TMTB Morning Wrap

Akramsrazor from X will be in TMTB Chat hosting a thread at 12pm est. to discuss his long GTLB view. We think he’s one of the better software investors (are there any left?) around. Here’s his recent post-earnings piece on GTLB if you haven’t read it.

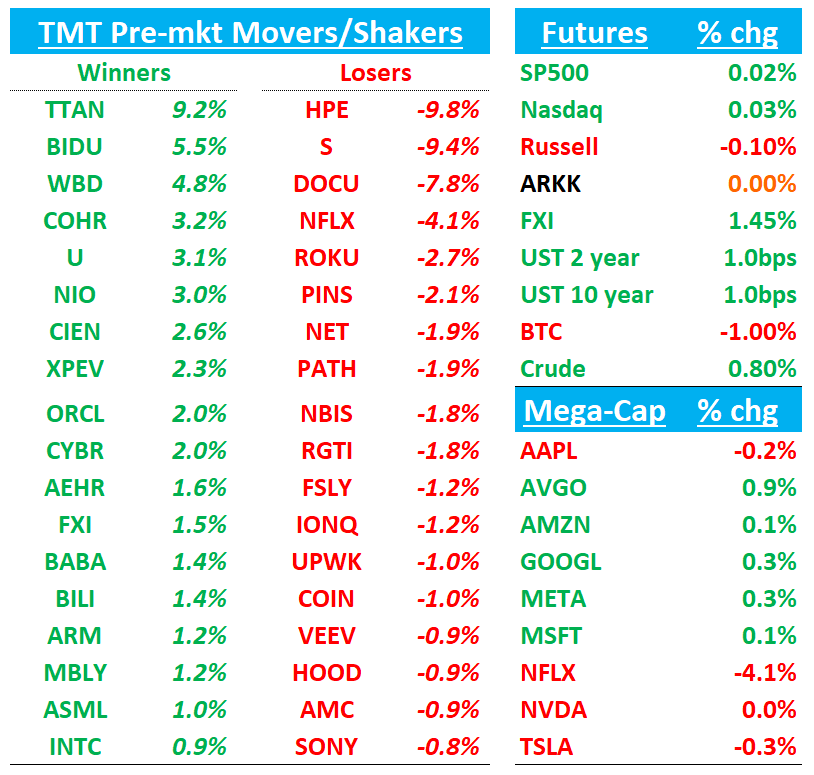

QQQs +15bps to start the day. BTC -1.4%. Yields ticking up slightly. Asia was generally up overnight with China +1.5% leading the way after a successful debut from Moore Threads Technology (+500%). Memory strong with KIOXIA+4%, SAMSUNG+3%, NANYA+1.3%, HYNIX +1%.

Lots to get to so let’s get to it. We’ll start with HPE, DOCU, TTAN, IOT, RBRK earnings then move onto the usual.

No EOD wrap today as I’ll be on the road.

Let’s get to it…

EARNINGS

HPE -9% mixed print: revenue missed but margins, EPS and FCF beat, AI demand stayed strong in orders/backlog, and FY26 EPS/FCF guidance was raised while near‑term revenue outlook was reset lower.

Key #s / Takeaways:

F4Q25 revenue was $9.679B, +14.4% y/y (last q +18.5% y/y) vs Street $9.877B, +~17.5%, a ~2% top‑line miss driven mainly by AI server shipment timing and weaker U.S. federal.

F4Q25 Non‑GAAP EPS of $0.62 beat Street $0.58 on record 36.4% gross margin and 12.2% operating margin, helped by networking mix; FCF was $1.9B vs Street ~$1.7B.

AI systems revenue stepped down to $1.0B (from $1.6B last q) but orders were $1.9B and backlog rose to $4.7B, with ~60% of cumulative $13.4B orders now from enterprise/sovereign customers.

FY26 guide held +17–22% reported revenue growth (5–10% pro‑forma) but raises EPS to $2.25–2.45 (from $2.20–2.40) and lifts FCF guidance to $1.7–2.0B, implying more profit/FCF on similar growth, with H2 weighted by AI shipments. Management highlighted that most AI backlog will ship in 2H26 and beyond, and that AI systems demand remains robust despite shipment timing.

