TMTB Morning Wrap

Good morning. QQQs +10bps, BTC +1.4%, as yields flattish.

China/U.S. meeting today…

WH ADVISOR HASSETT: US TO RELEASE EXPORT CONTROLS IF CHINA TALKS GO WELL

Potentially good for NVDA, AMD

We have AAPL WWDC today at 1pm est. NVDA in Paris this week, AMD AI event on June 12th, ADBE/ORCL/GTLB/CHWY earnings, and on the macro front have CPI on Wednesday. Should be a fun one.

Let’s get straight to it…

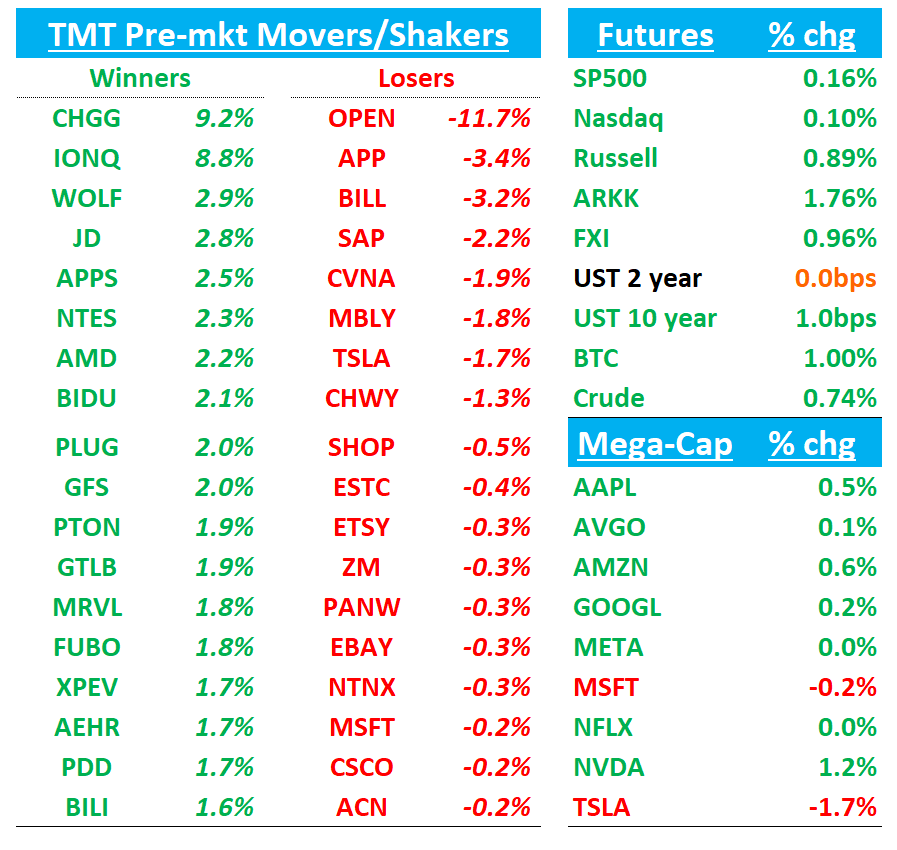

TSLA: Baird Downgrades TSLA to Neutral from Outperform, PT $320

Baird has cut its rating on Tesla to Neutral from Outperform, while keeping its $320 price target intact. In a note to clients, the firm says the stock’s recent strength came despite what it calls a “fundamentally weak quarter,” driven largely by investor hype around the expected unveiling of a lower-cost vehicle and a potential robotaxi launch in June. Baird cautions that Elon Musk’s suggested ramp timeline for the robotaxi business seems overly aggressive and likely already reflected in the stock price. The firm also flags that Musk’s political connections—particularly his ties to Donald Trump—have introduced a new layer of uncertainty. While Baird still considers Tesla a long-term foundational position, it is taking a more cautious stance near-term.

TSLA: Tesla downgraded to Hold from Buy at Argus

Tesla Loses Leader of Optimus Robotics Project

WSJ:

One of Tesla’s top artificial-intelligence executives left the company on Friday, a setback for the Optimus robotics project that Chief Executive Elon Musk says is pivotal to the future of the company.

Milan Kovac, a vice president of engineering, oversaw Tesla’s development of Optimus, a humanoid robot that is central to Musk’s vision of transforming the electric-vehicle maker into a robotics and artificial-intelligence company.

In a post on X, Kovac said he was leaving for personal reasons, and that his support for Musk and Tesla is ironclad. He wrote, “My departure now will not change a thing.”

