TMTB MORNING WRAP

QQQs hovering near flat. BTC -1%. China +1%. Yields dipping 4-6bps across the curve.

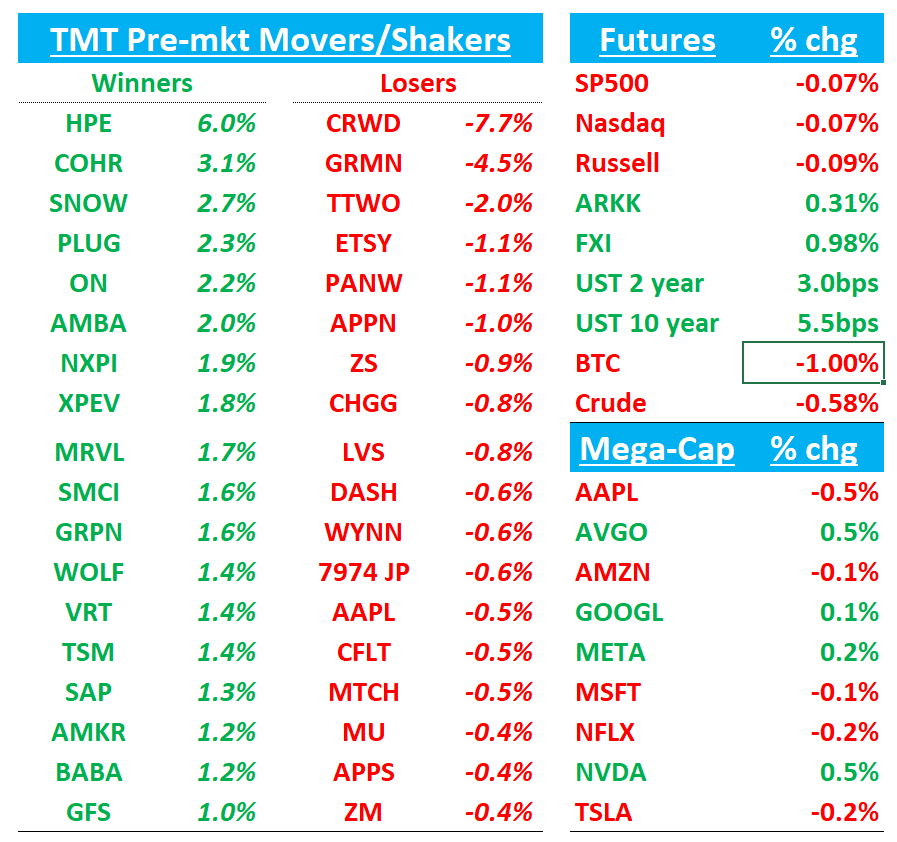

Let’s get straight to it - earnings first (CRWD, HPE, ASAN, GWRE, LITE), then News/Research/3p…

EARNINGS

CWRD -7%: NNARR misses bogeys, Q2 rev guide a bit light, and FY reiterated

Lots of debate on this one overnight…

NNARR slightly light of bogeys at $193.8B vs bogeys closer to $190-$210M and street at $175M…Revs missed slightly for first time as a public co (although hit by CCP rebate issue - $11M impact in the q)

Other than that #s seemed ok as margins/billings came in better. Expectations high here as stock sitting at ATHs and NNARR expects had crept up and mgmt didn’t do a great job explaining the slowing growth. Authorized a $1B repurchase.

Q2 margins guided slightly above and Q2 Revs were slightly below street but driven by impact of CCP rebates: Specifically, partners were offered their own CCP incentives, including cash rebates tied to performance thresholds. Under ASC 606, these rebates are recorded as contra-revenue, effectively reducing reported revenue in the current period. These will shave $10–15 million off subscription revenue in both Q2 and Q3 before fading in Q4. These rebates do not affect ARR.

While the company does not formally guide ARR, it said the sequential growth rate for net-new ARR will be “at least double” last year’s 2.8 % step-up; that implies ≈ $205 million of NNARR for Q2 versus consensus ≈ $193 million, 6 % upside. Assuming and average $20M - 25M beat and you get +4-6% growth, which is first time in 4 quarters NNARR is going to go positive y/y

Bull vs. Bear Debate:

HF Bears pretty vocal overnight and co. got 3 downgrades overnight.

Bulls (mainly long onlys) argue that CrowdStrike’s platform story is intact: Flex packaging is driving larger, longer deals and early “re-Flex” renewals show customers are consuming, not shelf-ware. Triple-digit growth in Next-Gen SIEM and accelerating MSSP traction point to a second leg of growth beyond core endpoint protection. Management’s confidence in a 2H-26 net-new ARR bounce and acceleration, combined with a freshly raised buy-back and path to >30 % FCF margins is enough to support the multiple.

