TMTB Morning Wrap

Good morning. QQQs +15bps to start the week. Oil +3% as no deal yet on the Iran front; Trump said the US would begin guiding neutral ships through the SOH strting today in an effort known as “Project Freedom.”

Lots of Tech earnings on the docket this week (we’ll have some bogeys out tomorrow morning as we finalize them today). We also get NOW, IBM and TEAM analyst days this week.

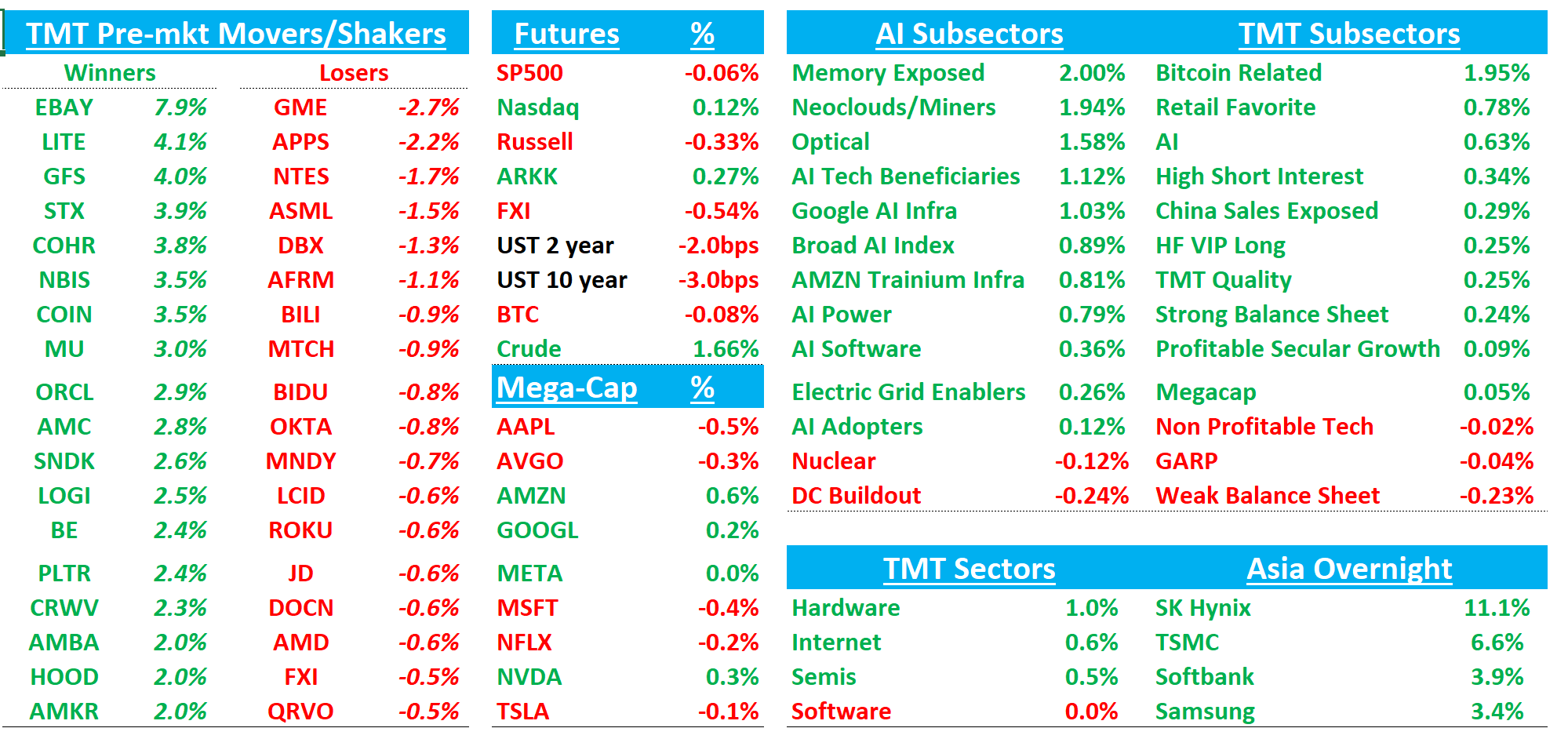

Asia generally higher with HK +1.25 (HK Tech +2%), Taiwan +4% (TSMC +7%), and Korea +5% led by SK Hynix +11% / Samsung +4%. Memory names following the latter higher SNDK/MU/STX +3-4% early.

EBAY +8% leading the way higher after an unexpected $56B takeout bid from GME

Lots to get to, so let’s get to it…

AMD: HSBC downgrades to Hold on capacity constraints; 2026 upside capped despite strong demand.

HSBC (Blayne Curtis) takes a more cautious stance, arguing that while server CPU and AI demand remains strong, supply—particularly foundry capacity at advanced nodes—will be the binding constraint through 2026, limiting upside vs. elevated expectations. The firm expects 1Q26/2Q26 results largely in-line with consensus (e.g., 2Q revs ~$10.5B) and sees limited potential for upside surprises, cutting its 2026 AI GPU revenue estimate (to ~$14.6B from ~$18.5B) on MI455 ramp uncertainty. Server CPU growth remains healthy but capped by supply, with revised 2026 estimates (~$11.8B, +32% y/y) still materially below consensus (~$13.3B), reflecting constrained unit upside despite potential ASP strength. HSBC believes the setup improves into 2027 as capacity expands (2nm/3nm), but near-term risk/reward is less compelling given recent stock momentum, driving a downgrade to Hold and a modest PT increase to $340.