Networking revenue hit $2.8B, +150% y/y, with 23% segment OM and Juniper delivering an 8‑year high operating margin, helped by synergies. For FY26, management now guides networking revenue to grow 65–70% reported to ~$11B (mid‑single‑digit pro‑forma) and expects networking to generate >50% of total operating profit at low‑20s OM, underscoring a structural mix shift toward higher‑margin businesses.

Server revenue declined 5% y/y on a 10% q/q drop, with management citing timing of AI shipments and weaker U.S. federal spending as the main drags. At the same time, traditional servers and Alletra MP storage saw double‑digit order growth, and private cloud AI orders more than doubled sequentially, supporting the view that core IT demand is healthy even as large AI deals remain lumpy.

Management described the underlying demand environment as strong, with orders growing faster than revenues and an acceleration in orders in the last weeks of the quarter, driven by networking and AI. The main demand headwind flagged was lower‑than‑expected U.S. federal spending in servers

HPE called out industry‑wide DRAM/NAND inflation, saying they are monitoring these markets daily, taking pricing actions, and expect to pass through the majority of component cost increases while monitoring demand elasticity. Servers are most exposed, then storage, then networking; this is one of the main bear talking points given the risk to volume if price hikes bite. The FY26 guide already assumes higher DRAM pricing, and they have already implemented price increases; they expect revenue impact from memory inflation to be net neutral over time as higher average selling prices offset any modest volume headwinds.

Bull vs. Bear Debate

Bulls see this quarter as noise around timing that doesn’t derail the core thesis: HPE is transitioning into a higher‑growth, higher‑margin infrastructure platform where networking, AI systems and GreenLake‑delivered software/services meaningfully lift earnings power. Networking is already +150% y/y with 23% OM, and management expects it to be >50% of total operating profit at low‑20s OM in FY26 – a very different mix than the legacy commodity server/storage business. Add to that 62% ARR growth to $3.2B with ~80% software/services, and bulls argue HPE’s earnings quality is steadily improving and cyclicality should moderate over time.

On AI, bulls focus less on Q4’s $1.0B vs $1.6B revenue and more on the structural indicators: $13.4B cumulative orders, $4.7B backlog (up from $3.7B), a pipeline that management describes as multiples of backlog, and a customer mix now skewed to sovereign/enterprise (>60% of bookings). They like that FY26 revenue guidance is unchanged while EPS and FCF guidance are raised, suggesting HPE can offset DRAM inflation and AI lumpiness through price, mix and cost actions. Assuming their >$3 LT EPS guide holds for FY28, at $20, you have a stock trading at sub 7x earnings and bulls will say there is limited downside while a re-rating higher because of the networking biz could get you something closer to $33-36.

Bears focus on growth quality, cyclicality and execution risk, arguing that the quarter reinforces concerns that HPE’s growth is still heavily tied to big, lumpy AI and networking projects in a volatile component‑cost environment. Pro‑forma, HPE is still only guiding 5–10% revenue growth; once you strip out Juniper and the initial AI ramp, that looks like a mid‑single‑digit grower with heavy capital needs. The top‑line miss in Q4 and material under‑guide vs Street for F1Q26 revenue despite a “strong demand environment” feed the narrative that management is still working through visibility issues on AI deployments, customer readiness, and federal budgets. Bears also worry about memory/DRAM inflation and demand elasticity. While HPE expects to pass through most cost increases, that inherently means higher prices for customers and could pressure unit volumes just as AI systems remain nascent and highly competitive versus other OEMs and ODMs

DOCU -7% posted a solid Q3 beat on revenue, billings, margins and FCF with visible IAM traction, but the normalized growth rate, early‑renewal dependence, pulling billings disclosure disappointed

Key #s / Takeaways:

F3Q26: Revenue $818.4M, +8.4% y/y (last q +8.8% y/y) vs Street ~$806M, +6.8%; subscription revenue $801M, +9% y/y vs Street ~$789M; billings $829M, +10.3% y/y vs Street ~$790M, +5%. Non‑GAAP OM was 31.4% vs Street ~28.5%, with ~1.5 pts of one‑time/timing benefit and underlying OM ~30%; non‑GAAP EPS $1.01 vs Street $0.92. Non‑GAAP OM of 31.4% expanded nearly +200bps y/y, but included ~150bps of one‑time/timing savings, leaving “core” OM around 30%.

