TMTB Morning Wrap

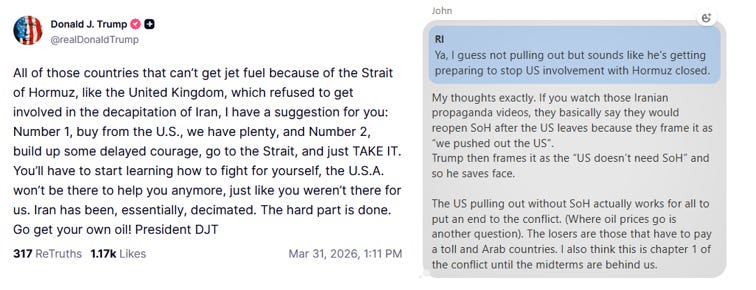

Good morning. Futures +1% as Trump signals he could exit the war without reopening Hormuz - the art of the deal:

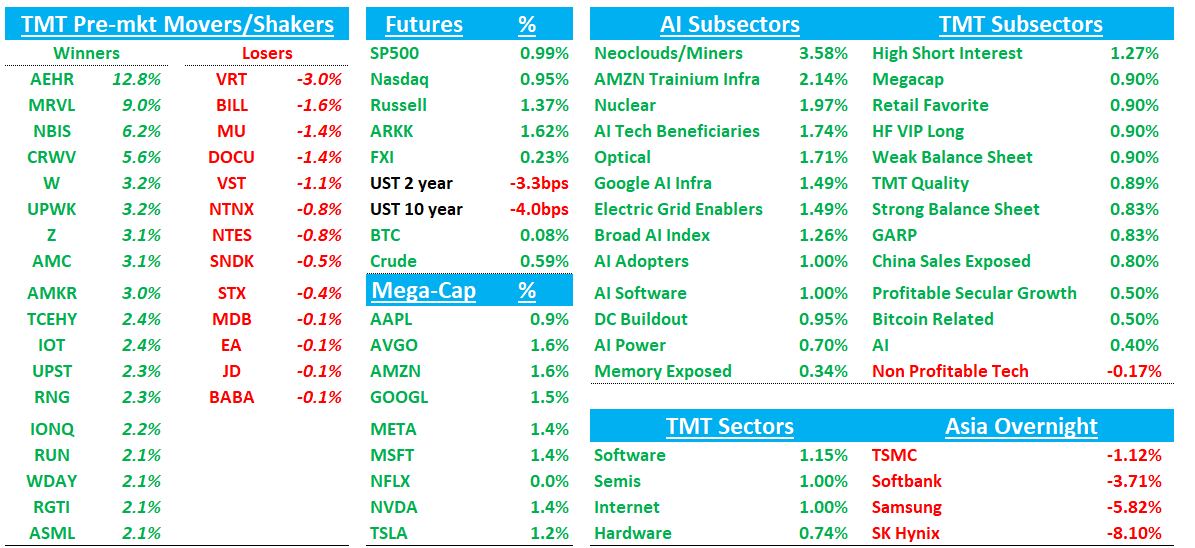

Oil not budging though. Asia re dovernight: TPX -1.26%, NKY -1.58%, Hang Seng +0.15%, HSCEI -0.3%, SHCOMP -0.8%, Shenzhen -1.71%, Taiwan TAIEX -2.45%, Korea KOSPI -4.26%, Samsung -6%; SK Hynix -8%

Early price action shows continuing of yesterday: Memory names weaker while large cap tech is outperforming (AVGO /GOOGL/NVDA/MTEA/AMZN/AMD +1.5% while memory/HDDs flat to down), the perception being what is bad for memory is good for hyperscaler ROI. There’s been a massive rotation into the AI leaders since Oct. and we are seeing a bit of unwind of that trade, relatively speaking, over the last week or so. Interesting that it’s happening again today despite early signs of risk on.

Let’s get to the good stuff…

NVDA/MRVL +9%: NVIDIA AI Ecosystem Expands as Marvell Joins Forces Through NVLink Fusion - NVDA Invests $2B in MRVL

NVIDIA and Marvell Technology, Inc. (NASDAQ: MRVL) today announced a strategic partnership to connect Marvell to the NVIDIA AI factory and AI-RAN ecosystem through NVIDIA NVLink Fusion™, offering customers building on NVIDIA architectures greater choice and flexibility in developing next-generation infrastructure. The companies will also collaborate on silicon photonics technology.

WDC/STX/SNDK: Bernstein Upgrades WDC to Outperform, Says TurboQuant Selloff Overdone — Zero Impact on HDD, Negligible on NAND

Bernstein argues the ~20% selloff in HDD and memory names since Google’s TurboQuant announcement is an overreaction, noting TurboQuant only compresses KV cache during inference — “zero impact to HDD demand and negligible impact on NAND.” The firm upgrades WDC to Outperform with a $340 target (20x FY28 EPS), impressed by its ePMR roadmap though noting what looks like a soft push-out of HAMR by 1-2 years. Bernstein raises STX’s target to $620, calling it their top HDD pick on a 12-month+ horizon given HAMR’s higher areal density should drive accelerating cost declines in FY27-28. AI workloads, richer content creation, and data sovereignty requirements continue to support demand and pricing, with combined WDC/STX revenue now expected to grow at a 24% CAGR through FY30.

VRT: Jefferies Assumes Coverage at Hold from Buy/$260 PT, Says Demand Is Strong but Consensus Already Embeds Aggressive Expectations

Jefferies starts Vertiv at Hold, arguing that while demand is robust (4Q organic orders +252% YoY, TTM orders +81%), the Street at +23% organic growth for 2027 already assumes VRT hits its long-term 25% margin target a year early and underwrites smooth capacity expansion — “which carries some risk.” The firm sees datacenter equipment as potentially entering a “weaker for longer” phase where strength persists but tougher comps, large order volatility, and capacity/labor constraints mean growth “may miss the most robust bull expectations.” Jefferies prefers to wait for a better entry point at $260 PT (26x 2027E EBITDA).