Third Party Data

SNOW: Cleveland says Q2 tracking slightly ahead of plan and longer term outlooks optimistic

META: Edgewater says fear from early Q2 has largely dissipated for Now as “Agencies see surprisingly buoyant QTD results for DR campaigns”

APP: Morgan Stanley Bullish on sale of 1P games biz

Morgan Stanley reiterated its Overweight rating on AppLovin and raised the price target to $460, highlighting the value potential of the company’s decision to divest its first-party games segment. MS argues the sale would enhance shareholder value while being earnings-neutral, thanks to the way profits will shift from a low-multiple games business to the higher-multiple advertising segment. By removing the Apps unit, AppLovin can now report over $500M in previously internal ad spend as external revenue, which MS estimates will nearly offset the lost EBITDA from games. The firm also raised its valuation multiple on APP’s ad business to 29x EV/EBITDA from 26x, no longer applying a blended multiple that included the lower-valued games unit. With higher-margin, higher-multiple ad revenues now more visible, MS believes APP may actually be worth more without its 1P games portfolio.

HOOD: Redburn Atlantic downgrades to sell from neutral

Redburn Atlantic downgraded Robinhood to Sell from Neutral, even as it raised its price target to $48 from $40. In its note, the firm acknowledges the company’s impressive turnaround, with a pickup in both user growth and deposits. However, Redburn argues that the bullish narrative hinges on the assumption that these gains will prove durable, which it sees as uncertain. The firm questions the strength of Robinhood’s competitive advantages, the uptake of its newer offerings, and the consistency of user engagement. It also highlights that a large portion of revenue is tied to trading activity, which remains closely linked to market cycles. Lastly, Redburn flags potential execution risks tied to international expansion and the integration of two recent acquisitions.

MBLY: Mobileye downgraded to Neutral from Buy at Goldman Sachs

Goldman Sachs downgraded Mobileye to Neutral from Buy while maintaining its $17 price target. GS points to increasing competitive pressure, downside risk to 2026–2027 consensus estimates, and a valuation that it views as already pricing in much of the upside. While the firm still sees Mobileye as technically strong, it notes that adoption of its platform by future AV programs has been more limited than previously anticipated—both in China and globally. Goldman also cautions that U.S. autonomous vehicle volumes will likely stay muted over the next two to three years, primarily confined to commercial use cases.

CHWY: Mizuho “takes a Paws” and downgrades to Hold

Mizuho downgraded Chewy to Neutral from Buy and removed it from their Top Picks, while lifting the price target slightly to $47 from $43. The firm still views the long-term outlook for the business model favorably but believes the near-term setup is less compelling after the stock’s sharp rally—up over 55% since the April lows. Mizuho says customer and revenue growth trends remain solid but are now fully reflected in the valuation, which trades at over 22x forward EV/EBITDA. The firm warns that Q1 expectations are already high, especially with bullish management commentary and potential one-time margin tailwinds from last year. They also highlight risk from a potential supply overhang, noting that BC Partners—Chewy’s largest shareholder—could sell more shares following earnings. While Mizuho’s long-term confidence remains intact, they are stepping to the sidelines near-term due to stretched valuation and limited near-term upside catalysts.

EQIX: Equinix downgraded to Peer Perform on valuation at Wolfe Research

Wolfe Research downgraded Equinix to Peer Perform from Outperform and removed its price target. In its note, Wolfe says it expects the company’s earnings to reflect consistent, steady growth rather than any meaningful acceleration, especially as pricing gains in its core retail offering appear stable but unremarkable. The firm points out that Equinix is now trading at a 27% premium to peers—well above its historical average of 16%—and argues that this elevated valuation could make further multiple expansion tough in the near term. Wolfe believes the current premium to other REITs may already reflect much of the optimism around the name.

ETSY: Jefferies comments positive on app re-design reigniting GMS growth

Jefferies raised its price target on Etsy to $60 from $45 and reiterated a Hold rating, citing early signs that the company’s renewed focus on its mobile app could help revive gross merchandise sales (GMS). The firm highlights a noticeable uptick in app downloads and user engagement, with browser-to-app conversion picking up and app users historically delivering stronger conversion and lifetime value. Jefferies notes total downloads rose 31% in May, with MAUs accelerating and app GMS outperforming non-app channels. However, the firm remains cautious, pointing out that Etsy still needs to demonstrate a durable turnaround after three years of GMS declines. While buyer frequency and monetization could benefit from app-driven improvements, Jefferies is watching for an inflection in churn and more concrete signs of sustained buyer growth before turning more constructive.