FY26 guidance nudged up: revenue now $3.208–3.212B (+8% y/y) and billings $3.379–3.389B (+9% y/y), both modestly ahead of the Street and prior guide, while OM guidance moves up to ~29.8–29.9% (flat y/y).

Management highlighted that slightly more than half of the billings outperformance vs plan came from early renewals, with underlying billings growth closer to ~8% y/y. That, plus FX and a shift to annual payment terms, suggests a good but not step‑function re‑acceleration in core demand.

DOCU will stop reporting billings after Q4’26 and instead disclose annual ARR and IAM as a % of ARR, with full‑year ARR growth guidance for FY27 updated each quarter. Management stressed quarterly net‑new ARR is only ~$60M on average in FY26 and highly timing‑sensitive, so they view annual ARR plus IAM mix as a better lens on long‑term growth than volatile quarterly billings.

Management repeated that “there’s nothing material that we’ve seen in the business in Q3” from a macro standpoint; consumption and usage trends remain consistent, with “pretty strong year‑over‑year growth across most verticals,” even as customers continue to scrutinize spend. Dollar net retention improved to 102% (vs 100% a year ago, 102% in Q2), supported by envelope utilization “amongst the highest levels we have seen since early fiscal 2022” and consistently growing envelope volumes over the last five quarters.

Strategically, IAM is scaling (25K+ customers vs 10K in April, tracking to low‑double‑digit % of recurring revenue by year‑end), NRR improved to 102%, envelope utilization is at multi‑year highs, international reached 30% of revenue (+14% y/y), and management leaned into AI (contract agents, LLM partnerships, FedRAMP/GovRAMP) while calling the macro/IT‑spend backdrop stable and downplaying AI “noise” from DocuGPT.

Management, including on the callback, continues to downplay any material impact from “AI noise”, emphasizing they aren’t trying to be an LLM provider and instead see LLMs as partners plugged into IAM’s workflow/data moat.

Bull vs Bear Debate:

Bulls say Q3 reinforces a thesis that DOCU is quietly rebuilding a durable, higher‑quality growth engine on top of a very sticky core. IAM now has 25K+ paying customers (up from 10K in April), is on pace to reach a low double‑digit percentage of recurring revenue by year‑end, and early renewal cohorts are showing gross retention several points above the corporate average with higher eSign usage post‑migration. Dollar net retention has climbed back to 102% on multi‑year‑high envelope utilization, while customers spending >$300K ACV posted their best growth in over two years. Bulls see this as evidence that core demand is healthy and IAM is starting to bend the growth curve, even if the P&L contribution is still modest in dollar terms. On the AI front, bulls argue DOCU is structurally better positioned than the “DocuGPT panic” narrative suggests. Management highlighted a ~15‑point accuracy advantage from training models on a massive corpus of consented private agreements, plus deep integrations into system‑of‑record apps (Salesforce, HRIS, ERP) and FedRAMP/GovRAMP authorization that generic LLM agents don’t have.

Bears see a very different picture: a core eSignature business that has structurally slowed to mid‑ to high‑single‑digit growth, an IAM story that is real but small, and a valuation that already embeds much of the upside. Normalized billings growth was ~8% y/y this quarter (once you strip out early‑renewal timing), and the Q4 guide explicitly calls for revenue growth to decelerate vs Q3 due to tough comps and less early‑renewal benefit. Bears argue that “beat‑and‑raise” is being driven as much by renewal timing, FX, and mix shift to annual billings as by genuine underlying acceleration, and that DOCU still hasn’t demonstrated a sustained path to double‑digit revenue growth.

