TMTB Morning Wrap

Good morning. Futures -40bps as PCE came in roughly in line. Yields ticking up slightly. BTC -1%.

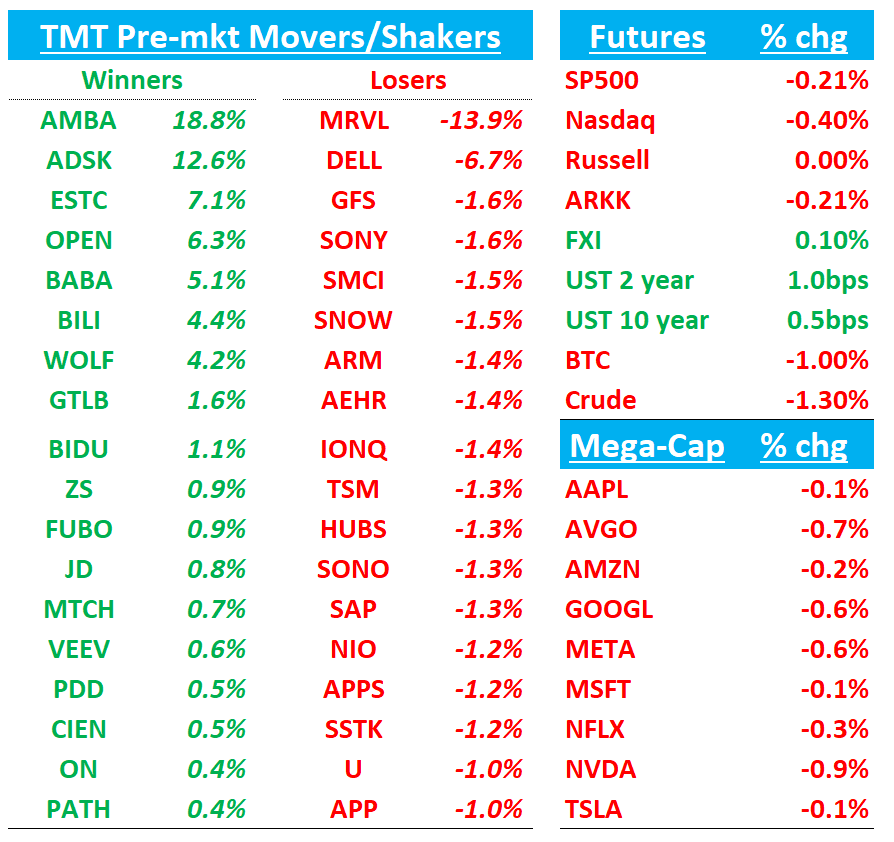

Lots to get to so let’s get straight to it…We’ll cover Earnings first (BABA DELL ADSK ESTC MRVL etc) then dive into Research/News…

BABA +5%: Mixed quarter as revenue and miss and margin pressure weighing despite accelerating cloud growth and solid CMR

Revenue of RMB247.7bn grew +2% y/y but missed Street by ~2%. On a like-for-like basis (excluding deconsolidations), growth would have been closer to +10%. Cloud growth the big standout for us as it accelerated to 26% vs last q in the high teens. Call ongoing…

China E-commerce: Revenue +10% y/y to RMB140.1bn, with CMR also +10% in line with expectations.

International Commerce: +19% y/y to RMB34.7bn, slightly below Street.

Cloud: +26% y/y to RMB33.4bn, a clear beat vs Street and the strongest segment

All Others: -28% y/y to RMB58.6mn.

Group adj. EBITA fell -21% y/y to RMB38.4bn, missing expectations, while margins contracted on weakness in China e-commerce

MRVL -14%: DC q and guide comes in weaker as custom ASIC digestion offsets DD optics…Call goes pretty bad, to put it mildly

Positioning here probably skewed more on the bearish side after investors got positive into June’s AI day, but weak custom guide, DC miss, and lack of details have bears excited about the near-term bear case.

