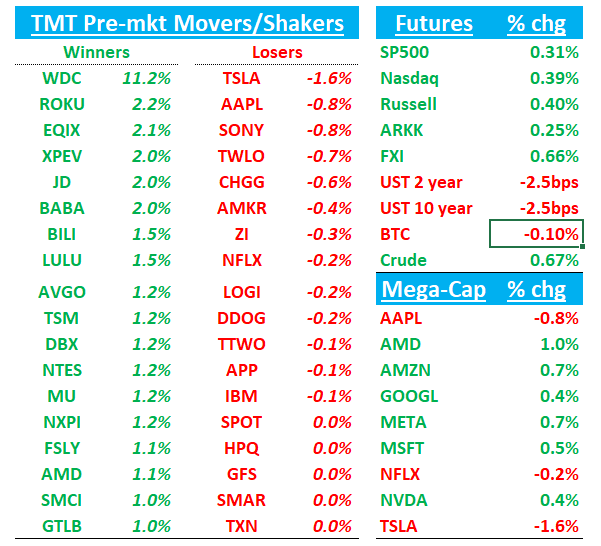

Good morning. QQQs +38bps as yields ticking slightly lower this morning; China +70bps; BTC flat

Key news this morning: WDC +13% with a nice beat; AAPL dg at KEYB; OpenAI to launch Orion model in Dec. Let’s get straight to it…

WDC: Guidance better than feared as investors await early CY25 split

Key # was the $1.90 guide ($1.75 - $2.05) - although lower than street at $1.95 - is better than most bogeys I heard going in (anywhere from $1.60 to $1.85) as most investors were feeling skittish around NAND pricing. Seems like a redux of MU’s print last month when co crushed #s despite weaker checks going in.

In terms of the q, key # was GM 38.5% vs street at 37.9% with significantly better incremental NAND margins. In terms of the spin, WDC confirmed its likely an early CY25 event (most likely January). WDC guided 15-20% FY25 bits which is up from the 10% they mentioned on the call last q.

Other key points: 1) Nearline HDD demand remains strong at 141EB, up 14% q/q as HDD ASP flattish q/q, 2) AI demand strong with enterprise SSD and Ultra SMR demand, 3) NAND CAPEX potentially up y/y in C25E post very low C24 CAPEX, with return to consumer/client demand and node transitions

Some Key snippets from analysts:

JPMorgan

Western Digital reported solid results and forecast that reflect “strong cloud/AI demand”

“Better-than-feared Dec-Qtr guidance reflects sustained shipment strength in both Flash/HDD on strong cloud/AI demand”

Barclays

NAND flash memory segment “continues to not be as bad as many have expected”

“From here, the focus will be on the upcoming split, which sounds to be pushed out slightly to early 2025, and should be a value unlock”

TD Cowen

The company’s results were “in line with expectations amid NAND correction fears”

For Western Digital, strength in hard disk drive business sustaining and flash memory holding up “is all that matters now”

Evercore ISI

The flash memory market is holding up “better than feared”

“Investors will continue to debate the sustainability of current results, but the in-line revenue guide for the Dec-qtr should alleviate concerns about a near-term downturn in the flash market.”

Morgan Stanley

Considering the "nervous NAND market," Western Digital "did well," with like-for-like pricing up in September and implied guidance for modest declines in December, with bits up mid-single digits and NAND revenues up slightly

“Optimistic" about NAND improving next year, but adds that "even if it doesn't, the NAND asset is mispriced" and post the "solid numbers," the focus should shift to the separation.

$WDC GUIDANCE: Q2

- Guides revenue $4.20B to $4.40B, EST $4.35B

- Guides ADJ EPS $1.75 to $2.05, EST $1.95

- Guides ADJ gross margin 37% to 39%, EST 38.5%

- Guides operating expenses $835M to $855M, EST $843.4M

RESULTS: Q1

- ADJ EPS $1.78 vs. loss/shr $1.76 y/y, EST $1.72

- Net revenue $4.10B, +49% y/y, EST $4.13B

- ADJ gross margin 38.5% vs. 4.1% y/y, EST 37.9%

- Operating expenses $809M, +16% y/y, EST $829.7M

- Inventory $3.38B, -3.2% y/y, EST $3.35B

- Negative free cash flow $14M, -97% y/y, EST positive $608M

AAPL: KEYB downgrades to sell from Hold and $200PT

KEYB’s says their consumer survey disproves one major bull case: the iPhone SE is “not purely additive to iPhone sales.” KEYB also cites data points surrounding U.S. iPhone upgrades: 3% in Q3, down 9% y/y for VZ, T-Mobile and T. KEYB notes that expectations call for Apple's highest growth in three years and a major inflection in all geographies and products, which has rarely occurred throughout its history and with AAPL trading at 23x their 25 EBITDA #s vs 20x average, they think AAPL is expensive given everything mentioned above.

OpenAI: Plans to release its next big AI model - Orion - by December - TheVerge

3P Roundup:

Keep reading with a 7-day free trial

Subscribe to TMT Breakout to keep reading this post and get 7 days of free access to the full post archives.