Another key bear nitpick is around margins and the metric shift. FY26 non‑GAAP OM will now be ~29.8–29.9%, up from prior 29.1% but still flat vs FY25, and management has leaned heavily on one‑time/timing benefits (about 150bps in Q3) plus a multi‑year cost‑cutting cycle to get to 30% OM. Bears worry that with cloud migration, comp mix shifts (more cash vs equity) and IAM investment, further OM expansion will be hard without a step‑up in growth—so DOCU is increasingly a “steady 8–9% grower at ~30% OM,” not a compounder. The decision to retire billings and guide only annual ARR (without quarterly ARR disclosure) feeds skepticism that management wants to reduce scrutiny on a metric that has historically surfaced growth issues. Lastly, AI/competition is an additional pressure point. The DocuGPT demo and other internal agents from OpenAI remain an overhang that is unlikely to go away and will improve over time.

EARNINGS QUICK HITS:

IOT: Delivered a solid 3Q, highlighted by steady total ARR expansion and a pickup in NNARR.

IOT posted strong F3Q26 results, with revenue coming in 4% ahead of Street and ARR +29%. NNARR accelerated to 24% (vs. 19% in F2Q26), fastest pace in 7 quarters. Operating margin and FCF margin exceeded expectations by 420bps and 220bps, respectively.

RBRK +18% posted a clean beat-and-raise quarter with record net new ARR, first positive non‑GAAP operating margin, and a substantial raise to FY26 ARR/revenue/FCF guidance

This quarter mostly reinforced the bull narrative and softened several bear arguments. Rubrik showed it can deliver record NNARR, re‑accelerating cloud ARR, and strong identity traction while also inflecting to positive operating margin and 22% FCF margin, prompting a broad‑based raise to ARR, revenue, EPS, ARR contribution margin and FCF guidance.

The #s: Subscription ARR came in at $1.347B, +34% y/y, ~2% above Street ($1.321B, +31.8% y/y). Net new subscription ARR was ~$94–95M, +14% y/y, vs Street around $68–71M and ahead of prior‑quarter $71M. Cloud ARR grew +53% y/y to $1.175B, now 87% of subscription ARR (vs 77% a year ago). Subscription revenue of $336.4M, +51.9% y/y beat Street’s $307.5M (+38.8% y/y), and total revenue of $350.2M, +48% y/y beat Street’s $320.5M (+35.7% y/y) and the guidance midpoint by ~$30M. FY26 guidance for subscription ARR, revenue, EPS, ARR contribution margin and FCF all moved higher; normalized FY26 revenue growth is now ~35% despite a sizable non‑recurring “material rights” tailwind (~$68M) that will become a reported-growth headwind in FY27

TTAN +9% posted another beat‑and‑raise quarter with accelerating GTV, clean execution on Pro/AI and commercial initiatives, and a modestly better FY26 outlook despite tougher comps into year‑end.

For bulls, the biggest incremental positives were the re‑acceleration of GTV to ~22% y/y (with clear commentary that HVAC OEM weakness isn’t showing up in TTAN’s data), the strong beat and raise on revenue and margins, and concrete progress on AI/Pro and commercial initiatives (Field Pro, virtual agents, the Max program, commercial CRM and construction management, high‑profile enterprise/roofing wins). The margin story also improved: TTAN is pacing ahead of its 25% incremental‑margin target and delivered record FCF while still investing, which supports the thesis that it can expand profitability without sacrificing growth.

TECH RESEARCH/NEWS

NFLX/WBD: Netflix says it’s struck a deal to buy Warner Bros. Discovery for $27.75 per share

NFLX -2%; ROKU -3%…Big question is does this get approved - they’ll have to argue for pay TV market but DOJ might argue for streaming market…Other qustion is does PSKY go all cash at a lower price (higher certainty of closing and shorter timeline)

CNBC:

The deal is comprised of cash and stock and is valued at $27.75 per WBD share, the companies said. That puts the total enterprise value of the transaction at approximately $82.7 billion.

The deal is for WBD’s film studio and streaming service, HBO Max. Warner Bros. Discovery will still spin out its TV networks, which includes TNT and CNN, as previously planned.

The acquisition is expected to close after that separation takes place, now expected in the third quarter of 2026.