Bears (mainly HFs) counter that headline growth is slowing (first rev miss as a public company and slightly below 20% for first time) and investors are frustrated with one-time issues the co keeps calling out — why wasn’t CCP issue addressed earlier? The ARR beat was the smallest in five quarters, revenue guidance is below street and net-new ARR is still down year-on-year. Of course co going to accelerate when comps get massively easier given last year’s outage. Guide implies only 20% growth with risk it might dip into teens next year. With the stock at ~20× CY-26 sales and ~70× FCF, any slip-up—whether slower “re-Flex” velocity, tougher macro budgets, dip into teens growth or mounting competition from Microsoft and SentinelOne—should compress the multiple.

Our view? Lots of frustration on buyside about why stock not down more especially given valuation/rev + NNARR miss, but we think bull case stays intact here and not going to shake many long-onlys off and their willing to defend one of their favorite software stocks as investors continue to want exposure to Cyber…we don’t have a strong view on this one and aren’t involved…

BofA downgrades saying while the firm favors CrowdStrike's fundamentals and growth prospects, its believes the valuation "leaves only limited upside" from current levels, noting that its raised price target implies 3% upside potential at the after-hours closing price of $457. Growth has decelerated to below 20% in the first half of FY26 and while the firm expects acceleration to about 22% in the second half on the back of CCP related renewals, it believes growth will decelerate in the next few years, the analyst added.

Evercore ISI downgrades saying he company's Q1 "was solidly executed, though not exceptional," the analyst tells investors in a research note. The firm detects growing investor frustration around several lingering, unaddressed issues at CrowdStrike. Evercore awaits more clarity before recommending the shares and is "taking a breather."

Canaccord downgrades: . While encouraged by some early expansionary proof points within the Flex customer base and viewing CrowdStrike's business operations since the July 19 incident "as nothing short of remarkable," Canaccord simply believes the stock's risk/reward is more balanced at these levels with shares trading near 21-times estimated 2026 sales.

HPE -7%: Clean beat and raise as cc growth re-accelerates after two messy quarters

HPE printed revenue of $7.63 bn, 2 % above Street’s $7.45 bn, and non-GAAP EPS of $0.38, a $0.05 beat.

Constant-currency growth re-accelerated to +7 % as every segment returned to y/y growth, led by Hybrid Cloud (+15 % cc) and a long-awaited rebound in Intelligent Edge (+8 % cc).

Gross margin 29.4 %, roughly 60 bps ahead of street; operating margin was 8.0 %, also ahead.

AI systems revenue reached $1.0 bn (Street ≈ $0.9 bn) and cumulative AI orders now total $9.3 bn with backlog at $3.2 bn.

ARR for GreenLake/as-a-Service hit $2.2 bn, up 47 % y/y.

Jul-quarter guidance calls for revenue of $8.2–8.5 bn (mid-point 1.6 % above Street) and EPS of $0.40-0.45 (mid-point in line).

FY25 revenue range tightens to +7-9 % cc while the EPS floor rises to $1.78 on a lower tariff drag (-$0.04 vs -$0.07 prior).

Key takeaways

Macro/Tariffs: Management struck a more upbeat tone on enterprise demand for AI clusters while acknowledging a still-mixed macro backdrop and no evidence of pull-forward buying. Tariff costs proved milder than feared—just 2 c in the quarter and 4 c for the year—thanks to supply-chain work-arounds and mgmt feels confident on further mitigation. A 5 % workforce reduction and inventory discipline underpin plans to exit FY25 with gross margin back above 30 % and operating margin above 9 %.

AI: $1 bn shipped this quarter, backlog steady at $3.2 bn and a “multiples-of-backlog” pipeline, with one of the world’s largest GB200 deployments slated for F3Q.

Catalysts: Juniper/DOJ ruling (trial starts July 9), Discover product launches, October analyst day.

Bull vs. Bear Debate

Bulls argue that HPE has turned the corner: AI systems demand is translating into tangible revenue beats, Alletra and GreenLake are accelerating high-margin recurring ARR, and management’s cost actions give earnings upside even if macro IT budgets stay sluggish. With EPS now tracking toward the high end of guidance and the stock at roughly 8× FY26 consensus, r/r probably only $2 down and $6-7 up plus optionality from a successful Juniper close and networking cross-sell.

Bears counter that the story remains heavily dependent on a few very large AI server deals that can slip, and gross margin is still 370 bps below last year because of that hardware mix. Free cash flow remains negative and July’s DOJ trial could derail the Juniper strategy. They also worry that the tightened FY guide hides a softer F4Q revenue trajectory once the biggest AI order ships, and that any macro wobble or tariff re-escalation could quickly erase the slim margin gains.