Before we dig into the numbers, let’s talk about the call, where CEO Matt Murphy took a noticeable step down in tone and content from the previous call. He didn’t address why they missed the q/q guide on DC, CFO couldn’t answer a straightforward question about his most important business line because he “didn’t have his spreadsheet.”, and the affirmation around custom wins was missing. He failed to give any details when JPM analyst Harlan Su asked him a straightforward question around AMZN AWS - recall that last quarter and at their analyst day, CEO gave a bunch of breadcrumbs that they won Trn 3, but now radio silence, which aligns with talk that AIchip has won bulk of Trn3 leaving MRVL only with the Lite version.

New business updates were vague: management cited “several” additional billion-dollar sockets since AI Day, plus broad XPU and hyperscaler engagements, but with no granularity to build a long-term bull case.

The Numbers:

Jul‑Q (F2Q26): Revenue $2.006B +58% y/y vs Street $2.01B; EPS $0.67 vs Street $0.67; NG GM 59.4% vs Street 59.5%. By segment: Data Center $1.49B (+3% q/q) vs Street $1.513B; Enterprise $194M vs $185M; Carrier $130M vs $147M; Consumer $116M vs $90M; Auto/Industrial $76M vs $76M.

Oct‑Q (F3Q26) guide: Revenue $2.06B (+3% q/q; +36% y/y) vs Street $2.115B; EPS mid‑$0.74 vs Street $0.73; NG GM 59.5–60% vs Street ~59.3%. Mix: Data Center flat q/q (Street expected +~5% q/q), Enterprise+Carrier ~+30% q/q, Consumer down LSD%, Auto/Industrial ~$35M (auto Ethernet sale).

Bull vs. Bear Debate:

Bulls see MRVL as a prime levered play on AI infrastructure through (i) custom compute as the “second source” and attach partner across hyperscalers with 18+ sockets and a $75B pipeline, (ii) electro‑optics leadership shipping 1.6T and demonstrating 3.2T‑enabling 400G/λ PAM, and (iii) a coming scale‑up networking cycle (UALink/Ethernet) alongside scale‑out Ethernet—plus a cyclical Enterprise/Carrier recovery that smooths the P&L. Bulls will add that co has one of best IPs in semis. This quarter added two pro‑bull datapoints: optics up double‑digit q/q in Oct‑Q and reiterated H2>H1 in custom with Q4 stronger than Q3, while Enterprise/Carrier guided ~+30% q/q on normalized channel inventory. Bulls will argue MRVL can drive mid‑teens to 20%+ revenue growth in CY26 with EPS power of $3.75 in CY25 and a 28x multiple =is a $100+ stock. Some bulls frame it on revenue: if DC grows ~20% in CY26 to ~$6.9B and investors pay ~7x DC revenue for leadership in optics/custom, that lens also supports $100+ scenarios.

Bears will frame the earnings call on their wall. They focus on customer concentration and program visibility in custom compute, worrying that “lumpiness” masks share/roadmap risks into Trainium/next‑gen/AMZN and that limited disclosure on “lead customers” raises even more uncertainty. They also see mix headwinds from custom to gross margin ceilings, and optics cadence as competitive/technology‑dependent (e.g., LPO/CPO pathways). This quarter fed the bear narrative with DC flat q/q for Oct‑Q (bulls wanted growth), custom digestion, and softer tone on next‑year visibility. Bears will say CY26 EPS closer to sub $3 and MRVL shouldn’t deserve more than a 20x multiple given lumpiness and uncertainty in the biz, which means a sub $60 stock.

TMTB: Yup bears have it today. We like easy, simple and clean stories/set-ups and this definitely isn’t one of them. We continue to stay away from MRVL both on long and short side.

Gets a downgrade at BofA…

DELL -7%: Beat on revenue/EPS on record AI server shipments, raised FY26 revenue/EPS and lifted AI server shipment outlook to $20B, but GM compressed on AI mix and the Oct‑Q EPS guide is below Street

Sentiment/Positioned skewed mix here going into the print given concerns around AI server margins and the print delivered on that front as underwhelming margins continue to cloud the strong AI backlog and guidance underwhelmed.