the Asian country without a US permit.

Bessent: NVDA Chip decision part of ‘Mosaic’ of China Talks (makes sense - rare earth access for GPU access)

Reuters: Chinese firms rush to buy Nvidia AI chips as sales set to resume

Most on sell-side had written off any H20 revs ($4.5B write down NVDA took in May + additional $15B impact for the year - Bernstein says every $10B in recovered revs adds 25c in additional EPS for the year), so street/buyside numbers will be going up by ~10%+ on the news. NVDA +4.5% / AMD +4% (will ship Mi308 chips to China - they guided to $1.5B impact) to start early — China related names like BABA +6%, GDS/VNET +12% benefitting as well, and TSM/Taiwan names should be helped as well as China/US tensions ease. Rest of semi supply chain also up and the likely read is this lowers risk of sectoral 232 tariffs.

Trump also out with some more dovish talk re: Europe Tariffs - Bloomberg…BTC -2.5%

Yields slightly up to start the day as all eyes now on CPI which hits at 8:30am…

Let’s get to it…

DASH: Jefferies Downgrades to Hold, PT Raised to $250 as Growth Appears Fully Priced

Jefferies downgraded DoorDash to Hold from Buy despite raising its price target to $250 (from $235), citing limited further upside after a 45% YTD rally and valuation at a 120% premium to the Internet peer group. The firm acknowledges DASH’s strong execution and expects EBITDA to double over the next two years, but sees recent affordability initiatives (like DashPass) capping further margin expansion. While advertising and reduced losses in New Verticals could drive ~40% of EBITDA growth, take rate outlook remains murky following the weakest Q1 increase since the pandemic. Jefferies still sees DASH delivering a top-tier 36% 3-year EBITDA CAGR through 2027, tied for 3rd best in their coverage, but believes much of that strength is already priced in.

Citizens and Loop out +ve on DASH (see below)

TTD will be added to the S&P 500 before the open on Friday, July 18, replacing ANSS, which is being acquired by SNPS …watch APP which was up yesterday on hopes of inclusion

TTD: BMO Reiterates Outperform, $115 PT; Sees Amazon DSP Concerns as Overblown

BMO Capital Markets reaffirmed its Outperform rating and $115 price target on The Trade Desk, dismissing concerns that Amazon DSP is taking meaningful share. The firm sees a multi-winner environment in the $1T digital ad market and continues to view TTD as a long-term beneficiary. While acknowledging that Kokai’s learning curve may have contributed to TTD’s Q4 2024 miss, BMO believes the platform represents a major improvement in the ad-buying experience and should unlock more spend over time. Estimates for 2H25 were adjusted to reflect a more gradual Kokai ramp and to better align with consensus expectations.

PINS: TD Cowen Raises PT to $43 on Strong Q2 Ad Trends and Performance+ Momentum

TD Cowen reiterated its Buy on Pinterest and lifted its price target from $40 to $43, citing solid Q2 advertising checks and accelerating traction with the Performance+ ad suite. The firm now sees Q2 revenue growing 14.6% y/y to $977.9M, right in line with the high end of management’s guide, with adjusted EBITDA of $233.6M (+24% y/y). Cowen’s proprietary ad channel data and agency checks highlight robust ramp in spend and impressions, driven by Creative and Automated Bidding tools and improved monetization. PINS saw a 66% y/y jump in managed ad spend in Q2 from one major partner, up from +32% the prior quarter. Cowen sees a multi-year growth runway supported by adoption of new tools and improving ROI for advertisers, and views the stock as attractively valued at 13x EV/EBITDA on FY26 numbers.

META: BofA Raises PT to $775 on AI Ad Tailwinds Despite Higher R&D Drag on EPS

BofA reiterated its Buy on Meta Platforms and raised its price target to $775 from $765, reflecting stronger AI-driven ad trends and higher revenue forecasts, though partially offset by elevated R&D investment. The firm notes CEO comments on Threads regarding multi-gigawatt data center builds suggest long-term AI infrastructure confidence, but also set expectations for rising capex and opex. BofA lifted its 2026 revenue estimate by 1% to $217B, but trimmed EPS to $29.16 (vs. Street’s $28.40) on $6B+ in AI-related R&D. For 2025, revenue is now seen at $190B with EPS of $26.83. BofA continues to see Meta as the best-positioned large-cap internet stock to benefit from AI-enabled ad product innovation and improving monetization. Shares now trade at 25x 2026 EPS, and BofA sees room for multiple expansion as the Street prices in AI returns.