TMTB Morning Wrap

If you are still having trouble with joining TMTB Slack, please e-mail me at Slack@tmtbreakout.com. If you’ve already e-mailed me, I will get back to you this morning. Thanks for your patience.

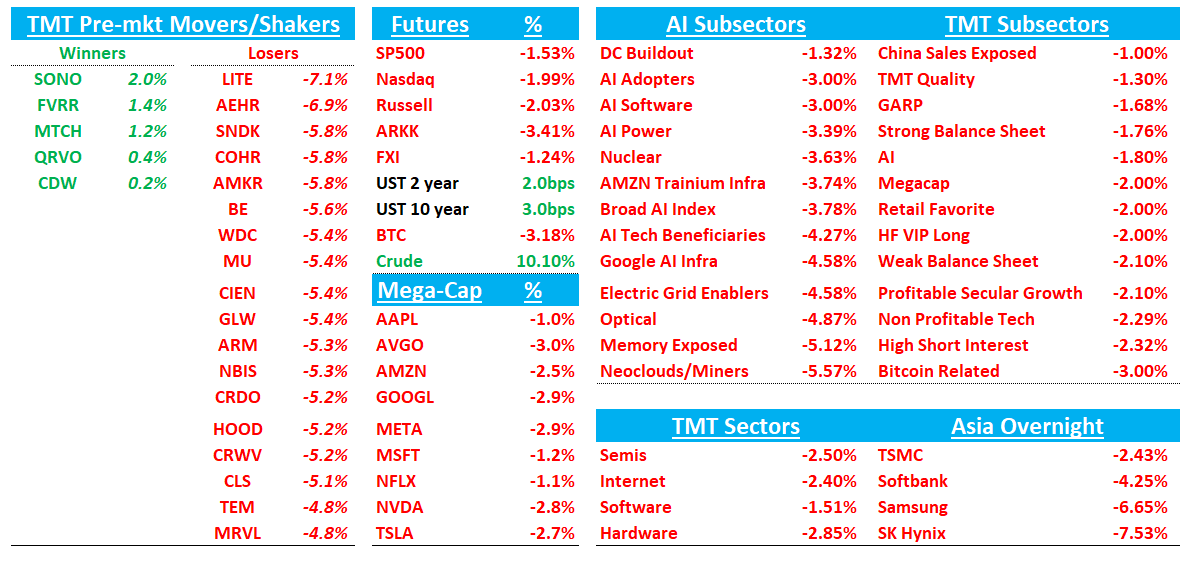

Good morning. Futures -2% and began their descent during Trump’s speech last night. Oil +10%. We framed it as: the speech didn’t have much new, which means it was negative “rate of change” (can you tell we trade tech stocks?). The direction of travel — at least from a perception standpoint — was de-escalatory all week, but this speech wasn’t that at all and opened up more questions than existed about path going forward while at the same time Trump failed to “pump the market.” No mention of boots on the ground (is that a typical Trump non-denial which = might happen?). We got the 5-7% rally this week on the perception of a walk away happening increasing. Now that’s over and going into a long weekend, investors rather not be grossed up on a situation that skews negative. Back to playing defense. Great thread here in TMTB Slack last night which was extremely helpful real-time in framing and reading the tea leaves of the speech, especially in a situation like this which continues to be extremely fluid. Thanks to all those who continue to share their views.

BTC -3%. Yields ticking up 2-4 bps across the curve. Asia lower across the board: Korea -4.5%; Japan -2.5%; HK -70bps.

Early action is opposite of yesterdays with leading AI names leading the way lower: LITE -&%, SNDK -6%; MU -5%. Large cap internet also off with AMZN -3%; GOOGL -3%; META -3%

NOW: Stifel Cuts PT to $135; SI Checks Soft, Fed Business Tracking Below Plan

Stifel’s channel checks down-ticked q/q as SIs flagged a slower-than-usual 1Q with larger deals elongating sales cycles and greater potential for push-outs. More concerning, government data suggests the US Fed business declined meaningfully YoY against a strong +30% comp. The firm expects only ~50bps of 1Q cRPO upside and organic cRPO growth of ~19.5% after stripping out ~100bps of Moveworks contribution. PT goes to $135 on concerns around AI tools (consumption-based revenue) driving potential GM compression.

GPUs: Semianalysis positive on Rental Pricing saying “On-Demand GPU rental capacity is sold out across all GPU types – those that have locked up on-demand instances are not willing to relinquish this capacity back into the pool despite recent price hikes.”

{kind=link}